Exam 4: Wholly Owned Subsidiaries: Reporting Subsequent Acquisitions

Exam 1: Setting the Stage40 Questions

Exam 2: Intercorporate Equity Investments: an Introduction43 Questions

Exam 3: Business Combinations43 Questions

Exam 3: Appendix A: AIncome Tax Allocation6 Questions

Exam 4: Wholly Owned Subsidiaries: Reporting Subsequent Acquisitions40 Questions

Exam 4: Appendix A: Wholly Owned Subsidiaries: Reporting Subsequent Acquisitions4 Questions

Exam 4: Appendix B: Wholly Owned Subsidiaries: Reporting Subsequent Acquisitions6 Questions

Exam 5: Consolidation of Non-Wholly Owned Subsidiaries41 Questions

Exam 5: Appendix A: Step Purchases6 Questions

Exam 5: Appendix B: Decreases in Ownership Interest4 Questions

Exam 6: Subsequent-Year Consolidations: General Approach40 Questions

Exam 6: Appendix A: Preferred and Restricted Shares of Investee Corporation5 Questions

Exam 6: Appendix B: Intercompany Bond Holdings6 Questions

Exam 7: Segment and Interim Reporting41 Questions

Exam 8: Foreign Currency Transactions and Hedges49 Questions

Exam 9: Reporting Foreign Operations44 Questions

Exam 10: Financial Reporting for Not-For-Profit Organizations46 Questions

Exam 10: Appendix A: Fund Accounting5 Questions

Exam 11: Public Sector Financial Reporting44 Questions

Select questions type

On December 31, 20X5, Space Co. purchased 100% of the outstanding common shares of Shuttle Ltd. for $1,200,000 in shares and $200,000 in cash. The statements of financial position of Space and Shuttle immediately before the acquisition and issuance of the notes payable were as follows (in 000s):

Book Fair Book Fair Value Value Value Value Cash \ 360 \ 360 \ 200 \ 200 Accounts receivable 520 500 380 340 Inventory 800 880 400 Property, plant, and equipment 2,000 1,520 Accounts payable \ 380 \ 380 \ 260 \ 260 Long-term liabilities 1,200 1,200 1000 1000 Common shares 500 600 Retained earnings The difference in the carrying value and the fair value of the capital assets for Shuttle relates to its office building. This building was originally purchased by Shuttle in January 20X1 and is being depreciated over 30 years.

During 20X6, the year following the acquisition, the following occurred:

1. Shuttle borrowed $350,000 from Space on June 1, 20X6, and was charged interest at 10% per annum, which it paid on a monthly basis. There were no repayments of principal made during the remaining of the year.

2. Throughout the year, Shuttle purchased merchandise of $800,000 from Space. Space's gross margin is 30% of selling price. At December 31, 20X6, Shuttle still owed Space $250,000 on this merchandise; 75% of this merchandise was resold by Shuttle prior to December 31, 20X6.

3. Shuttle paid dividends of $250,000 at the end of 20X6 and Space paid dividends of $500,000.

During 20X7, the following occurred:

1. Shuttle paid $150,000 on the loan payable to Space on May 30, 20X7.

2. Throughout the year, Shuttle purchased merchandise of $1,000,000 from Space. Space's gross margin is 30% of selling price. At December 31, 20X6, Shuttle still owed Space $150,000 on this merchandise; 85% of this merchandise was resold by Shuttle prior to December 31, 20X7.

3. Shuttle paid dividends of $250,000 at the end of 20X7 and Space paid dividends of $500,000.  Required:

Prepare the consolidated statement of comprehensive income for the year ended December 31, 20X7, for Space.s) } \end{array} \\ \begin{array} { | l | r | r | } \hline & \text { Space \$} & \text { Shuttle \$} \\ \hline \text { Retained earnings, December 31, 20X6 } & 1,775 & 695 \\ \hline \text { Net income } & 990 & 490 \\ \hline \text { Dividends declared } & ( 500 ) & ( 250 ) \\ \hline \text { Retained earnings, December 31, 20X7 } & \underline { 2,265 } & 935 \\ \hline \end{array} \end{array} Required: Prepare the consolidated statement of comprehensive income for the year ended December 31, 20X7, for Space. " class="answers-bank-image d-inline" loading="lazy" > 11ea84f2_a85b_0257_9a63_4171128d30b3_TB3071_00 Required:

Prepare the consolidated statement of comprehensive income for the year ended December 31, 20X7, for Space.s) } \end{array} \\ \begin{array} { | l | r | r | } \hline & \text { Space \$} & \text { Shuttle \$} \\ \hline \text { Retained earnings, December 31, 20X6 } & 1,775 & 695 \\ \hline \text { Net income } & 990 & 490 \\ \hline \text { Dividends declared } & ( 500 ) & ( 250 ) \\ \hline \text { Retained earnings, December 31, 20X7 } & \underline { 2,265 } & 935 \\ \hline \end{array} \end{array} Required: Prepare the consolidated statement of comprehensive income for the year ended December 31, 20X7, for Space. " class="answers-bank-image d-inline" loading="lazy" > Required:

Prepare the consolidated statement of comprehensive income for the year ended December 31, 20X7, for Space.s) } \end{array} \\ \begin{array} { | l | r | r | } \hline & \text { Space \$} & \text { Shuttle \$} \\ \hline \text { Retained earnings, December 31, 20X6 } & 1,775 & 695 \\ \hline \text { Net income } & 990 & 490 \\ \hline \text { Dividends declared } & ( 500 ) & ( 250 ) \\ \hline \text { Retained earnings, December 31, 20X7 } & \underline { 2,265 } & 935 \\ \hline \end{array} \end{array} Required: Prepare the consolidated statement of comprehensive income for the year ended December 31, 20X7, for Space. " class="answers-bank-image d-inline" loading="lazy" > 11ea84f2_a85b_0257_9a63_4171128d30b3_TB3071_00 Required:

Prepare the consolidated statement of comprehensive income for the year ended December 31, 20X7, for Space.

Required:

Prepare the consolidated statement of comprehensive income for the year ended December 31, 20X7, for Space.s) } \end{array} \\ \begin{array} { | l | r | r | } \hline & \text { Space \$} & \text { Shuttle \$} \\ \hline \text { Retained earnings, December 31, 20X6 } & 1,775 & 695 \\ \hline \text { Net income } & 990 & 490 \\ \hline \text { Dividends declared } & ( 500 ) & ( 250 ) \\ \hline \text { Retained earnings, December 31, 20X7 } & \underline { 2,265 } & 935 \\ \hline \end{array} \end{array} Required: Prepare the consolidated statement of comprehensive income for the year ended December 31, 20X7, for Space. " class="answers-bank-image d-inline" loading="lazy" > 11ea84f2_a85b_0257_9a63_4171128d30b3_TB3071_00 Required:

Prepare the consolidated statement of comprehensive income for the year ended December 31, 20X7, for Space.s) } \end{array} \\ \begin{array} { | l | r | r | } \hline & \text { Space \$} & \text { Shuttle \$} \\ \hline \text { Retained earnings, December 31, 20X6 } & 1,775 & 695 \\ \hline \text { Net income } & 990 & 490 \\ \hline \text { Dividends declared } & ( 500 ) & ( 250 ) \\ \hline \text { Retained earnings, December 31, 20X7 } & \underline { 2,265 } & 935 \\ \hline \end{array} \end{array} Required: Prepare the consolidated statement of comprehensive income for the year ended December 31, 20X7, for Space. " class="answers-bank-image d-inline" loading="lazy" > Required:

Prepare the consolidated statement of comprehensive income for the year ended December 31, 20X7, for Space.s) } \end{array} \\ \begin{array} { | l | r | r | } \hline & \text { Space \$} & \text { Shuttle \$} \\ \hline \text { Retained earnings, December 31, 20X6 } & 1,775 & 695 \\ \hline \text { Net income } & 990 & 490 \\ \hline \text { Dividends declared } & ( 500 ) & ( 250 ) \\ \hline \text { Retained earnings, December 31, 20X7 } & \underline { 2,265 } & 935 \\ \hline \end{array} \end{array} Required: Prepare the consolidated statement of comprehensive income for the year ended December 31, 20X7, for Space. " class="answers-bank-image d-inline" loading="lazy" > 11ea84f2_a85b_0257_9a63_4171128d30b3_TB3071_00 Required:

Prepare the consolidated statement of comprehensive income for the year ended December 31, 20X7, for Space.

Free

(Essay)

4.9/5  (38)

(38)

Correct Answer: Verified

Verified

Under the direct method, what values should be entered for the assets, liabilities, and shareholders' equity to start the consolidation process?

Free

(Multiple Choice)

4.7/5 (45)

Correct Answer:Verified

A

On January 1, 20X3, Dwayne Ltd. formed Carlos Co., a 100% owned subsidiary. During 20X6, Dwayne sold Carlos $100,000 in goods. The unrealized profit in Carlos's inventories was $20,000 at December 31, 20X5, and $25,000 at December 31, 20X6.

-Ignoring income taxes, what accounts should Dwayne debit and credit by $20,000 in preparing its consolidated financial statements for the year ended December 31, 20X6, to reflect the unrealized profit in Carlos's beginning inventory? Debit Credit

A) Cost of sales Inventory

B) Inventcry Cost of Sales

C) Retained earnings Cost of sales

D) Cost of sales Tetained earnings

Free

(Short Answer)

4.7/5 (31)

Correct Answer:Verified

C

Mitzi's Muffins Ltd. purchased a commercial baking system for $150,000 at the beginning of 20X1. The estimated economic life of the system is 10 years and Mitzi's uses straight-line amortization. At the beginning of 20X3, Delicious Bakeries Ltd. acquired Mitzi's in a business combination.

-At the time of acquisition, Mitzi's baking system had a fair value of $140,000. At the end of 20X3, how much amortization expense should Mitzi report?

(Multiple Choice)

4.8/5 (29)

Which of the following statements about goodwill impairment testing under IFRS and ASPE is true?

(Multiple Choice)

4.9/5 (38)

On December 31, 20X5, Space Co. purchased 100% of the outstanding common shares of Shuttle Ltd. for $1,200,000 in shares and $200,000 in cash. The statements of financial position of Space and Shuttle immediately before the acquisition and issuance of the notes payable were as follows (in 000s):

Book Fair Book Fair Value Value Value Value Cash \ 360 \ 360 \ 200 \ 200 Accounts receivable 520 500 380 340 Inventory 800 880 400 Property, plant, and equipment 2,000 1,520 \ 3,500 \ 2,400 Accounts payable \ 380 \ 380 \ 260 \ 260 Long-term liabilities 1,200 1,200 1000 1000 Common shares 500 600 Retained earnings The difference in the carrying value and the fair value of the property, plant, and equipment for Shuttle relates to its office building. This building was originally purchased by Shuttle in January 20X1 and is being depreciated over 30 years.

During 20X6, the year following the acquisition, the following occurred:

1. Shuttle borrowed $350,000 from Space on June 1, 20X6, and was charged interest at 10% per annum, which it paid on a monthly basis. There were no repayments of principal made during the remaining of the year.

2. Throughout the year, Shuttle purchased merchandise of $800,000 from Space. Space's gross margin is 30% of selling price. At December 31, 20X6, Shuttle still owed Space $250,000 on this merchandise; 75% of this merchandise was resold by Shuttle prior to December 31, 20X6.

3. Shuttle paid dividends of $250,000 at the end of 20X6 and Space paid dividends of $500,000.

During 20X7, the following occurred:

1. Shuttle paid $150,000 on the loan payable to Space on May 30, 20X7.

2. Throughout the year, Shuttle purchased merchandise of $1,000,000 from Space. Space's gross margin is 30% of selling price. At December 31, 20X6, Shuttle still owed Space $150,000 on this merchandise; 85% of this merchandise was resold by Shuttle prior to December 31, 20X7.

3. Shuttle paid dividends of $250,000 at the end of 20X7 and Space paid dividends of $500,000.

Required:

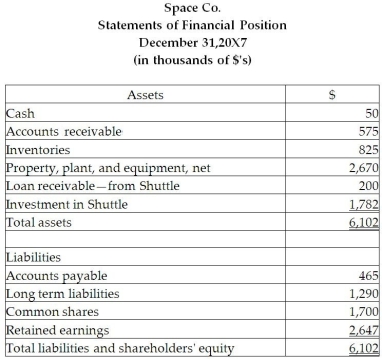

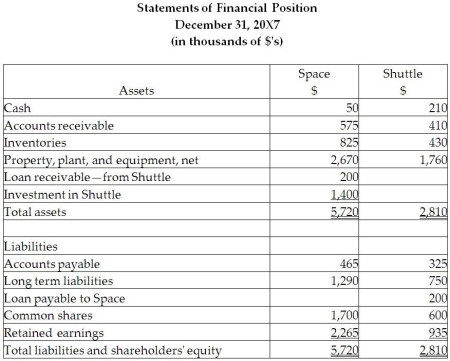

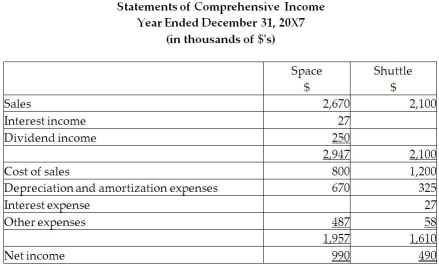

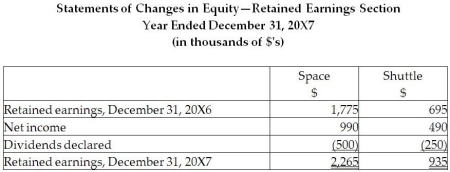

Space has decided to record its investment in Shuttle using the equity method. Determine the balance in the Investment in Shuttle account at December 31, 20X7, using the equity method.

Prepare the statement of financial position and the statement of comprehensive income for the year ended December 31, 20X7, for Space, assuming it accounts for its investment in Shuttle using the equity method.

Required:

Space has decided to record its investment in Shuttle using the equity method. Determine the balance in the Investment in Shuttle account at December 31, 20X7, using the equity method.

Prepare the statement of financial position and the statement of comprehensive income for the year ended December 31, 20X7, for Space, assuming it accounts for its investment in Shuttle using the equity method.

(Essay)

4.7/5 (32)

On December 31, 20X2, Pipe Ltd. purchased 100% of the outstanding common shares of Fitter Ltd. for $10.5 million in cash. On that date, the shareholders' equity of Fitter totalled $8 million and consisted of $1 million in no par common shares and $7 million in retained earnings. Both companies use the straight-line method to calculate depreciation and amortization. Goodwill, if any arises as a result of this business combination, is written down if there is an impairment in its value. Pipe follows IFRS.

For the year ending December 31, 20X6, the income statements for Pipe and Fitter were as follows:

Pipe Fitter Sales and other revenue Cost of goods sold 16,000,000 5,000,000 Depreciation expense 2,500,000 2,000,000 Other expenses Total expenses Net income At December 31, 20X6, the condensed balance sheets for the two companies were as follows:

Pipe Fitter Total assets Liabilities \ 5,000,000 \ 1,200,000 No par common stock 12,100,000 1,000,000 Retained earnings Total liabilities andshareholders' equity OTHER INFORMATION:

1. On December 31, 20X2, Fitter had a building with a fair value that was $500,000 greater than its carrying value. The building had an estimated remaining useful life of 20 years.

2. On December 31, 20X2, Fitter had trademark that was not reported on its balance sheet but had a fair value that was $200,000. The trademark is amortized over 10 years.

3. During 20X6, Fitter sold merchandise to Pipe for $100,000, a price that included a gross profit of $40,000. During 20X6, 20% of this merchandise was resold by Pipe and the other 80% remains in its December 31, 20X6, inventories. On December 31, 20X5, the inventories of Pipe contained merchandise purchased from Fitter on which Fitter had recognized a gross profit in the amount of $50,000.

4. During 20X6, it was determined that the goodwill arising at the date of acquisition was impaired and that an impairment loss of $70,000 should be recorded. No impairment had been charged in earlier years.

5. During 20X6, Pipe declared and paid dividends of $300,000, while Fitter declared and paid dividends of $100,000.

6. Pipe accounts for its investment in Fitter using the cost method.

The retained earnings of Pipe as at December 31, 20X5, equalled $12,000,000. On that date, Fitter had retained earnings of $9,800,000. Fitter has not issued any common stock since its acquisition by Pipe.

Required:

Prepare, in good form, a consolidated statement of comprehensive income for the year ended December 31, 20X6.

(Essay)

4.9/5 (40)

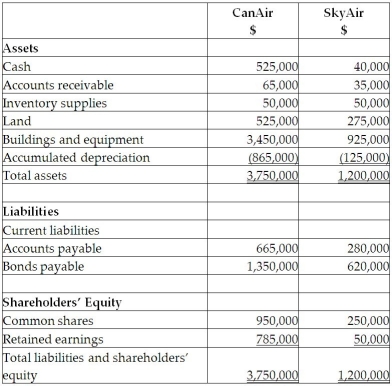

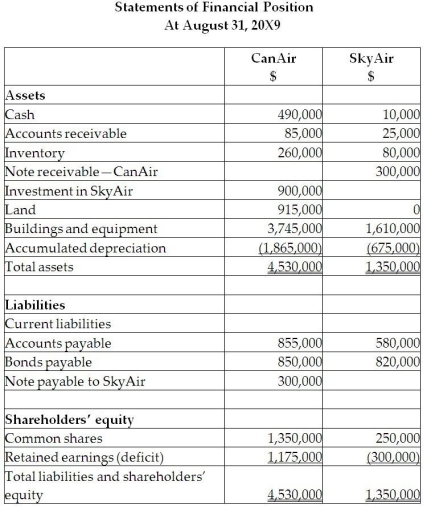

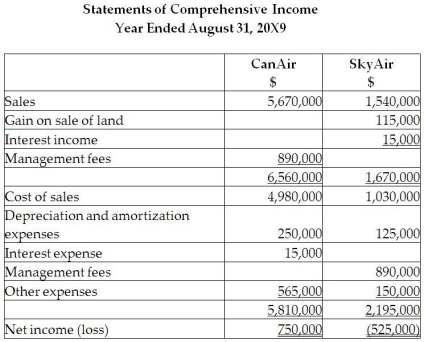

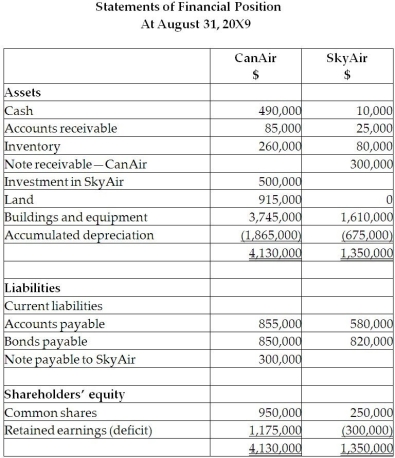

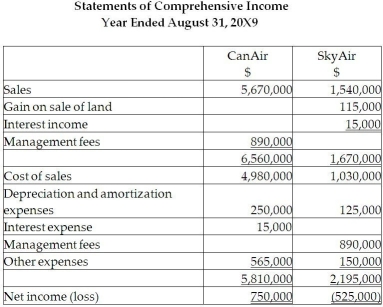

On September 1, 20X5, CanAir Limited decided to buy 100% of the shares outstanding of SkyAir Inc. for $900,000. CanAir will pay for this acquisition by using cash of $500,000 and issuing share capital for the remaining amount. The balances showing on the statement of financial position for the two companies at August 31, 20X5, are as follows:  After a review of the financial assets and liabilities, CanAir determines that some of the assets of SkyAir have fair values different from their carrying values. These items are listed below:

• Land has a fair value of 225,000.

• The building has a fair value of $1,090,000. (The company does not own any equipment.)The remaining useful life of the building is 20 years.

• Internet domain name has a fair value is $55,000. The domain name is estimated to have a useful life of five years.

• Customer lists have a fair value is $35,000. It is estimated that the customer lists will have a useful life of seven years.

During the 20X9 fiscal year, the following events occurred:

1. On March 1, 20X9, SkyAir sold land to CanAir for $390,000, which had a carrying value of $275,000. CanAir paid for this with $90,000 cash and a note payable for the difference. This note pays interest at 10%, which is paid monthly.

2. CanAir provided management expertise to SkyAir and charged management fees of $890,000.

3. CanAir sold supplies (included in CanAir sales)to SkyAir for $200,000. CanAir charged SkyAir an amount that was 25% above cost. SkyAir still has supplies on hand of $70,000.

4. In 20X8, SkyAir provided seat space on flights to CanAir for a value of $500,000. This amount was included in sales for SkyAir. Profit margin on these sales is 40%. At the end of August, 20X8, CanAir still had an amount of $200,000 in these prepaid seats that had not yet been used. (CanAir includes this in inventory.)

After a review of the financial assets and liabilities, CanAir determines that some of the assets of SkyAir have fair values different from their carrying values. These items are listed below:

• Land has a fair value of 225,000.

• The building has a fair value of $1,090,000. (The company does not own any equipment.)The remaining useful life of the building is 20 years.

• Internet domain name has a fair value is $55,000. The domain name is estimated to have a useful life of five years.

• Customer lists have a fair value is $35,000. It is estimated that the customer lists will have a useful life of seven years.

During the 20X9 fiscal year, the following events occurred:

1. On March 1, 20X9, SkyAir sold land to CanAir for $390,000, which had a carrying value of $275,000. CanAir paid for this with $90,000 cash and a note payable for the difference. This note pays interest at 10%, which is paid monthly.

2. CanAir provided management expertise to SkyAir and charged management fees of $890,000.

3. CanAir sold supplies (included in CanAir sales)to SkyAir for $200,000. CanAir charged SkyAir an amount that was 25% above cost. SkyAir still has supplies on hand of $70,000.

4. In 20X8, SkyAir provided seat space on flights to CanAir for a value of $500,000. This amount was included in sales for SkyAir. Profit margin on these sales is 40%. At the end of August, 20X8, CanAir still had an amount of $200,000 in these prepaid seats that had not yet been used. (CanAir includes this in inventory.)

Required:

Prepare the consolidated statement of comprehensive income for the year ended August 31, 20X9.

Required:

Prepare the consolidated statement of comprehensive income for the year ended August 31, 20X9.

(Essay)

4.9/5 (38)

Which of the following consolidation adjustments will be required for a subsidiary that was acquired as a going concern, but will not be applicable for a parent-founded subsidiary?

(Multiple Choice)

4.7/5 (39)

On January 1, 20X3, Dwayne Ltd. formed Carlos Co., a 100% owned subsidiary. During 20X6, Dwayne sold Carlos $100,000 in goods. The unrealized profit in Carlos's inventories was $20,000 at December 31, 20X5, and $25,000 at December 31, 20X6.

-Ignoring income taxes, what accounts should Dwayne debit and credit by $25,000 in preparing its consolidated financial statements for the year ended December 31, 20X6, to reflect the unrealized profit in Carlos's ending inventory? Debit Credit

A) Cost of sales Inventory

B) Inventcry Cost of Sales

C) Retained earnings Cost of sales

D) Cost of sales Tetained earnings

(Short Answer)

4.8/5 (33)

Coral Ltd. owns 100% of Ambrose Ltd. Coral uses the cost method to record this subsidiary. Coral received $150,000 in dividends from Ambrose. What journal entry should Coral make on its consolidation worksheet with respect to the dividends?

(Multiple Choice)

4.7/5 (37)

DC Company purchased 80% of the outstanding common shares of FA Company on December 31, 20X3, for $170,000. At that date, FA had $100,000 of outstanding common stock and retained earnings of $30,000. It was agreed that the net assets were fairly valued except that the fair value of the capital assets exceeded their net book value by $20,000 and the carrying value of the inventory exceeded its fair value by $10,000. The capital assets had a remaining useful life of eight years as of the acquisition date and have no salvage value. Inventory turns over four times a year. It is now 20X6 and DC has been very pleased with how profitable its investment in FA has been. On DC's consolidated financial statements at December 31, 20X6, what balance should be reported for goodwill assuming no impairment has occurred?

(Multiple Choice)

4.8/5 (42)

Franklin Ltd., a subsidiary of Frayer Ltd., sold $500,000 of goods to its parent company in 20X1. At the end of 20X1, some of the goods were not sold and there was $90,000 of unrealized profit associated with these goods. The goods were sold in 20X2. At the end of 20X2, which of the following consolidating entries should be made with respect to the unrealized profits?

(Multiple Choice)

4.8/5 (36)

A parent company records an investment in its subsidiary using the equity method. Which of the following statements about consolidated net income is true?

(Multiple Choice)

4.9/5 (33)

In consolidating parent-founded subsidiaries, what account is used to offset the parent company's "Investment in Subsidiary" account?

(Multiple Choice)

4.7/5 (42)

Paranich Co. acquired Crowley Co. in a business combination at December 31, 20X4. Crowley has a capital asset that it has been amortizing at a rate of $10,000 per year. At the time of the acquisition, the asset had a book value of $70,000 and a fair value of $77,000. The asset has a remaining life of seven years. With respect to this asset, how much amortization expense should Paranich report on its December 31, 20X5, consolidated financial statements?

(Multiple Choice)

4.9/5 (42)

Piri Ltd. acquired 100% of the commons shares of Golden Co. This business combination resulted in $100,000 of goodwill. Piri allocated the goodwill to three cash-generating units. At its year-end, Piri conducts a goodwill impairment test. Which of the following statements about the impairment test is true?

(Multiple Choice)

4.8/5 (45)

DC Company purchased 100% of the outstanding common shares of FA Company on December 31, 20X3, for $170,000. At that date, FA had $100,000 of outstanding common shares and retained earnings of $30,000. It was agreed that the net assets were fairly valued except that the fair value of the capital assets exceeded their net book value by $20,000 and the carrying value of the inventory exceeded its fair value by $10,000. The capital assets had a remaining useful life of eight years as of the acquisition date and have no residual value. Inventory turns over four times a year.

- What adjustment should be made to the consolidated financial statements for the year ended December 31, 20X6, for the fair value increment related to the capital assets?

(Multiple Choice)

4.9/5 (39)

Amber Ltd. acquired Luna Ltd. in a business combination. One of the main reasons for the acquisition is that Amber wanted access to Luna's extensive customer list. The list is not recorded on Luna's books and has an estimated value of $100,000 and an estimated life of seven years. On Amber's consolidated statement of financial position, what value should be shown for Luna's customer list?

(Multiple Choice)

4.8/5 (39)

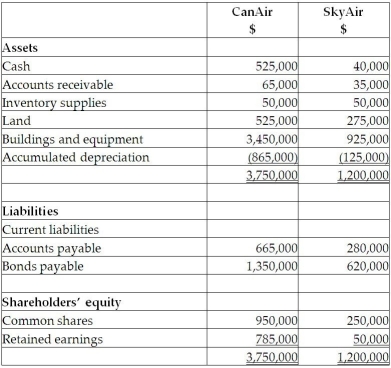

On September 1, 20X5, CanAir Limited decided to buy 100% of the shares outstanding of SkyAir Inc. for $500,000. Can Air will pay for this acquisition by using cash of $500,000. The balances showing on the statement of financial position for the two companies at August 31, 20X5, are as follows:  After a review of the financial assets and liabilities, CanAir determines that some of the assets of SkyAir have fair values different from their carrying values. These items are listed below:

• The building has a fair value of $1,090,000. The remaining useful life of the building is 20 years.

• Internet domain name has a fair value is $55,000. The domain name is estimated to have a useful life of five years.

• Brand name has a fair value is $65,000 and an indefinite life.

During the 20X9 fiscal year, the following events occurred:

1. On March 1, 20X9, SkyAir sold land to CanAir for $390,000, which had a carrying value of $275,000. CanAir paid for this with $90,000 cash and a note payable for the difference. This note pays interest at 10%, which is paid monthly.

2. CanAir provided management expertise to SkyAir and charged management fees of $890,000.

3. CanAir sold supplies (included in CanAir sales)to SkyAir for $200,000. CanAir charged SkyAir an amount that was 25% above cost. SkyAir still has supplies on hand of $20,000.

4. In 20X8, SkyAir provided seat space on flights to Can Air for a value of $300,000. This amount was included in sales for SkyAir. Profit margin on these sales is 30%. At the end of August, 20X8, CanAir still had an amount of $150,000 in these prepaid seats that had not yet been used. (CanAir includes this in inventory.)

After a review of the financial assets and liabilities, CanAir determines that some of the assets of SkyAir have fair values different from their carrying values. These items are listed below:

• The building has a fair value of $1,090,000. The remaining useful life of the building is 20 years.

• Internet domain name has a fair value is $55,000. The domain name is estimated to have a useful life of five years.

• Brand name has a fair value is $65,000 and an indefinite life.

During the 20X9 fiscal year, the following events occurred:

1. On March 1, 20X9, SkyAir sold land to CanAir for $390,000, which had a carrying value of $275,000. CanAir paid for this with $90,000 cash and a note payable for the difference. This note pays interest at 10%, which is paid monthly.

2. CanAir provided management expertise to SkyAir and charged management fees of $890,000.

3. CanAir sold supplies (included in CanAir sales)to SkyAir for $200,000. CanAir charged SkyAir an amount that was 25% above cost. SkyAir still has supplies on hand of $20,000.

4. In 20X8, SkyAir provided seat space on flights to Can Air for a value of $300,000. This amount was included in sales for SkyAir. Profit margin on these sales is 30%. At the end of August, 20X8, CanAir still had an amount of $150,000 in these prepaid seats that had not yet been used. (CanAir includes this in inventory.)

Required:

CanAir would like to report this investment in SkyAir using the equity method.

Determine the income from this equity investment for the year.

Determine the balance in the Investment in SkyAir account if the company used the equity method.

Required:

CanAir would like to report this investment in SkyAir using the equity method.

Determine the income from this equity investment for the year.

Determine the balance in the Investment in SkyAir account if the company used the equity method.

(Essay)

4.9/5 (30)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)