Exam 5: Cost Allocation and Activity-Based Costing Systems

Exam 1: Management Accounting and Management Decisions90 Questions

Exam 2: Cost Behaviour and Cost-Volume Relationships96 Questions

Exam 3: Measurement of Cost Behaviour97 Questions

Exam 4: Cost Management Systems134 Questions

Exam 5: Cost Allocation and Activity-Based Costing Systems128 Questions

Exam 6: Job-Costing Systems88 Questions

Exam 7: Process-Costing Systems82 Questions

Exam 8: Relevant Information and Decision Making: Marketing Decisions100 Questions

Exam 9: Relevant Information and Decision Making: Production Decisions111 Questions

Exam 10: Capital Budgeting Decisions116 Questions

Exam 11: The Master Budget112 Questions

Exam 12: Flexible Budgets and Variance Analysis106 Questions

Exam 13: Management Control Systems, the Balanced Scorecard, and Responsibility Accounting94 Questions

Exam 14: Management Control in Decentralized Organizations103 Questions

Select questions type

Activity-based accounting systems classify more costs as direct, thus simplifying and reducing the cost of a traditional system.

(True/False)

4.8/5  (34)

(34)

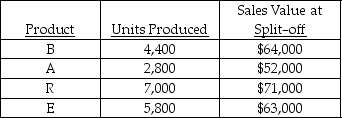

Bare Company manufactures four products from a joint process. Joint costs for the year amounted to $140,000. The following data are also available:

-Assuming the relative-sales-value method of allocating joint costs, the amount of joint costs allocated to product R would be

-Assuming the relative-sales-value method of allocating joint costs, the amount of joint costs allocated to product R would be

(Multiple Choice)

4.8/5 (43)

The preferred guidelines for allocating service department costs include all of the following EXCEPT

(Multiple Choice)

4.8/5 (35)

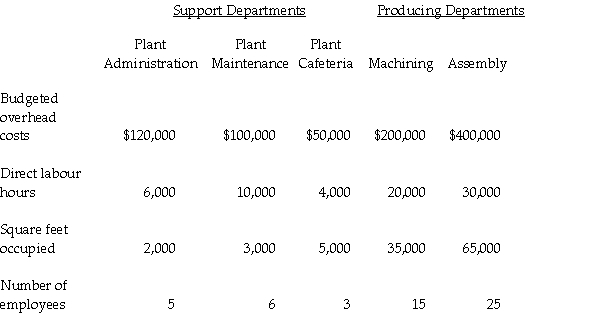

Henry Company has three support departments and two producing departments. Information for each department for 2006 is as follows:  Plant administration costs are allocated based on direct labour hours, plant maintenance costs are allocated based on square footage occupied, and plant cafeteria costs are allocated based on the number of employees.

The company does not divide overhead into fixed and variable components. Predetermined overhead rates for the producing departments are based on direct labour hours.

Allocate the support department costs using the direct method. Next calculate the predetermined overhead rates the producing departments would use to apply overhead to units of product.

Plant administration costs are allocated based on direct labour hours, plant maintenance costs are allocated based on square footage occupied, and plant cafeteria costs are allocated based on the number of employees.

The company does not divide overhead into fixed and variable components. Predetermined overhead rates for the producing departments are based on direct labour hours.

Allocate the support department costs using the direct method. Next calculate the predetermined overhead rates the producing departments would use to apply overhead to units of product.

(Essay)

4.9/5 (40)

Which of the following is NOT a name for a system that first accumulates overhead costs for each of the activities of an organization, and then assigns the costs of activities to the products, services, or other cost objects that caused that activity?

(Multiple Choice)

4.8/5 (26)

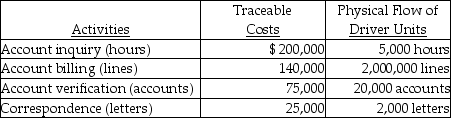

John Gordan Company had the following activities, traceable costs, and physical flow of driver units:

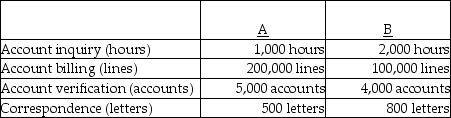

The above activities are used by departments A and B as follows:

The above activities are used by departments A and B as follows:

-How much of the account inquiry cost will be assigned to Department A?

-How much of the account inquiry cost will be assigned to Department A?

(Multiple Choice)

4.8/5 (32)

A method that simultaneously allocates service costs to all user departments. It gives full consideration to interactions among support departments.

(Short Answer)

4.9/5 (42)

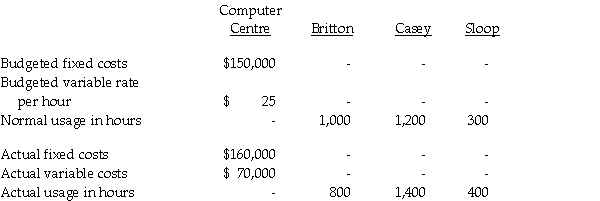

There are three Easy Stay Inns, one in each of the following cities: Britton, Casey, and Sloop.

The central office provides computer services to each of the three motels. Information pertaining to the computer centre and the three motels follows.  a. Using the direct method, allocate the computer centre costs to each motel location to provide information for setting room rates.

b. Using the direct method, allocate the computer centre costs to each motel location assuming the purpose is to evaluate performance.

c. Did the total amount allocated in requirement (B) above differ from the amount of costs incurred by the computer centre?

a. Using the direct method, allocate the computer centre costs to each motel location to provide information for setting room rates.

b. Using the direct method, allocate the computer centre costs to each motel location assuming the purpose is to evaluate performance.

c. Did the total amount allocated in requirement (B) above differ from the amount of costs incurred by the computer centre?

(Essay)

4.9/5 (34)

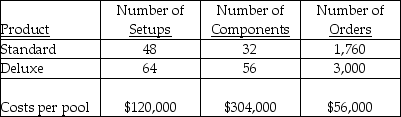

Dorpinghaus Corp. manufactures two models of its telephones, a standard and a deluxe model. Three activities have been identified as cost drivers and the related costs pooled together to arrive at the following information:

-If activity-based costing is used, then the total cost of the components used in the deluxe model would be

-If activity-based costing is used, then the total cost of the components used in the deluxe model would be

(Multiple Choice)

4.9/5 (36)

Producing departments are responsible for producing the products sold to customers.

(True/False)

4.9/5 (33)

Costs are allocated for all the following purposes EXCEPT to

(Multiple Choice)

4.8/5 (28)

Which of the following is NOT an example of a non-value-added cost?

(Multiple Choice)

4.8/5 (28)

A method of allocating service costs that ignores any interactions that may exist among support departments.

(Short Answer)

4.8/5 (33)

One of the main objectives of cost allocation is to motivate managers.

(True/False)

4.8/5 (44)

The direct method of allocating service department costs partially recognizes services that service departments provide to each other.

(True/False)

4.7/5 (38)

Stumbo Company has two production departments, Cutting and Assembling, served by one maintenance department. Budgeted fixed costs for the maintenance department for 20X3 were $60,000, and the variable cost per labour hour was $2.00. Other relevant data for 20X3 are as follows:

Actual maintenance department costs for 20X3 were $64,000 fixed and $120,000 variable.

*in labour hours

-The amount of fixed maintenance costs allocated to the Cutting Department should be

Actual maintenance department costs for 20X3 were $64,000 fixed and $120,000 variable.

*in labour hours

-The amount of fixed maintenance costs allocated to the Cutting Department should be

(Multiple Choice)

4.7/5 (35)

Stohr Company has two departments, New and Old. Central costs are allocated to the two departments in various ways. Relevant information is presented below:

-If total advertising expense is $240,000 and it is allocated on the basis of sales, the amount allocated to the New Department should be

-If total advertising expense is $240,000 and it is allocated on the basis of sales, the amount allocated to the New Department should be

(Multiple Choice)

4.9/5 (45)

John Gordan Company had the following activities, traceable costs, and physical flow of driver units:

The above activities are used by departments A and B as follows:

-What is the cost per driver unit for the account inquiry activity?

(Multiple Choice)

4.8/5 (36)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)