Exam 8: Firms in Perfectly Competitive Markets

Exam 1: Economics: Foundations and Models160 Questions

Exam 2: Choices and Trade-Offs in the Market192 Questions

Exam 3: Where Prices Come From: the Interaction of Demand and Supply202 Questions

Exam 4: Elasticity: the Responsiveness of Demand and Supply226 Questions

Exam 5: Economic Efficiency, Government Price Setting and Taxes187 Questions

Exam 6: Consumer Choice and Behavioural Economics254 Questions

Exam 7: Technology, Production and Costs300 Questions

Exam 8: Firms in Perfectly Competitive Markets270 Questions

Exam 9: Monopoly Markets281 Questions

Exam 10: Monopolistic Competition253 Questions

Exam 11: Oligopoly: Firms in Less Competitive Markets186 Questions

Exam 12: The Markets for Labour and Other Factors of Production253 Questions

Exam 13: International Trade131 Questions

Exam 14: Government Intervention in the Market122 Questions

Exam 15: Externalities, Environmental Policy and Public Goods212 Questions

Exam 16: The Distribution of Income and Social Policy121 Questions

Select questions type

If,as a perfectly competitive industry expands,it can supply larger quantities only at a higher long-run equilibrium price,it is

(Multiple Choice)

4.9/5  (42)

(42)

A perfectly competitive firm in a constant-cost industry produces 1000 units of a good at a total cost of $50 000.The prevailing market price is $48.Assuming that this firm continues to produce in the long run,what happens to output level in the long run?

(Multiple Choice)

4.9/5 (28)

Under what conditions should a competitive firm shut down in the short run?

(Essay)

4.9/5 (27)

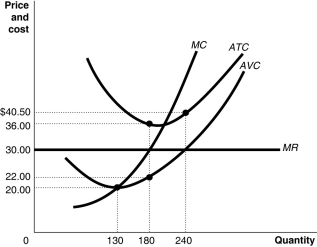

Figure 8-4  Figure 8-4 shows the cost and demand curves for a profit-maximising firm in a perfectly competitive market.

-Refer to Figure 8-4.If the market price is $30,should the firm represented in the diagram continue to stay in business?

Figure 8-4 shows the cost and demand curves for a profit-maximising firm in a perfectly competitive market.

-Refer to Figure 8-4.If the market price is $30,should the firm represented in the diagram continue to stay in business?

(Multiple Choice)

4.8/5 (32)

Figure 8-4 Figure 8-4 shows the cost and demand curves for a profit-maximising firm in a perfectly competitive market.

-Refer to Figure 8-4.Assuming the firm is profit maximising,what is the amount of its total fixed cost?

(Multiple Choice)

4.7/5 (38)

The market demand curve for a perfectly competitive industry is the horizontal summation of each individual firm's demand curve.

(True/False)

4.8/5 (35)

A perfectly competitive firm produces 3000 units of a good at a total cost of $36 000.The price of each good is $10.Calculate the firm's short-run profit or loss.

(Multiple Choice)

4.8/5 (30)

A perfectly competitive firm's marginal revenue curve is downward sloping.

(True/False)

4.9/5 (41)

Which of the following describes a situation in which a good or service is produced at the lowest possible cost?

(Multiple Choice)

4.7/5 (39)

A perfectly competitive firm produces 3000 units of a good at a total cost of $36 000.The fixed cost of production is $20 000.The price of each good is $10.Should the firm continue to produce in the short run?

(Multiple Choice)

4.9/5 (31)

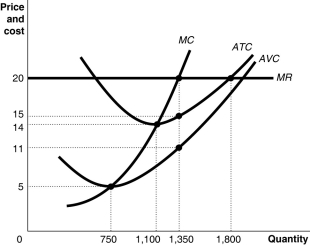

Figure 8-5  Figure 8-5 shows cost and demand curves facing a typical firm in a constant-cost,perfectly competitive industry.

-Refer to Figure 8-5.If the market price is $20,what is the firm's profit-maximising output?

Figure 8-5 shows cost and demand curves facing a typical firm in a constant-cost,perfectly competitive industry.

-Refer to Figure 8-5.If the market price is $20,what is the firm's profit-maximising output?

(Multiple Choice)

4.8/5 (33)

The price a perfectly competitive firm receives for its output

(Multiple Choice)

4.9/5 (30)

Suppose there are economies of scale in the production of a specialised memory chip that is used in manufacturing microwaves.This suggests that the microwave industry is a decreasing-cost industry.

(True/False)

4.7/5 (32)

In the short run,a firm that incurs losses might choose to produce rather than shut down if the amount of its revenue is less than its fixed cost.

(True/False)

4.8/5 (28)

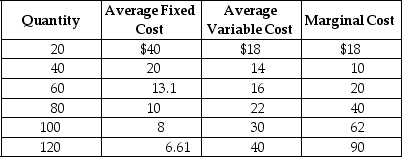

Table 8-4

Table 8-4 shows the short-run cost data of a perfectly competitive firm.Assume that output can only be increased in batches of 20 units.

-Refer to Table 8-4.If the market price is $45,the firm

Table 8-4 shows the short-run cost data of a perfectly competitive firm.Assume that output can only be increased in batches of 20 units.

-Refer to Table 8-4.If the market price is $45,the firm

(Multiple Choice)

4.8/5 (31)

If the market price is $25 in a perfectly competitive market,the marginal revenue from selling the fifth unit is

(Multiple Choice)

4.8/5 (34)

Figure 8-12  -Refer to Figure 8-12.Consider a typical firm in a perfectly competitive industry which is incurring short-run losses.Which of the diagrams in the figure shows the effect on the industry as it transitions to a long-run equilibrium?

-Refer to Figure 8-12.Consider a typical firm in a perfectly competitive industry which is incurring short-run losses.Which of the diagrams in the figure shows the effect on the industry as it transitions to a long-run equilibrium?

(Multiple Choice)

4.8/5 (41)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)