Exam 10: Deductions and Losses: Certain Itemized Deductions

Phillip, age 66, developed hip problems and was unable to climb the stairs to reach his second-floor bedroom. His physician advised him to add a first-floor bedroom to his home. The cost of constructing the room was $32,000. The increase in the value of the residence as a result of the room addition was determined to be $17,000. In addition, Phillip paid the contractor $5,500 to construct an entrance ramp to his home and $8,500 to widen the hallways to accommodate his wheelchair. Phillip's AGI for 2017 was $75,000. How much of these expenditures can Phillip deduct as a medical expense in 2017?

C

Al contributed a painting to the Metropolitan Art Museum of St. Louis, Missouri. The painting, purchased six years ago, was worth $40,000 when donated, and Al's basis was $25,000. If this painting is immediately sold by the museum and the proceeds are placed in the general fund, Al's charitable contribution deduction is $25,000 (subject to percentage limitations).

True

Shirley sold her personal residence to Mike for $400,000. Before the sale, Shirley paid the real estate taxes of $7,030 for the calendar year. For income tax purposes, the deduction is apportioned as follows: $4,000 to Shirley and $3,030 to Mike.

a. What is Mike's basis in the residence?

b. What is Shirley's amount realized from the sale of the residence?

c. What amount of real estate taxes can Mike deduct?

d. What amount of real estate taxes can Shirley deduct?

General discussion. For Federal income tax purposes, real estate taxes must be apportioned between the buyer and the seller. The taxes paid by the seller that are apportioned to the buyer affect both the basis of the buyer's property and the amount realized by the seller.

a. Mike's basis in the residence is $396,970 [$400,000 (purchase price) - $3,030 (property taxes allocated to Mike but paid by Shirley)].

b. Shirley's amount realized is $396,970 [$400,000 (sales price) - $3,030 (property taxes allocated to Mike but paid by Shirley)].

c. Mike can deduct the $3,030 apportioned to him, even though the tax was paid by Shirley.

d. Shirley can deduct only the tax apportioned to her of $4,000, even though she paid the entire amount of $7,030.

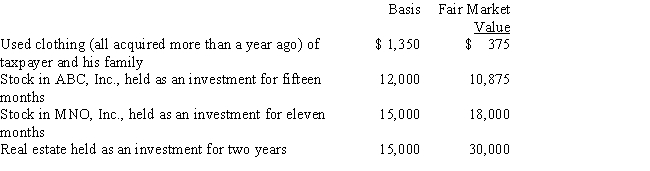

Zeke made the following donations to qualified charitable organizations during the year:

The used clothing was donated to the Salvation Army; the other items of property were donated to Eastern State University. Both are qualified charitable organizations. Disregarding percentage limitations, Zeke's charitable contribution deduction for the year is:

The used clothing was donated to the Salvation Army; the other items of property were donated to Eastern State University. Both are qualified charitable organizations. Disregarding percentage limitations, Zeke's charitable contribution deduction for the year is:

For the past several years, Jeanne and her two sisters have taken turns claiming a dependency exemption deduction for their mother under a multiple support agreement. This year Jeanne will be entitled to the exemption, and her mother needs money for surgery and new eyeglasses. Should Jeanne pay for the medical expenses as her share of her mother's expenses? How would this benefit Jeanne?

A phaseout of certain itemized deductions applies for all taxpayers who choose to itemize their deductions.

Rick and Carol Ryan, married taxpayers, took out a mortgage of $160,000 when purchasing their home ten years ago. In October of the current year, when the home had a fair market value of $200,000 and they owed $125,000 on the mortgage, the Ryans took out a home equity loan for $110,000. They used the funds to purchase a sailboat to be used for recreational purposes. The sailboat does not qualify as a residence. What is the maximum amount of debt on which the Ryans can deduct home equity interest?

Gambling losses may be deducted to the extent of the taxpayer's gambling winnings. Such losses are subject to the 2%-of-AGI floor for miscellaneous itemized deductions.

Edna had an accident while competing in a rodeo. She sustained facial injuries that required cosmetic surgery. While having the surgery done to restore her appearance, she had additional surgery done to reshape her chin, which was not injured in the accident. The surgery to restore her appearance cost $9,000 and the surgery to reshape her chin cost $6,000. How much of Edna's surgical fees will qualify as a deductible medical expense (before application of the 10%-of-AGI floor)?

In the current year, Jerry pays $8,000 to become a charter member of Mammoth University's Athletic Council. The membership ensures that Jerry will receive choice seating at all of Mammoth's home basketball games. Also this year, Jerry pays $2,200 (the regular retail price) for season tickets for himself and his wife. For these items, how much qualifies as a charitable contribution?

Brad, who would otherwise qualify as Faye's dependent, had gross income of $9,000 during the year. Faye, who had AGI of $120,000, paid the following medical expenses in 2017:

Faye has a medical expense deduction of:

Faye has a medical expense deduction of:

In April 2017, Bertie, a calendar year cash basis taxpayer, had to pay the state of Michigan additional income tax for 2016. Even though it relates to 2016, for Federal income tax purposes the payment qualifies as a tax deduction for tax year 2017.

Joe, who is in the 33% tax bracket this year, expects to retire next year and be in the 25% tax bracket. He plans to donate $50,000 to his church. Because he will not have the cash available until next year, Joe donates land (long-term capital gain property) with a basis of $10,000 and fair market value of $50,000 to the church in December of the current year. He reacquires the land for $50,000 in February of next year. Discuss Joe's tax objectives and all tax issues related to his actions.

In order to dissuade his pastor from resigning and taking a position with a larger church, Michael, an ardent leader of the congregation, gives the pastor a new car. The cost of the car is deductible by Michael as a charitable contribution.

Contributions to public charities in excess of 50% of AGI may be carried back 3 years or forward for up to 5 years.

For purposes of computing the deduction for qualified residence interest, a qualified residence includes only the taxpayer's principal residence.

Pat gave 5,000 shares of stock in Coyote Corporation (a publicly traded corporation) to her church (a qualified charitable organization) in the current year. The stock was worth $180,000 and she had acquired it as an investment four years ago at a cost of $120,000. She reported AGI of $300,000 for the year. In completing her current income tax return, how much is her current-year charitable contribution deduction?

Herbert is the sole proprietor of a furniture store. He can deduct real property taxes on his store building as a business deduction but he cannot deduct state income taxes related to his net income from the furniture store as a business deduction.

Personal expenditures that are deductible as itemized deductions include medical expenses, Federal income taxes, state income taxes, property taxes on a personal residence, mortgage interest, and charitable contributions.

Sandra is single and does a lot of business entertaining at home. Because Arthur, Sandra's 80-year old dependent grandfather who lived with Sandra, needs medical and nursing care, he moved to Twilight Nursing Home. During the year, Sandra made the following payments on behalf of Arthur:

Twilight has medical staff in residence. Disregarding the AGI floor, how much, if any, of these expenses qualify for a medical deduction by Sandra?

Twilight has medical staff in residence. Disregarding the AGI floor, how much, if any, of these expenses qualify for a medical deduction by Sandra?

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)