Exam 18: Activity-Based Costing and Other Cost Management Tools

Exam 1: Accounting and the Business Environment156 Questions

Exam 2: Recording Business Transactions156 Questions

Exam 3: The Adjusting Process160 Questions

Exam 4: Completing the Accounting Cycle165 Questions

Exam 5: Merchandising Operations168 Questions

Exam 6: Merchandising Inventory155 Questions

Exam 7: Internal Control and Cash161 Questions

Exam 8: Receivables166 Questions

Exam 9: Plant Assets and Intangibles170 Questions

Exam 10: Current Liabilities and Payroll159 Questions

Exam 11: Long-Term Liabilities, Bonds Payable, and Classification of Liabilities on the Balance Sheet161 Questions

Exam 12: Corporations: Paid-In Capital and the Balance Sheet167 Questions

Exam 13: Corporations: Effects on Retained Earnings and the Income Statement164 Questions

Exam 14: The Statement of Cash Flows162 Questions

Exam 15: Financial Statement Analysis163 Questions

Exam 16: Introduction to Management Accounting163 Questions

Exam 17: Job Order and Process Costing172 Questions

Exam 18: Activity-Based Costing and Other Cost Management Tools162 Questions

Exam 19: Cost-Volume-Profit Analysis165 Questions

Exam 20: Short-Term Business Decisions163 Questions

Exam 21: Capital Investment Decisions and the Time Value of Money153 Questions

Exam 22: The Master Budget and Responsibility Accounting157 Questions

Exam 23: Flexible Budgets and Standard Costs166 Questions

Exam 24: Performance Evaluation and the Balanced Scorecard166 Questions

Select questions type

The main difference between activity-based costing and traditional costing systems is that activity-based

costing uses a separate allocation rate for each activity.

(True/False)

4.8/5  (41)

(41)

Internal failure costs occur when the company detects and corrects poor-quality goods or services before delivery to customers.

(True/False)

4.8/5 (31)

The cost to improve equipment and processes comes under which of the following cost categories?

(Multiple Choice)

4.7/5 (41)

Alonzo Company has been experiencing lost sales and high returns recently, so they decided to undertake a comprehensive quality program. Here are factors being considered:

If the cost of implementing the quality program is under $270,000, the company should go forward with it.

If the cost of implementing the quality program is under $270,000, the company should go forward with it.

(True/False)

4.9/5 (36)

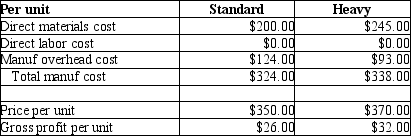

AAA Metal Bearings produces two sizes of metal bearings (sold by the crate)-standard and heavy. The standard bearings require $200 of direct materials per unit (per crate)and the heavy bearings require $245 of direct materials per unit. The operation is mechanized and there is no direct labor. Previously AAA used a single plantwide allocation rate for manufacturing overhead, which was $1.55 per machine hour. Based on the single rate, gross profit data were as follows:

Although the data showed that the heavy bearings were more profitable than the standard bearings, the plant manager knew that the heavy bearings required much more processing in the metal fabrication phase than the standard bearings, and that this factor was not adequately reflected in the single allocation rate. He suspected that it was distorting the profit data. He suggested adopting an activity based costing approach.

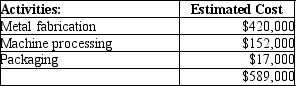

Working together, the engineers and accountants identified the following three manufacturing activities, and broke down the annual overhead costs as shown:

Although the data showed that the heavy bearings were more profitable than the standard bearings, the plant manager knew that the heavy bearings required much more processing in the metal fabrication phase than the standard bearings, and that this factor was not adequately reflected in the single allocation rate. He suspected that it was distorting the profit data. He suggested adopting an activity based costing approach.

Working together, the engineers and accountants identified the following three manufacturing activities, and broke down the annual overhead costs as shown:

Engineers believed that metal fabrication costs should be allocated by weight, and estimated that the plant processed 12,000 kilos of metal per year. Machine processing costs were correlated to machine hours, and the engineers estimated a total of 380,000 machine hours for the year. Packaging costs were the same for both types of products, and so they could be allocated simply by the number of units produced. The production plan provided for 4,000 units of standard and 1,000 units of heavy bearings to be produced during the year. Additional data on a per unit basis are as follows:

Engineers believed that metal fabrication costs should be allocated by weight, and estimated that the plant processed 12,000 kilos of metal per year. Machine processing costs were correlated to machine hours, and the engineers estimated a total of 380,000 machine hours for the year. Packaging costs were the same for both types of products, and so they could be allocated simply by the number of units produced. The production plan provided for 4,000 units of standard and 1,000 units of heavy bearings to be produced during the year. Additional data on a per unit basis are as follows:

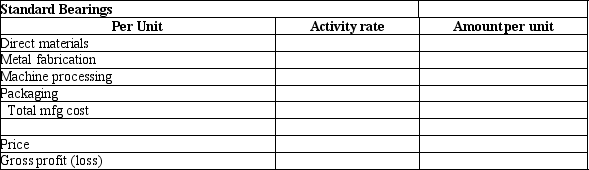

Using the data above, please calculate activity rates. Then, following the ABC methodology, calculate the production cost and gross profit for one unit of heavy bearings, using the format below:

Using the data above, please calculate activity rates. Then, following the ABC methodology, calculate the production cost and gross profit for one unit of heavy bearings, using the format below:

(Essay)

4.7/5 (32)

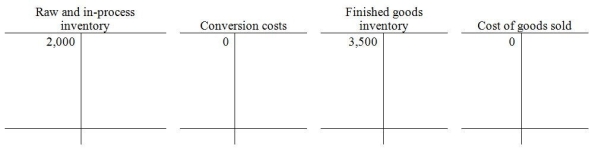

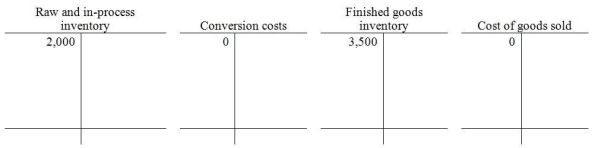

Archetype Fabrication makes pre-stressed concrete forms for the building industry. They use just-in-time production and accounting methodology. At the beginning of January, selected account balances are shown in the T-accounts below.  During January, the following 5 transactions take place:

During January, the following 5 transactions take place:

Use the T-accounts shown above to record the transactions, and then answer the following question:

After transaction number 4, what was the balance in the Raw and in-process inventory account?

Use the T-accounts shown above to record the transactions, and then answer the following question:

After transaction number 4, what was the balance in the Raw and in-process inventory account?

(Multiple Choice)

4.8/5 (36)

Archetype Fabrication makes pre-stressed concrete forms for the building industry. They use just-in-time production and accounting methodology. At the beginning of January, selected account balances are shown in the T-accounts below.  During January, the following 5 transactions take place:

During January, the following 5 transactions take place:

Use the T-accounts shown above to record the transactions, and then answer the following question:

After transaction number 5, what was the balance in the Conversion costs account?

Use the T-accounts shown above to record the transactions, and then answer the following question:

After transaction number 5, what was the balance in the Conversion costs account?

(Multiple Choice)

4.7/5 (35)

Orlando Avionics makes three types of radios for small aircraft-model A, model B, and model C. The manufacturing operations are mechanized and there is no direct labor. Manufacturing overhead costs are significant, and Orlando has adopted an activity-based costing system. Direct materials costs per unit for each model are as follows:  Orlando has three activities-assembly, materials management, and testing. The cost driver for assembly is machine hours. The cost driver for materials management is number of parts, and the cost driver for testing is the number of units of product. Total costs and production volumes for the year 2012 were estimated as follows:

Orlando has three activities-assembly, materials management, and testing. The cost driver for assembly is machine hours. The cost driver for materials management is number of parts, and the cost driver for testing is the number of units of product. Total costs and production volumes for the year 2012 were estimated as follows:

What is the allocation rate for the Assembly activity? (Please round to the nearest cent.)

What is the allocation rate for the Assembly activity? (Please round to the nearest cent.)

(Multiple Choice)

4.8/5 (42)

Just-in-time systems are based on a "demand-pull system" where customer demand triggers the production process.

(True/False)

4.9/5 (38)

Kenney Company uses activity-based costing to account for its manufacturing process. Kenney Company produces tires and each tire has $.50 of direct materials, includes 20 parts and requires 2 hours of machine time. There is no direct labor. Additional information follows:  What is the cost of materials handling per tire?

What is the cost of materials handling per tire?

(Multiple Choice)

4.7/5 (48)

Target costing starts with the price that customers are willing to pay and then subtracts the company's desired profit to determine the desired full-product cost.

(True/False)

4.8/5 (33)

The following four steps are necessary in order to use an activity-based costing system: 1. Compute the allocation rate for each activity.

2. Identify activities and estimate their total costs.

3. Identify the cost driver for each activity and then estimate the quantity of each driver's allocation base.

4. Allocate the indirect costs to the cost object.

In what order are these steps performed?

(Multiple Choice)

4.8/5 (31)

Johnson Production Company uses just-in-time production and accounting methods. On June 1, Johnson purchased $4,000 of raw materials on account. Please provide the journal entry.

(Essay)

4.9/5 (26)

Just-in-time methodology depends on maintaining higher inventory levels to ensure that the manufacturing process isn't interrupted by supply shortages.

(True/False)

4.9/5 (48)

For just-in-time systems, it is essential that manufacturers develop relationships with suppliers that are very reliable, and that can guarantee quick deliveries of materials in small quantities.

(True/False)

4.9/5 (33)

Johnson Production Company uses just-in-time production and accounting methods. On June 1, Johnson paid $6,000 for factory repair and maintenance costs in cash. Please provide the journal entry.

(Essay)

4.8/5 (42)

Kenney Company uses activity-based costing to account for its manufacturing process. Kenney Company produces tires, and each tire has $.50 of direct materials, includes 20 parts and requires 2 hours of machine time. There is no direct labor. Additional information follows:  What is the cost of machining per tire?

What is the cost of machining per tire?

(Multiple Choice)

4.9/5 (35)

Equival Company wishes to sell truck axles to car manufacturers. The current market price of the axles is $400, and Equival knows it must accept the market price. Currently, it costs the company $330 to produce each axle. The company wishes to make a profit equal to 20% of the price. Which of the following strategies should Equival adopt to achieve its objective?

(Multiple Choice)

4.8/5 (36)

Just-in-time systems allow manufacturers to save money on storing, insuring, and financing inventories, by maintaining lower levels of inventory.

(True/False)

4.8/5 (33)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)