Exam 9: Reporting Foreign Operations

Exam 1: Setting the Stage40 Questions

Exam 2: Intercorporate Equity Investments: an Introduction43 Questions

Exam 3: Business Combinations43 Questions

Exam 3: Appendix A: AIncome Tax Allocation6 Questions

Exam 4: Wholly Owned Subsidiaries: Reporting Subsequent Acquisitions40 Questions

Exam 4: Appendix A: Wholly Owned Subsidiaries: Reporting Subsequent Acquisitions4 Questions

Exam 4: Appendix B: Wholly Owned Subsidiaries: Reporting Subsequent Acquisitions6 Questions

Exam 5: Consolidation of Non-Wholly Owned Subsidiaries41 Questions

Exam 5: Appendix A: Step Purchases6 Questions

Exam 5: Appendix B: Decreases in Ownership Interest4 Questions

Exam 6: Subsequent-Year Consolidations: General Approach40 Questions

Exam 6: Appendix A: Preferred and Restricted Shares of Investee Corporation5 Questions

Exam 6: Appendix B: Intercompany Bond Holdings6 Questions

Exam 7: Segment and Interim Reporting41 Questions

Exam 8: Foreign Currency Transactions and Hedges49 Questions

Exam 9: Reporting Foreign Operations44 Questions

Exam 10: Financial Reporting for Not-For-Profit Organizations46 Questions

Exam 10: Appendix A: Fund Accounting5 Questions

Exam 11: Public Sector Financial Reporting44 Questions

Select questions type

ISP has a wholly owned subsidiary in China. This subsidiary is self-sufficient and does not rely on ISP for financing and sales. How should foreign exchange gains on translation of the subsidiary's statements to Canadian dollars be reported on ISP's consolidated financial statements?

Free

(Multiple Choice)

4.8/5  (38)

(38)

Correct Answer: Verified

Verified

A

What does a funds-flow statement measure?

Free

(Multiple Choice)

4.9/5 (27)

Correct Answer:Verified

B

A company has translated its foreign subsidiary's financial statements using the temporal method. What is the accounting treatment for exchange gains and losses arising from previous years?

Free

(Multiple Choice)

4.8/5 (30)

Correct Answer:Verified

D

If a foreign currency is strengthening with respect to the Canadian dollar, which of the following is true?

(Multiple Choice)

4.8/5 (30)

Under the temporal method, which of the following items would be translated using the historical rate?

(Multiple Choice)

4.9/5 (42)

For consolidation purposes, what exchange rate is used for converting the retained earnings of a foreign subsidiary into Canadian dollars under the current rate method?

(Multiple Choice)

4.9/5 (36)

When it is not clear what the functional currency is, an accountant must use professional judgment to choose the functional currency. What is the main criterion upon which the choice should be based?

(Multiple Choice)

4.8/5 (42)

Under the current-rate method, which of the following items would be translated using the historical rate?

(Multiple Choice)

4.9/5 (33)

All of the following statements are stated in Brazil reals (R$).  Additional information:

Selected exchange rates:

June 30,20\times4 =\ 0.5906 June 30,20\times5 =\ 0.5623 Average for 20\times5 S1=\ 0.5744 Date of purchase of inventory on hand at year-end Dividends were declared on June 30, 20X5 Opening inventory = R$130,000

Inventory purchases for the year = R$1,570,000

Machinery, land, and buildings were purchased on June 30, 20X4

-

Bralta is the Brazilian subsidiary of Altapro Co., a Canadian company. What is the balance of total assets under the temporal method?

Additional information:

Selected exchange rates:

June 30,20\times4 =\ 0.5906 June 30,20\times5 =\ 0.5623 Average for 20\times5 S1=\ 0.5744 Date of purchase of inventory on hand at year-end Dividends were declared on June 30, 20X5 Opening inventory = R$130,000

Inventory purchases for the year = R$1,570,000

Machinery, land, and buildings were purchased on June 30, 20X4

-

Bralta is the Brazilian subsidiary of Altapro Co., a Canadian company. What is the balance of total assets under the temporal method?

(Multiple Choice)

4.8/5 (42)

A Canadian company has three subsidiaries that operate autonomously in Asia. What is the most appropriate alternative for handling translation gains and losses?

(Multiple Choice)

4.8/5 (34)

On January 1, 20X7, Clock Inc. of Vancouver purchased 75% of the outstanding shares of Time Limited in London, England. Time Limited's statements of financial position and statements of comprehensive income and changes in equity-retained earnings section for the year ended December 31, 20X7, are below. \begin{array}{c} \text {Time Limited}\\ \text {Statement of Financial Position}\\ \text {December 31, 20X7}\\ \text {(in thousands of £^{\prime} s )}\\\\\begin{array}{|l|r|}\hline \text { Assets } & £ \\\hline \text { Cash } & 50 \\\hline \text { Accounts receivable } & 575 \\\hline \text { Inventories } & 825 \\\hline \text { Equipment, net } & \underline{2,670} \\\hline \text { Total assets } & \underline{4.120} \\\hline\\\hline\text { Liabilities }\\\hline \text { Accounts payable } & 465 \\\hline \text { Bonds payable } & 1,290 \\\hline \text { Common shares } & 1,200 \\\hline \text { Retained earnings } & \underline{1,165} \\\hline \text { Total liabilities and shareholders' equity } & \underline{4,120}\\\hline\end{array}\end{array} Time Limited Statement of Comprehensive Income Year Ended December 31, 20 X 7 (in thousands of s ) £ Sales 2,170 Cost of goods sold 1,203 Depreciation expense 267 Interest expense 80 Other expenses Comprehensive income \begin{array}{c}\text { Time Limited}\\\text { Statement of Changes in Equity-Partial-Retained earnings section}\\\text { Year Ended December 31, 20X7}\\\text { (in thousands of £^{\prime} s)}\\\\\begin{array}{|l|r|}\hline&£\\ \hline \text { Retained earnings-January } 1,20 \times 7 & 1,002 \\\hline \text { Comprehensive income for the year } & 213 \\\hline \text { Dividends paid } & (\underline{50}) \\\hline \text { Retained earnings-December 31, 20X7 } &\underline{ 1,165} \\\hline\end{array}\end{array}

Additional information:

1. Time was incorporated on January 1, 20X3, when it acquired all its equipment for £4,005,000 and issued its 10-year bonds payable.

2. Time's purchases and sales occurred evenly over the year. Inventories on hand at December 31, 20X6, and December 20X7 were purchased evenly over the last quarter of 20X6 and 20X7, respectively. Inventories as at December 31, 20X7, were £650,000.

3. Dividends were paid on March 31, 20X7. There were no changes in share capital over the year.

4. Foreign exchange rates are as follows:

January 1,20X3 £1=C \1 .95 Average for Oct to Dec, 20X6 £1=C \1 .64 Average for 20X6 £1=C \1 .73 December 31,20X6/ January 1, 20X7 £1=C\ 1.67 March 31, 20X7 £1=C\ 1.61 Average for Oct to Dec, 20X7 £1=C\ 1.55 Average for 20X7 £1=C\ 1.57 December 31.20X7 £1=C\ 1.52 Required:

Translate Time's statement of financial position at December 31, 20X7, into Canadian dollars, assuming its functional currency is British pound sterling. Include a calculation to prove the amount of the cumulative foreign exchange translation gains and losses.

(Essay)

4.9/5 (29)

Under the temporal method, which of the following items would be translated using the year-end spot rate?

(Multiple Choice)

4.8/5 (44)

On January 1, 20X6, Clock Inc. of Vancouver purchased 75% of the outstanding shares of Time Limited in London, England. Time Limited's statements of financial position and statements of comprehensive income and changes in equity-retained earnings section for the year ended December 31, 20X7, are below. \begin{array}{c}\text { Time Limited}\\\text { Statement of Financial Position}\\\text { December 31, 20X7}\\\text { (in thousands of £^{\prime} s )}\\\\\begin{array}{|l|r|r|}\hline \text { Assets } & 20 \times 7 & 20 \times 6 \\\hline \text { Cash } & 50 & 20 \\\hline \text { Accounts receivable } & 575 & 280 \\\hline \text { Inventories } & 825 & 650 \\\hline \text { Equipment, net } & \underline{2,670} & \underline{2,937} \\\hline \text { Total assets } & \underline{4,120} & \underline{3, 887 }\\\hline\\\hline \text { Liabilities } & & \\\hline \text { Accounts payable } & 465 & 395 \\\hline \text { Bonds payable } & 1,290 & 1,290 \\\hline \text { Common shares } & 1,200 & 1,200 \\\hline \text { Retained earnings } & \underline{1,165} & \underline{1,002} \\\hline \text { Total liabilities and shareholders' equity } & \underline{4,120} & \underline{3,887} \\\hline\end{array}\end{array}

\begin{array}{c}\text { Time Limited}\\\text { Statement of Comprehensive Income}\\ \text { Year Ended December 31, 20X7}\\\text { (in thousands of £^{\prime} s )}\\\\\begin{array}{|l|r|}\hline & £ \\\hline \text { Sales } & \underline{2,170} \\\hline \text { Cost of goods sold } & 1,203 \\\hline \text { Depreciation expense } & 267 \\\hline \text { Interest expense } & 80 \\\hline \text { Other expenses } & 407 \\\hline & \underline{1,957} \\\hline \text { Comprehensive income } & 213\\\hline\end{array}\end{array}

\begin{array}{c}\text {Time Limited}\\\text {Statement of Changes in Equity-Partial-Retained earnings section}\\\text {Year Ended December 31, 20X7}\\\text {(in thousands of £ ^{\prime} s )}\\\\\begin{array}{|l|r|}\hline & £ \\\hline \text { Retained earnings-January } 1,20X7 & 1,002 \\\hline \text { Comprehensive income for the year } & 213 \\\hline \text { Dividends paid } & (50) \\\hline \text { Retained earnings - December } 31,20X7 & 1,165\\\hline\end{array}\end{array}

Additional information:

1. Time was incorporated on January 1, 20X3, when it acquired all its equipment for £4,005,000 and issued its 10-year bonds payable.

2. Time's purchases and sales occurred evenly over the year. Inventories on hand at December 31, 20X6, and December 20X7 were purchased evenly over the last quarter of 20X6 and 20X7, respectively. Inventories as at December 31, 20X7, were £650,000.

3. Dividends were paid on March 31, 20X7.

4. Foreign exchange rates are as follows:

January 1,20X3 £1=C\ 1.95 January 1, 20X6 £1=C\ 1.85 Average for Oct to Dec, 20X6 £1=C\ 1.64 Average for 20X6 £1=\ 1.73 December 31,20X6/ January 1,20X7 £1=C\ 1.67 March 31,20X7 £1=C\ 1.61 Average for Oct to Dec, 20X7 £1=C\ 1.55 Average for 20X7 £1=C\ 1.57 December 31.20X7 £1=C\ 1.52

Required:

Translate Time's statement of comprehensive income for the year ended December 31, 20X7 into Canadian dollars assuming its functional currency is Canadian dollars. Calculate the translation gain or loss arising in 20X7.

(Essay)

4.9/5 (45)

Under the current-rate method, at what exchange rate is depreciation expense translated?

(Multiple Choice)

4.9/5 (35)

All of the following statements are stated in Brazil reals (R$). Additional information:

Selected exchange rates:

June 30,20\times4 =\ 0.5906 June 30,20\times5 =\ 0.5623 Average for 20\times5 S1=\ 0.5744 Date of purchase of inventory on hand at year-end Dividends were declared on June 30, 20X5 Opening inventory = R$130,000

Inventory purchases for the year = R$1,570,000

Machinery, land, and buildings were purchased on June 30, 20X4

-

Bralta is the Brazilian subsidiary of Altapro Co., a Canadian company. Bralta had net assets at June 30, 20X4, of R$1,100,000. What is the cost of sales under the temporal method?

(Multiple Choice)

4.8/5 (37)

DNA was incorporated on January 2, 20X0, and commenced active operations immediately. Common shares were issued on the date of incorporation and no new common shares have been issued since then. On December 31, 20X3, INT purchased 70% of the outstanding common shares of DNA for 800,000 Swedish Krona (SEK).

DNA's main operations are located in Switzerland. For the year ending December 31, 20X6, the income statement (in 000s)for DNA was as follows:

Sales SEK 1,625 Cost of goods sold (1,200) Depreciation expense (75) Income tax expense-current Net income SEK The comparative and condensed statements of financial position (in 000s)for DNA were as follows:

20X6 20X5 Accounts receivable SEK 400 SEK 385 Inventory 200 90 Property, plant, and equipment - net Total SEK SEK Accounts payable SEK 90 SEK 85 Other current monetary liabilities 200 250 Common shares 1,250 1,250 Retained earnings (Note 3) SEK Total SEK SEK

OTHER INFORMATION:

• Purchases and sales of merchandise inventory occurred evenly throughout the year.

• The ending inventory was purchased evenly throughout the last month of the year.

• DNA purchased the property, plant, and equipment on hand at the end of 20X6 on March 17, 20X1. There were no purchases or sales of these assets from 20X3 to 20X6.

• Dividends were paid on June 30, 20X6.

Assume that foreign exchange rates were as follows:

January 2,20\times0 \ 1= SEK 2.30 March 17,20\times1 \ 1= SEK 2.60 December 31,20\times3 \ 1= SEK 2.70 Average for 20\times5 \ 1= SEK 2.90 Average for quarter 4 for 20\times5 \ 1= SEK 3.00 Average for December 20\times5 \ 1= SEK 3.10 December 31,20\times5 \ 1= SEK 3.30 June 30,20\times6 \ 1= SEK 3.60 Average for 20\times6 \ 1= SEK 3.50 Average for quarter 4 for 20\times6 \ 1= SEK 3.70 Average for December 20\times6 \ 1= SEK 3.80 December 31.20\times6 \ 1= SEK 3.90

- DNA's financial statements need to be translated into Canadian dollars for consolidation with INT's financial statements.

Required:

Translate DNA's statement of financial position at December 31, 20X6, into Canadian dollars under the temporal method.

(Essay)

4.9/5 (29)

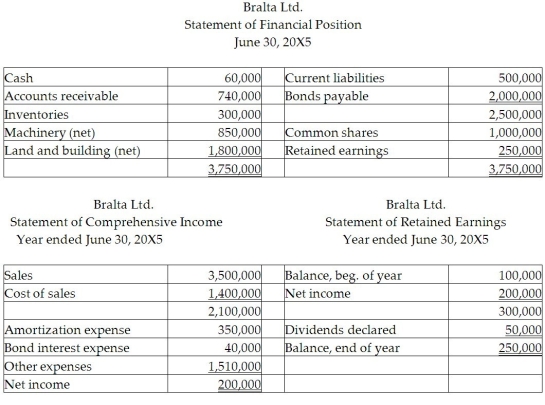

All of the following statements are stated in Brazil reals (R$). Bralta Ltd.

Statement of Financial Position

Iune Cash 60,000 Current liabilities 500,000 Accounts receivable 740,000 Bonds payable Inventories 300,000 2,500,000 Machinery (net) 850,000 Common shares 1,000,000 Land and building (net) Retained earnings Additional information:

Selected exchange rates:

June 30,20X4 R \ 1=\ 0.5906 June 30,20X5 R \ 1=\ 0.5623 Average for 20X5 R \ 1=\ 0.5744

Dividends were declared on June 30, 20X5

Opening inventory = R$130,000

Inventory purchases for the year = R$1,570,000

Machinery, land, and buildings were purchased on June 30, 20X4

Bralta is the Brazilian subsidiary of Altapro Co., a Canadian company.

-Under the current-rate method, what is the translation gain or loss?

(Multiple Choice)

4.8/5 (28)

Under the current-rate method, what is the accounting treatment for exchange gains and losses arising from the current year?

(Multiple Choice)

4.9/5 (37)

For publicly accountable companies, with foreign operations in countries with a hyper-inflationary economy, what should be done prior to translation?

(Multiple Choice)

4.8/5 (36)

LaSalle Ltd., a Canadian company, has a subsidiary in Brazil that produces a component used in LaSalle's manufacturing. All of the components that the subsidiary produces are sold to LaSalle. The subsidiary also purchases most of the raw materials used in its production from LaSalle. Both companies use the Canadian dollar as their functional currency. Which of the following statements is true?

(Multiple Choice)

4.8/5 (36)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)