Exam 6: Subsequent-Year Consolidations: General Approach

Exam 1: Setting the Stage40 Questions

Exam 2: Intercorporate Equity Investments: an Introduction43 Questions

Exam 3: Business Combinations43 Questions

Exam 3: Appendix A: AIncome Tax Allocation6 Questions

Exam 4: Wholly Owned Subsidiaries: Reporting Subsequent Acquisitions40 Questions

Exam 4: Appendix A: Wholly Owned Subsidiaries: Reporting Subsequent Acquisitions4 Questions

Exam 4: Appendix B: Wholly Owned Subsidiaries: Reporting Subsequent Acquisitions6 Questions

Exam 5: Consolidation of Non-Wholly Owned Subsidiaries41 Questions

Exam 5: Appendix A: Step Purchases6 Questions

Exam 5: Appendix B: Decreases in Ownership Interest4 Questions

Exam 6: Subsequent-Year Consolidations: General Approach40 Questions

Exam 6: Appendix A: Preferred and Restricted Shares of Investee Corporation5 Questions

Exam 6: Appendix B: Intercompany Bond Holdings6 Questions

Exam 7: Segment and Interim Reporting41 Questions

Exam 8: Foreign Currency Transactions and Hedges49 Questions

Exam 9: Reporting Foreign Operations44 Questions

Exam 10: Financial Reporting for Not-For-Profit Organizations46 Questions

Exam 10: Appendix A: Fund Accounting5 Questions

Exam 11: Public Sector Financial Reporting44 Questions

Select questions type

Basil Ltd. has an 80% interest in a joint venture. Under IFRS, what is attributed to the Basil?

Free

(Multiple Choice)

4.8/5  (39)

(39)

Correct Answer: Verified

Verified

B

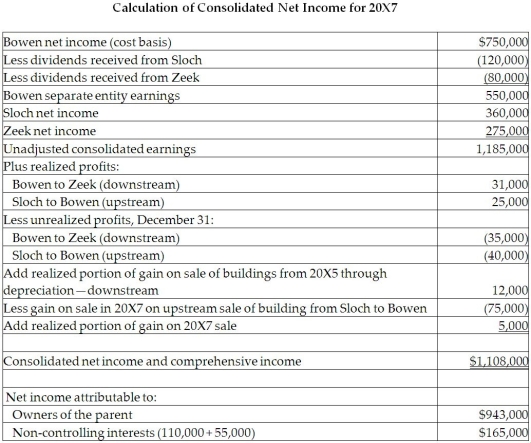

Bowen Limited purchased 60% of Sloch Co. when Sloch's reported retained earnings were $330,000. Bowen also owns 80% in Zeek Limited, which was purchased when Zeek reported retained earnings of $575,000. For each acquisition, the purchase price was equal to the fair value of the identifiable net assets, which was the same as the carrying value of their carrying values.

An analysis of the changes in retained earnings of the three companies during the year 20X7 gives the following results: Bowen Sloch Zeek Retained earnings -January 1, 20X7 \ 1,020,000 \ 525,000 \ 875,000 Net income for the year 750,000 360,000 275,000 Dividends paid (500,000) (200,000) (100,000) Retained earnings - December 31,20X7 \ 1,270,000 Sloch sells product to Bowen that is used in Bowen's production. Bowen will then sell part of its products to Zeek.

Intercompany profits on sales from Sloch to Bowen were $25,000 included in January 1, 20X7, inventory, and $40,000 included in December 31, 20X7, inventory.

Intercompany profits included on sales from Bowen to Zeek were $31,000 included in January 1, 20X7, inventory, and $35,000 included in December 31, 20X7 inventory.

During 20X5, Bowen sold a building to Zeek for a gain of $300,000. The building had a remaining life of 25 years. During 20X7, Sloch sold a building to Bowen for a gain of $75,000. This building has a useful remaining life of 15 years. Full depreciation was recorded in the year of acquisition by each company and no depreciation was recorded in the year of sale.

Required:

Calculate the consolidated net income for the year ended December 31, 20X6. Determine the allocation between the NCI and owners of the parent.

Free

(Essay)

4.7/5 (29)

Correct Answer:Verified

Realized and unrealized profits

20X5-Unrealized sale of building downstream sale $300,000

Excess depreciation each year $300,000/25 = $12,000 annually

20X7-Unrealized sale of building upstream sale $75,000 (Sloch to Bowen)

Excess depreciation each year $75,000/15 = $5,000 annually

Intercompany dividends:

Sloch dividends paid $200,000; $120,000 paid to Bowen (60%)

Zeek dividends paid $100,000; $80,000 paid to Bowen (80%)  Non-controlling interests for Sloch: 40% ×$275,000 ($360,000 +25,000-40,000-75,000+5,000)= 110,000

Non-controlling interests for Sloch: 40% ×$275,000 ($360,000 +25,000-40,000-75,000+5,000)= 110,000

Non-controlling interests for Zeek: 20% × $275,000 = $55,000

Total non-controlling interests: $165,000

Grayson Ltd. acquired 60% of the outstanding common shares of Goldberg Ltd. for $480,000. At the date of acquisition, Goldberg's shareholders' equity was $625,000. The goodwill at 100% has been determined to be $90,000 under the entity method.

- What is the amount of Goldberg's fair value increments?

Free

(Multiple Choice)

4.9/5 (39)

Correct Answer:Verified

C

Lobes Co. owns 65% of Banes Limited. During 20X5, Banes sold equipment to Lobes for a gain of $150,000, recognizing a gain on sale (before taxes)of $75,000. Lobes determined that the equipment had a useful life of 10 years, and took a full year's deprecation in 20X5. On April 1, 20X8, Lobes sold the equipment to an unaffiliated company for $110,000. Ignore any taxes.

Required:

Prepare the appropriate consolidation adjustments relating to the equipment for each year ending December 31, 20X5, to 20X8.

(Essay)

4.9/5 (30)

Dixon Ltd. owns 60% of the common shares of Kelly Co. At the beginning of 20X1, Kelly sold a machine with a book value of $350,000 to Dixon for $410,000. When Dixon prepares its consolidated financial statements for 20X1, it credits the machine account by $60,000. What account(s)should it debit in this journal entry?

(Multiple Choice)

4.9/5 (41)

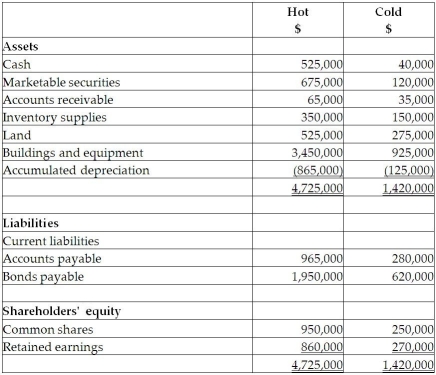

On September 1, 20X5, Hot Limited decided to buy 80% of the shares outstanding of Cold Inc. for $850,000. Hot paid for this acquisition by using cash of $500,000 and marketable securities for the remaining amount. The balances showing on the statement of financial position for the two companies at August 31, 20X5, are as follows:  After a review of the financial assets and liabilities, Hot determines that some of the assets of Cold have fair values different from their carrying values. These items are listed below:

• Inventory has a fair value of $130,000.

• The building has a fair value of $1,090,000. The remaining useful life of the building is 20 years.

• A trademark has a fair value of $300,000. The trademark is estimated to have a useful life of 15 years.

• The bonds payable have a fair value of $720,000 and are due on August 31, 20X9.

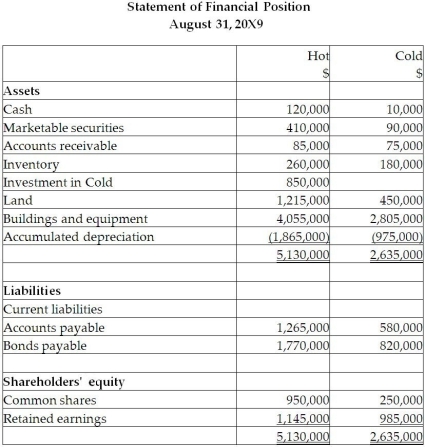

During the 20X9 fiscal year, the following events occurred:

1. Hot sold merchandise to Cold for $200,000. Profit margin on these sales was 30%. Cold still has inventory on hand of $70,000. Included in the opening inventory of Cold for 20X9 is merchandise purchased from Hot in 20X8 for $150,000. The gross profit margin on these sales was 30%

2. Cold sold merchandise to Hot for $500,000. The gross margin on these sales was 40%. At the end of the year, $180,000 of this was still in Hot's inventory and Hot still owed $100,000 on these sales. Included in the opening inventory of Hot for 20X9 was merchandise purchased from Cold in 20X8 for $230,000. The profit margin on these sales was 30%.

3. During 20X9, Cold sold to Hot equipment resulting in a gain to Cold of $75,000. At the time, the original cost and accumulated depreciation to date for the equipment on Cold's books were $510,000 and 160,000. The remaining useful life for this equipment is 15 years. Depreciation is fully recorded in the year of purchase, and no depreciation is recorded in the year of disposal by both companies.

4. During 20X9, Cold paid management fees of $450,000 to Hot.

5. During 20X9, Cold paid dividends of $400,000 and Hot paid dividends of $600,000.

After a review of the financial assets and liabilities, Hot determines that some of the assets of Cold have fair values different from their carrying values. These items are listed below:

• Inventory has a fair value of $130,000.

• The building has a fair value of $1,090,000. The remaining useful life of the building is 20 years.

• A trademark has a fair value of $300,000. The trademark is estimated to have a useful life of 15 years.

• The bonds payable have a fair value of $720,000 and are due on August 31, 20X9.

During the 20X9 fiscal year, the following events occurred:

1. Hot sold merchandise to Cold for $200,000. Profit margin on these sales was 30%. Cold still has inventory on hand of $70,000. Included in the opening inventory of Cold for 20X9 is merchandise purchased from Hot in 20X8 for $150,000. The gross profit margin on these sales was 30%

2. Cold sold merchandise to Hot for $500,000. The gross margin on these sales was 40%. At the end of the year, $180,000 of this was still in Hot's inventory and Hot still owed $100,000 on these sales. Included in the opening inventory of Hot for 20X9 was merchandise purchased from Cold in 20X8 for $230,000. The profit margin on these sales was 30%.

3. During 20X9, Cold sold to Hot equipment resulting in a gain to Cold of $75,000. At the time, the original cost and accumulated depreciation to date for the equipment on Cold's books were $510,000 and 160,000. The remaining useful life for this equipment is 15 years. Depreciation is fully recorded in the year of purchase, and no depreciation is recorded in the year of disposal by both companies.

4. During 20X9, Cold paid management fees of $450,000 to Hot.

5. During 20X9, Cold paid dividends of $400,000 and Hot paid dividends of $600,000.  Required:

Prepare the consolidated statement of financial position for Hot at August 31, 20X9. Calculate the closing balance for the retained earnings and the non-controlling interest. The company used the entity method to determine goodwill for this acquisition.

Required:

Prepare the consolidated statement of financial position for Hot at August 31, 20X9. Calculate the closing balance for the retained earnings and the non-controlling interest. The company used the entity method to determine goodwill for this acquisition.

(Essay)

4.8/5 (29)

Prawn Corporation owns 80% of the outstanding voting shares of Shrimp Corporation, having acquired its interest January 1, 20X3, for $100,000. At the time of the acquisition, Shrimp Corporation had a shareholders' equity totalling $50,000, made up for retained earnings of $30,000 and common shares of $20,000. The following accounts had fair values higher (or lower)than its carrying values:

Inventory fair value is higher than carrying value.

Equipment fair value is higher than carrying value

Land fair value is lower than carrying value. The equipment had a remaining useful life at the time of acquisition of five years.

The company uses the entity approach to determine the amount of goodwill. Prawn accounts for its investment in Shrimp using the cost method.

Statement of Comprehensive Income

Year Ended December 3,

(In thousands of s) Prawn Shrimp Sales \ 600 \ 250 Gain on sale of land and buildings 70 Dividend income Total revenue Cost of goods sold 380 134 Operating expenses Total expenses Net Income

Statement of Changes in Equity-Partial-Retained Earnings section

Year Ended December 3,20X6

(In thousands of s) Prawn Shrimp Opening retained earnings \ 400 \ 100 Net income 96 106 Dividends Ending retained eamings The balance of the land and buildings at December 31, 20X6, for Prawn totalled $895,000 and for Shrimp totalled $450,000.

Additional Information:

1. Shrimp had reported a gain of $50,000, relating to land (40%)and building (60%)sold to Prawn on January 3, 20X6. These separate properties had not been owned on January 1, 20X3. Remaining useful life was expected to be 10 years at that time.

2. Shrimp sold other land to a non-related company at a gain of $20,000 on June 30, 20X6.

3. Intercompany sales and inventory data for 20X5 and 20X6:

\ 20X5 \ 20X6 Sales by Prawn to Shrimp \ 40,000 \ 60,000 Inventory not yet sold at end of year \ 20,000 \ 35,000 Sales by Shrimp to Prawn \ 50,000 \ 50,000 Inventory not yet sold at end of year \ 10,000 \ 40,000

Profit margins on sales by Prawn to Shrimp are 40%.

Profit margins on sales by Shrimp to Prawn are at 30%.

Required:

Calculate the following consolidated balance as at December 31, 20X6:

a. Retained earnings

b. Land and buildings

(Essay)

4.8/5 (38)

A few years ago, Locke Ltd. purchased a machine from its wholly owned subsidiary, Dubois Ltd., for $90,000. Locke has just sold the machine to an unrelated party for a $15,000 gain. At the time of the sale, there was still an unrealized gain of $50,000 from the purchase from Dubois. With this sale of the asset to the unrelated party, what is the amount of gain that should be recognized on Locke's consolidated financial statements?

(Multiple Choice)

4.9/5 (42)

Cooper Ltd. acquired 70% of the common shares of Effy Ltd. at January 2, 20X1. At December 31, 20X3, Effy sold a machine to Cooper for $180,000. Effy had purchased the machine a few years earlier for $250,000. At the time of sale to Cooper, the machine had a carrying value of $150,000 and a remaining useful life of six years.

- Both companies do not claim depreciation for assets purchased in the second half of the year. For Cooper's December 31, 20X3, separate-entry financial statements, what net book value should be shown for the machine?

(Multiple Choice)

4.9/5 (43)

Pal Co. owns 70% of the outstanding common shares of Sadd Ltd. Sadd sold an asset to Pal at a loss. There is no evidence of impairment in the value of the asset sold to Pal. Which of the following statements about the loss is true?

(Multiple Choice)

4.8/5 (36)

Belzer Co. owns 70% of Sabo Ltd. At the beginning of 20X7, Sabo sold a piece of equipment to Belzer for a gain of $35,000. At that time, the equipment had an estimated useful life of seven years.

-Which of the following statements is true about calculating the NCI for the consolidated SFP?

(Multiple Choice)

4.9/5 (43)

Arnez Ltd. acquired 70% of the outstanding common shares of Bedard Ltd. At the acquisition date, Bedard's net identifiable assets had a carrying value of $825,000 and a fair market value of $1,000,000. Arnez paid $910,000 for the acquisition. Under the entity method, what amount should be reported for the non-controlling interest on the consolidated statement of financial position?

(Multiple Choice)

4.8/5 (40)

Tooker Co. acquired 80% of the outstanding common shares of Vu Ltd. There were no fair value increments or goodwill that arose with the purchase. During 20X1, Tooker sold $7,000 of inventory to Vu for a gross profit of 40%. At the end of 20X1, $3,000 of the inventory is still in Vu's inventory. On their separate-entity income statements for 20X1, Tooker and Vu reported the following: Tooker Vu Sales \ 38,000 \ 15,000 Cost of sales 26,400 8,500 Operating expenses Net income \ 6,400 \ 2,900 Vu sold all the goods from Tooker that were in its opening inventory. There were no sales between Tooker and Vu in 20X2. What is the non-controlling interest's share of consolidated net income at the end of 20X2?

(Multiple Choice)

4.8/5 (45)

Mallard Ltd. acquired 75% of the outstanding common shares of Teal Ltd. at December 31, 20X1, for $900,000. Mallard has recorded its investment using the cost method.

- At the end of 20X7, Mallard still had $40,000 of goods purchased from Teal in its inventory and Teal had $50,000 of goods purchased from Mallard in its inventory. Both companies had gross margins of 50% in their sales of goods to each other and both companies sold these goods in 20X8. What journal entry should be made for Mallard's 20X8 consolidated financial statements with respect to the goods purchased from Teal that were still in Mallard's opening inventory?

(Multiple Choice)

4.8/5 (38)

Singh Ltd. is a wholly owned subsidiary of Ross Co. At the beginning of 20X4, Ross acquired a machine for $350,000 and sold it to Singh for $437,500. The machine will be depreciated over five years using the straight-line method with no residual value.

-In preparing the consolidated financial statements for the second year after the sale to Singh, Ross made the following journal entry: DR Accumulated depreciation-machine 17,500 CR Depreciation expense-machine 17,500 What other adjustment must be made in preparing the consolidated financial statements?

(Multiple Choice)

4.8/5 (39)

On January 1, 20X5, PX's shareholders' equity was as follows:

Common shares \ 40,000 Retained earnings GL held 90% of the 8,000 outstanding shares of PX on January 1, 20X5, and its investment in PX account had a balance of $252,000 on that date. GL accounts for its investment in its subsidiary by the equity method using the entity approach. At the time of acquisition of PX, the only fair value increment arising was due to the patent, which had a remaining life of five years on January 1, 20X5.

The following transactions took place subsequent to January 1, 20X5:

• During 20X5, PX reported a net income of $80,000 (earned equally throughout the year).

• PX declared dividends of $10,000 on September 1.

• During 20X6, PX reported a net income of $76,000 and paid dividends of $16,000 on December 1.

• During 20X6, PX sold equipment to GL for $140,000. At the time, the net book value of the equipment to PX was $100,000. There are four years remaining on the useful life of the equipment. Both companies record a full year of depreciation expense in the year of the purchase and no depreciation in the year of a sale.

Required:

Assuming that no value is assigned to patents on the separate-entity financial statements for GL and PX, calculate patents on the consolidated balance sheet at December 31, 20X6.

Calculate the allocation of the consolidated net income to the non-controlling interest for each of 20X5 and 20X6.

(Essay)

4.8/5 (44)

When investments in associate or joint ventures are reported using the equity method, IFRS requires the application of ________.

(Multiple Choice)

4.8/5 (40)

Tooker Co. acquired 80% of the outstanding common shares of Vu Ltd. There were no fair value increments or goodwill that arose with the purchase. During 20X1, Tooker sold $7,000 of inventory to Vu for a gross profit of 40%. At the end of 20X1, $3,000 of the inventory is still in Vu's inventory. On their separate-entity income statements for 20X1, Tooker and Vu reported net income of $4,200 and $3,100, respectively. What is the non-controlling interest's share of consolidated net income at the end of 20X1?

(Multiple Choice)

4.7/5 (36)

Chandler Ltd. owns 65% of Stork Co. and accounts for its investment using the cost method. During 20X3, Chandler sold its only land holding to Stork for a $25,000 profit. At the end of 20X4, Stork showed the land on its single-entity financial statement at a value of $100,000. What balance should Chandler show on its consolidated statement of financial position for the land?

(Multiple Choice)

4.8/5 (33)

Linville Ltd. owns 80% of the outstanding shares of Chance Co. On January 2, 20X1, Chance sold a machine to Linville for $270,000. Chance recorded a $45,000 gain on the sale. At the time of the sale, the machine had a remaining useful life of three years. Both companies use the straight-line method of depreciation. What amount should be shown for depreciation expense on Linville's consolidated statement of comprehensive income at December 31, 20X1?

(Multiple Choice)

5.0/5 (30)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)