Exam 4: Appendix A: Wholly Owned Subsidiaries: Reporting Subsequent Acquisitions

Exam 1: Setting the Stage40 Questions

Exam 2: Intercorporate Equity Investments: an Introduction43 Questions

Exam 3: Business Combinations43 Questions

Exam 3: Appendix A: AIncome Tax Allocation6 Questions

Exam 4: Wholly Owned Subsidiaries: Reporting Subsequent Acquisitions40 Questions

Exam 4: Appendix A: Wholly Owned Subsidiaries: Reporting Subsequent Acquisitions4 Questions

Exam 4: Appendix B: Wholly Owned Subsidiaries: Reporting Subsequent Acquisitions6 Questions

Exam 5: Consolidation of Non-Wholly Owned Subsidiaries41 Questions

Exam 5: Appendix A: Step Purchases6 Questions

Exam 5: Appendix B: Decreases in Ownership Interest4 Questions

Exam 6: Subsequent-Year Consolidations: General Approach40 Questions

Exam 6: Appendix A: Preferred and Restricted Shares of Investee Corporation5 Questions

Exam 6: Appendix B: Intercompany Bond Holdings6 Questions

Exam 7: Segment and Interim Reporting41 Questions

Exam 8: Foreign Currency Transactions and Hedges49 Questions

Exam 9: Reporting Foreign Operations44 Questions

Exam 10: Financial Reporting for Not-For-Profit Organizations46 Questions

Exam 10: Appendix A: Fund Accounting5 Questions

Exam 11: Public Sector Financial Reporting44 Questions

Select questions type

Which of the following statements is true with respect to adjusting the deferred tax account on consolidation?

Free

(Multiple Choice)

4.9/5  (30)

(30)

Correct Answer: Verified

Verified

C

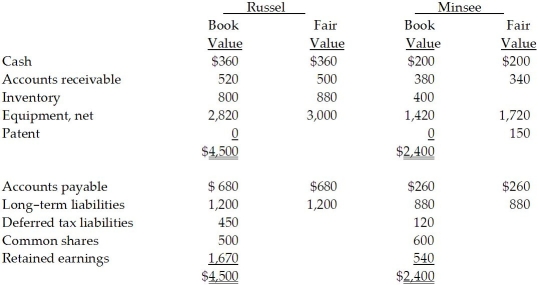

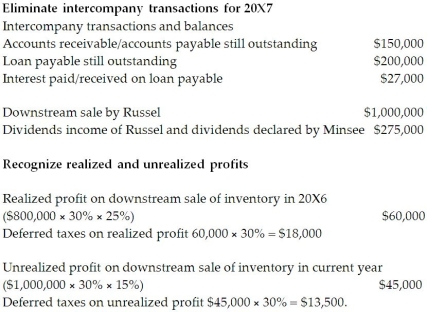

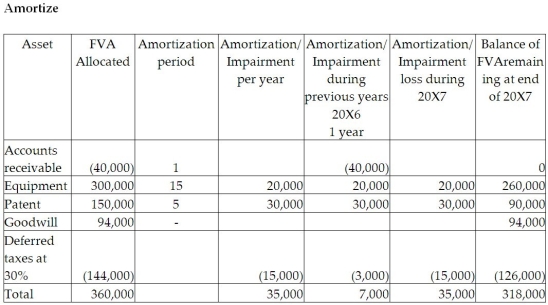

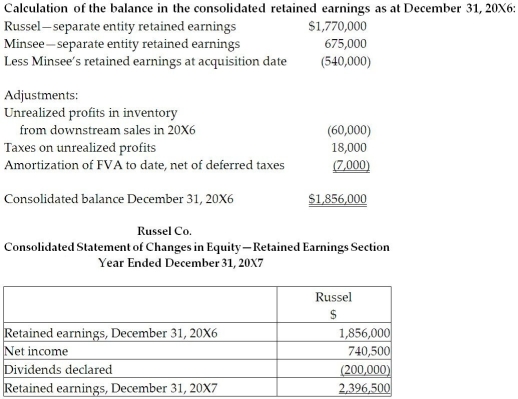

On December 31, 20X5, Russel Co. purchased 100% of the outstanding common shares of Minsee Ltd. for $1,300,000 in shares and $200,000 in cash. The statements of financial position of Russel and Minsee immediately before the acquisition and issuance of the notes payable were as follows (in 000s):  The tax value for each asset and liability is the same as its carrying value except for the equipment, which has a tax value of $950,000, and the patent, which has a tax value of nil. The equipment has a remaining useful life of 15 years from the date of acquisition. The patent has a useful life estimated to be five years from the date of acquisition.

During 20X6, the year following the acquisition, the following occurred:

1. Minsee borrowed $350,000 from Russel on June 1, 20X6, and was charged interest at 10% per annum, which it paid on a monthly basis. There were no repayments of principal made during the remaining of the year.

2. Throughout the year, Minsee purchased merchandise of $800,000 from Russel. Russel's gross margin is 30% of selling price. At December 31, 20X6, Minsee still owed Russel $250,000 on this merchandise; 75% of this merchandise was resold by Minsee prior to December 31, 20X6.

3. Minsee paid dividends of $275,000 at the end of 20X6 and Russel paid dividends of $200,000.

4. Minsee and Russel both have an income tax rate of 30%.

During 20X7, the following occurred:

1. Minsee paid $150,000 on the loan payable to Russel on May 30, 20X7.

2. Throughout the year, Minsee purchased merchandise of $1,000,000 from Russel. Russel's gross margin is 30% of selling price. At December 31, 20X6, Minsee still owed Russel $150,000 on this merchandise; 85% of this merchandise was resold by Minsee prior to December 31, 20X7.

3. Minsee paid dividends of $275,000 at the end of 20X7 and Russel paid dividends of $200,000.

4. Minsee and Russel both have an income tax rate of 30%.

The tax value for each asset and liability is the same as its carrying value except for the equipment, which has a tax value of $950,000, and the patent, which has a tax value of nil. The equipment has a remaining useful life of 15 years from the date of acquisition. The patent has a useful life estimated to be five years from the date of acquisition.

During 20X6, the year following the acquisition, the following occurred:

1. Minsee borrowed $350,000 from Russel on June 1, 20X6, and was charged interest at 10% per annum, which it paid on a monthly basis. There were no repayments of principal made during the remaining of the year.

2. Throughout the year, Minsee purchased merchandise of $800,000 from Russel. Russel's gross margin is 30% of selling price. At December 31, 20X6, Minsee still owed Russel $250,000 on this merchandise; 75% of this merchandise was resold by Minsee prior to December 31, 20X6.

3. Minsee paid dividends of $275,000 at the end of 20X6 and Russel paid dividends of $200,000.

4. Minsee and Russel both have an income tax rate of 30%.

During 20X7, the following occurred:

1. Minsee paid $150,000 on the loan payable to Russel on May 30, 20X7.

2. Throughout the year, Minsee purchased merchandise of $1,000,000 from Russel. Russel's gross margin is 30% of selling price. At December 31, 20X6, Minsee still owed Russel $150,000 on this merchandise; 85% of this merchandise was resold by Minsee prior to December 31, 20X7.

3. Minsee paid dividends of $275,000 at the end of 20X7 and Russel paid dividends of $200,000.

4. Minsee and Russel both have an income tax rate of 30%.

Required:

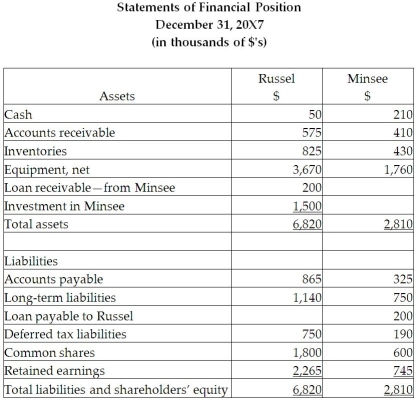

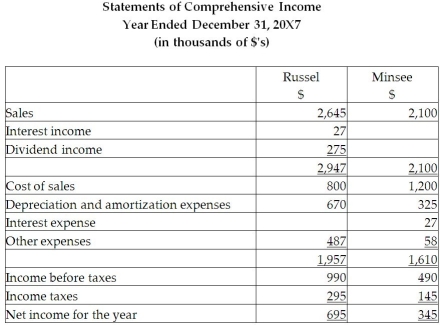

Calculate the consolidated retained earnings as at December 31, 20X7, and as at December 31, 20X6.

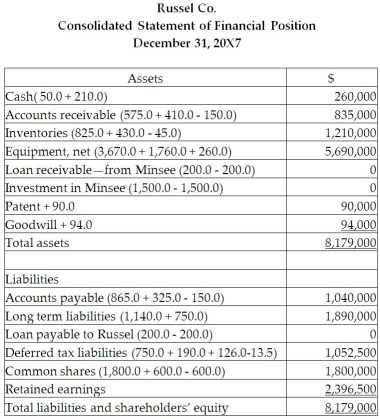

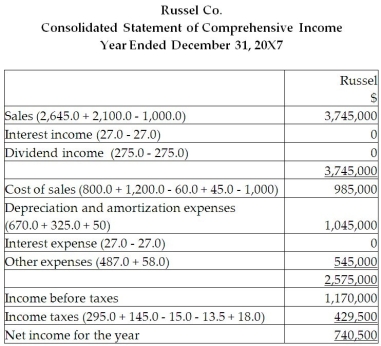

Prepare the consolidated statement of comprehensive income and the consolidated statement of financial position for the year ended December 31, 20X7, for Russel. Include all relevant income tax calculations.

Required:

Calculate the consolidated retained earnings as at December 31, 20X7, and as at December 31, 20X6.

Prepare the consolidated statement of comprehensive income and the consolidated statement of financial position for the year ended December 31, 20X7, for Russel. Include all relevant income tax calculations.

Free

(Essay)

4.7/5 (35)

Correct Answer:Verified

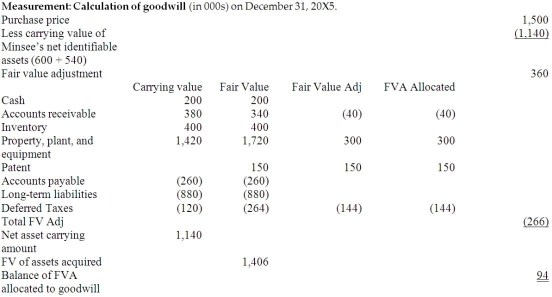

Calculation of the balance in the consolidated retained earnings as at December :

Calculation of the balance in the consolidated retained earnings as at December :

Morin Co. acquired all the shares of Lightfoot Ltd. Lightfoot has a number of amortizable capital assets and has properly recorded the related deferred income taxes on its books.

- What deferred income tax adjustment must Morin make for its consolidated financial statements?

Free

(Multiple Choice)

5.0/5 (38)

Correct Answer:Verified

B

Morin Co. acquired all the shares of Lightfoot Ltd. Lightfoot has a number of amortizable capital assets and has properly recorded the related deferred income taxes on its books.

- At the time of acquisition, the fair values of these assets were higher than their carrying values and their tax bases. In Morin's consolidation each year, it must adjust for the deferred taxes that resulted from these temporary differences. Which of the following statements is true?

(Multiple Choice)

4.8/5 (35)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)