Exam 8: Firms in Perfectly Competitive Markets

Exam 1: Economics: Foundations and Models160 Questions

Exam 2: Choices and Trade-Offs in the Market192 Questions

Exam 3: Where Prices Come From: the Interaction of Demand and Supply202 Questions

Exam 4: Elasticity: the Responsiveness of Demand and Supply226 Questions

Exam 5: Economic Efficiency, Government Price Setting and Taxes187 Questions

Exam 6: Consumer Choice and Behavioural Economics254 Questions

Exam 7: Technology, Production and Costs300 Questions

Exam 8: Firms in Perfectly Competitive Markets270 Questions

Exam 9: Monopoly Markets281 Questions

Exam 10: Monopolistic Competition253 Questions

Exam 11: Oligopoly: Firms in Less Competitive Markets186 Questions

Exam 12: The Markets for Labour and Other Factors of Production253 Questions

Exam 13: International Trade131 Questions

Exam 14: Government Intervention in the Market122 Questions

Exam 15: Externalities, Environmental Policy and Public Goods212 Questions

Exam 16: The Distribution of Income and Social Policy121 Questions

Select questions type

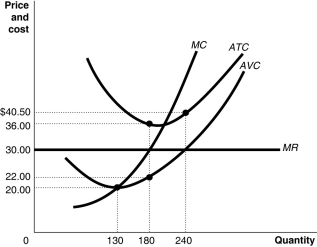

Figure 8-4  Figure 8-4 shows the cost and demand curves for a profit-maximising firm in a perfectly competitive market.

-Refer to Figure 8-4.If the market price is $30,the firm's profit-maximising output level is

Figure 8-4 shows the cost and demand curves for a profit-maximising firm in a perfectly competitive market.

-Refer to Figure 8-4.If the market price is $30,the firm's profit-maximising output level is

(Multiple Choice)

4.8/5  (36)

(36)

What is meant by allocative efficiency? How does a perfectly competitive firm achieve allocative efficiency?

(Essay)

4.8/5 (31)

Ted's Pancake Kitchen suffers a short-run loss.When should Ted decide to shut down rather than continue to produce?

(Multiple Choice)

4.8/5 (31)

If the market price is $40 in a perfectly competitive market,the marginal revenue from selling the fifth unit is

(Multiple Choice)

4.9/5 (44)

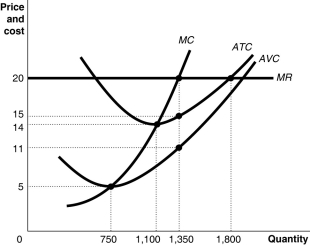

Figure 8-5  Figure 8-5 shows cost and demand curves facing a typical firm in a constant-cost,perfectly competitive industry.

-Refer to Figure 8-5.If the market price is $20,what is the average profit at the profit-maximising quantity?

Figure 8-5 shows cost and demand curves facing a typical firm in a constant-cost,perfectly competitive industry.

-Refer to Figure 8-5.If the market price is $20,what is the average profit at the profit-maximising quantity?

(Multiple Choice)

4.7/5 (39)

If total variable cost exceeds total revenue at all output levels,a perfectly competitive firm

(Multiple Choice)

5.0/5 (42)

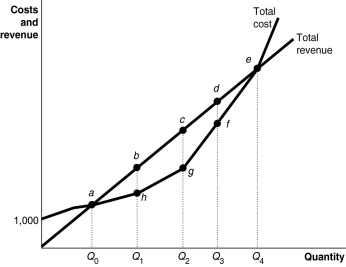

Figure 8-2  -Refer to Figure 8-2.The firm breaks even at an output level of

-Refer to Figure 8-2.The firm breaks even at an output level of

(Multiple Choice)

4.9/5 (41)

The long-run supply curve for a perfectly competitive,constant-cost industry

(Multiple Choice)

5.0/5 (34)

Figure 8-2

-Refer to Figure 8-2.Suppose the firm is currently producing Q2 units.What happens if it expands output to Q3 units?

(Multiple Choice)

4.7/5 (32)

Producing where marginal revenue equals marginal cost is equivalent to producing where

(Multiple Choice)

4.9/5 (34)

After an increase in demand in a constant-cost industry,firms will find themselves with higher average cost curves.

(True/False)

4.9/5 (42)

A perfectly competitive firm will maximise its profit at the rate of output where the vertical distance between its total revenue and total cost is the largest.This is the same rate of output where

(Multiple Choice)

4.9/5 (35)

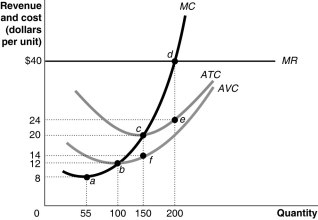

Figure 8-15  -Use the figure above to answer the following questions.

a.How can you determine that the figure represents a graph of a perfectly competitive firm? Be specific;indicate which curve gives you the information and how you use this information to arrive at your conclusion.

b.What is the market price?

c.What is the profit-maximising output?

d.What is total revenue at the profit-maximising output?

e.What is the total cost at the profit-maximising output?

f.What is the profit or loss at the profit-maximising output?

g.What is the firm's total fixed cost?

h.What is the total variable cost?

i.Identify the firm's short-run supply curve.

j.Is the industry in a long-run equilibrium?

k.If it is not in long-run equilibrium,what will happen in this industry to restore long-run equilibrium?

l.In long-run equilibrium,what is the firm's profit maximising quantity?

-Use the figure above to answer the following questions.

a.How can you determine that the figure represents a graph of a perfectly competitive firm? Be specific;indicate which curve gives you the information and how you use this information to arrive at your conclusion.

b.What is the market price?

c.What is the profit-maximising output?

d.What is total revenue at the profit-maximising output?

e.What is the total cost at the profit-maximising output?

f.What is the profit or loss at the profit-maximising output?

g.What is the firm's total fixed cost?

h.What is the total variable cost?

i.Identify the firm's short-run supply curve.

j.Is the industry in a long-run equilibrium?

k.If it is not in long-run equilibrium,what will happen in this industry to restore long-run equilibrium?

l.In long-run equilibrium,what is the firm's profit maximising quantity?

(Essay)

4.9/5 (30)

Letters are used to represent the terms used to answer this question: price (P),quantity of output (Q),total cost (TC)and average total cost (ATC).Which of the following equations is equal to a firm's profit?

(Multiple Choice)

4.8/5 (38)

Which of the following is a characteristic of a firm in a perfectly competitive market?

(Multiple Choice)

4.8/5 (34)

Apple introduced its iPhone 3G in July 2008,and within a month sales had topped 3 million units.By April 2009,more than 25 000 apps for the iPhone 3G were available in the iTunes store,an indication that in a competitive market,

(Multiple Choice)

4.8/5 (37)

The supply curve of a perfectly competitive firm in the short run is

(Multiple Choice)

4.8/5 (30)

What is meant by productive efficiency? How does a perfectly competitive firm achieve productive efficiency?

(Essay)

4.7/5 (42)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)