Exam 5: Cost Allocation and Activity-Based Costing Systems

Exam 1: Management Accounting and Management Decisions90 Questions

Exam 2: Cost Behaviour and Cost-Volume Relationships96 Questions

Exam 3: Measurement of Cost Behaviour97 Questions

Exam 4: Cost Management Systems134 Questions

Exam 5: Cost Allocation and Activity-Based Costing Systems128 Questions

Exam 6: Job-Costing Systems88 Questions

Exam 7: Process-Costing Systems82 Questions

Exam 8: Relevant Information and Decision Making: Marketing Decisions100 Questions

Exam 9: Relevant Information and Decision Making: Production Decisions111 Questions

Exam 10: Capital Budgeting Decisions116 Questions

Exam 11: The Master Budget112 Questions

Exam 12: Flexible Budgets and Variance Analysis106 Questions

Exam 13: Management Control Systems, the Balanced Scorecard, and Responsibility Accounting94 Questions

Exam 14: Management Control in Decentralized Organizations103 Questions

Select questions type

If the allocation is for performance evaluation, variable service department costs should be allocated based on the actual rate and actual usage.

(True/False)

4.8/5  (40)

(40)

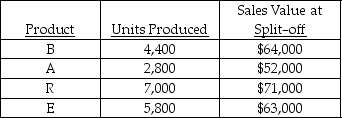

Bare Company manufactures four products from a joint process. Joint costs for the year amounted to $140,000. The following data are also available:

-Assuming the relative-sales-value method of allocating joint costs, the amount of joint costs allocated to product A would be

-Assuming the relative-sales-value method of allocating joint costs, the amount of joint costs allocated to product A would be

(Multiple Choice)

4.9/5 (34)

County Company has two service departments, Maintenance and Personnel, as well as two production departments, Mixing and Finishing. Maintenance costs are allocated based on square footage, while personnel costs are allocated based on number of employees. The following information has been gathered for the current year:

-If the step-down method is used to allocate costs, and the Maintenance Department renders the greatest service, then the total cost of the Mixing Department after allocation would be

-If the step-down method is used to allocate costs, and the Maintenance Department renders the greatest service, then the total cost of the Mixing Department after allocation would be

(Multiple Choice)

5.0/5 (37)

A method of allocating support department costs that gives partial consideration to interactions among support departments.

(Short Answer)

4.7/5 (36)

The goal of a just-in-time production system is to have zero inventory.

(True/False)

4.8/5 (43)

In the step-down method, the last service department in the sequence is the one that renders the

(Multiple Choice)

4.7/5 (35)

Service department costs should be allocated directly to units of product.

(True/False)

4.7/5 (45)

Each of the following is a step in the general approach to allocating costs to final products or services EXCEPT

(Multiple Choice)

4.7/5 (38)

Two dimensions are important in flexible production operations:

(Multiple Choice)

4.8/5 (41)

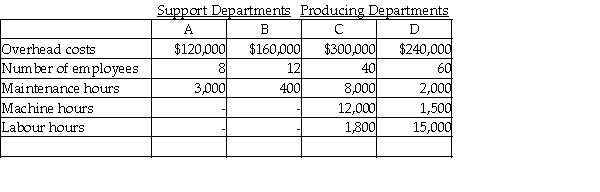

Use the following information to answer item(s) below.

Meesen Inc. operates two support departments (A and B) and two producing departments (C and D). Budgeted costs and normal activity levels are given below.  The costs of Department A are allocated on the basis of number of employees, and the costs of Department B are allocated on the basis of maintenance hours.

-If the direct method is used, Department B costs allocated to Department C would be

The costs of Department A are allocated on the basis of number of employees, and the costs of Department B are allocated on the basis of maintenance hours.

-If the direct method is used, Department B costs allocated to Department C would be

(Multiple Choice)

4.8/5 (32)

City Company has two service departments, Maintenance and Personnel, as well as two production departments, Mixing and Finishing. Maintenance costs are allocated based on square footage while personnel costs are allocated based on number of employees. The following information has been gathered for the current year:

-If the step-down method is used to allocate costs, and the Maintenance Department renders the greatest service, then the total amount of overhead that would be allocated from Personnel to Finishing is

-If the step-down method is used to allocate costs, and the Maintenance Department renders the greatest service, then the total amount of overhead that would be allocated from Personnel to Finishing is

(Multiple Choice)

4.8/5 (36)

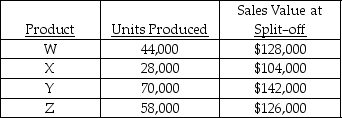

Upjohn Company manufactures four products from a joint process. Joint costs for the year amounted to $350,000. The following data are also available:

-Assuming the physical-units method of allocating joint costs, the amount of joint costs allocated to product W would be

-Assuming the physical-units method of allocating joint costs, the amount of joint costs allocated to product W would be

(Multiple Choice)

4.8/5 (34)

Use the following information to answer item(s) below.

Meesen Inc. operates two support departments (A and B) and two producing departments (C and D). Budgeted costs and normal activity levels are given below. The costs of Department A are allocated on the basis of number of employees, and the costs of Department B are allocated on the basis of maintenance hours.

-If the direct method is used, Department A costs allocated to Department C would be

(Multiple Choice)

4.9/5 (31)

Netton Bus Lines provides school bus service to two school districts: East and West.

Taylor has one support centre that is responsible for service, maintenance, and cleanup of its buses. The costs of the support centre are allocated to each district on the basis of total kilometres driven.

During the first month of the year, the support centre was expected to spend a total of $100,000. Of this total, $25,000 was viewed as being fixed.

During the month, the support centre incurred actual variable costs of $105,000 and actual fixed costs of $20,000.

The normal and actual kilometres logged by each district are given below:  a. Compute the predetermined service cost per kilometre driven.

b. Compute the costs that would be allocated at the end of the month to each district for purposes of performance evaluation.

c. Determine the costs of the support centre that were not allocated to the two districts. Why were these costs not allocated to the districts?

a. Compute the predetermined service cost per kilometre driven.

b. Compute the costs that would be allocated at the end of the month to each district for purposes of performance evaluation.

c. Determine the costs of the support centre that were not allocated to the two districts. Why were these costs not allocated to the districts?

(Essay)

4.9/5 (41)

Stumbo Company has two production departments, Cutting and Assembling, served by one maintenance department. Budgeted fixed costs for the maintenance department for 20X3 were $60,000, and the variable cost per labour hour was $2.00. Other relevant data for 20X3 are as follows:

Actual maintenance department costs for 20X3 were $64,000 fixed and $120,000 variable.

*in labour hours

-The amount of fixed maintenance costs allocated to the Assembling Department should be

Actual maintenance department costs for 20X3 were $64,000 fixed and $120,000 variable.

*in labour hours

-The amount of fixed maintenance costs allocated to the Assembling Department should be

(Multiple Choice)

4.7/5 (38)

County Company has two service departments, Maintenance and Personnel, as well as two production departments, Mixing and Finishing. Maintenance costs are allocated based on square footage, while personnel costs are allocated based on number of employees. The following information has been gathered for the current year:

-If the step-down method is used to allocate costs, and the Maintenance Department renders the greatest service, the total amount of overhead that would be allocated from Personnel to Mixing is

(Multiple Choice)

4.8/5 (41)

The techniques used to determine the cost of a product or service by collecting and classifying costs and assigning them to cost objectives.

(Short Answer)

4.9/5 (36)

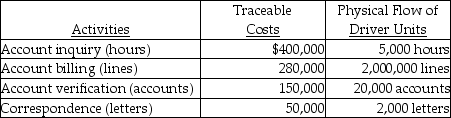

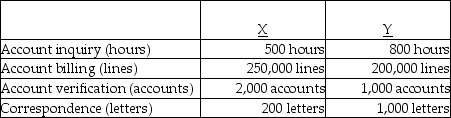

Allen Crabb Corporation had the following activities, traceable costs, and physical flow of driver units:

The above activities are used by departments X and Y as follows:

The above activities are used by departments X and Y as follows:

-How much of the account inquiry cost will be assigned to Department Y?

-How much of the account inquiry cost will be assigned to Department Y?

(Multiple Choice)

4.9/5 (36)

Upjohn Company manufactures four products from a joint process. Joint costs for the year amounted to $350,000. The following data are also available:

-Assuming the physical-units method of allocating joint costs, the amount of joint costs allocated to product Z would be

(Multiple Choice)

4.7/5 (41)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)