Exam 8: Firms in Perfectly Competitive Markets

Exam 1: Economics: Foundations and Models160 Questions

Exam 2: Choices and Trade-Offs in the Market192 Questions

Exam 3: Where Prices Come From: the Interaction of Demand and Supply202 Questions

Exam 4: Elasticity: the Responsiveness of Demand and Supply226 Questions

Exam 5: Economic Efficiency, Government Price Setting and Taxes187 Questions

Exam 6: Consumer Choice and Behavioural Economics254 Questions

Exam 7: Technology, Production and Costs300 Questions

Exam 8: Firms in Perfectly Competitive Markets270 Questions

Exam 9: Monopoly Markets281 Questions

Exam 10: Monopolistic Competition253 Questions

Exam 11: Oligopoly: Firms in Less Competitive Markets186 Questions

Exam 12: The Markets for Labour and Other Factors of Production253 Questions

Exam 13: International Trade131 Questions

Exam 14: Government Intervention in the Market122 Questions

Exam 15: Externalities, Environmental Policy and Public Goods212 Questions

Exam 16: The Distribution of Income and Social Policy121 Questions

Select questions type

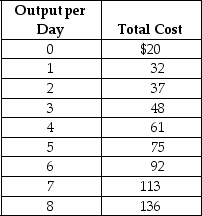

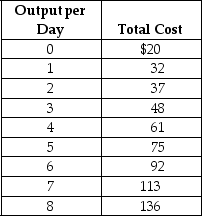

Suppose Veronica sells teapots in the perfectly competitive teapot market.Her output per day and her costs are as follows:

Suppose the current equilibrium price in the teapot market is $15.To maximise profit,how many teapots will Veronica produce,what price will she charge,and how much profit (or loss)will she make? Draw a graph to illustrate your answer.Your graph should include Veronica's demand,ATC,AVC,MC,and MR curves,the price she is charging,the quantity she is producing,and the area representing her profit (or loss).

Suppose the current equilibrium price in the teapot market is $15.To maximise profit,how many teapots will Veronica produce,what price will she charge,and how much profit (or loss)will she make? Draw a graph to illustrate your answer.Your graph should include Veronica's demand,ATC,AVC,MC,and MR curves,the price she is charging,the quantity she is producing,and the area representing her profit (or loss).

(Essay)

4.7/5  (29)

(29)

A teenaged babysitter is similar to a firm in a perfectly competitive industry in that,for both,

(Multiple Choice)

4.9/5 (46)

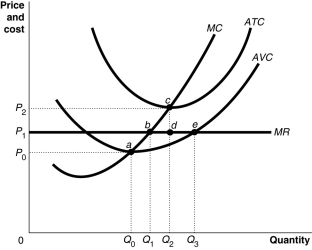

Figure 8-5  Figure 8-5 shows cost and demand curves facing a typical firm in a constant-cost,perfectly competitive industry.

-Refer to Figure 8-5.If the market price is $20,what is the amount of the firm's profit?

Figure 8-5 shows cost and demand curves facing a typical firm in a constant-cost,perfectly competitive industry.

-Refer to Figure 8-5.If the market price is $20,what is the amount of the firm's profit?

(Multiple Choice)

4.7/5 (35)

In the short run,a firm that is operating at a loss has two options.These options are

(Multiple Choice)

4.8/5 (40)

Which of the following describes a situation in which every good or service is produced up to the point where the last unit provides a marginal benefit to consumers equal to the marginal cost of producing it?

(Multiple Choice)

4.9/5 (34)

Table 8-1

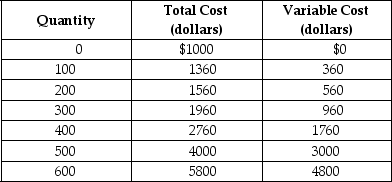

Table 8-1 shows the short-run cost data of a perfectly competitive firm that produces plastic camera cases.Assume that output can only be increased in batches of 100 units.

-Refer to Table 8-1.If the market price of each camera case is $8,what is the firm's total revenue?

Table 8-1 shows the short-run cost data of a perfectly competitive firm that produces plastic camera cases.Assume that output can only be increased in batches of 100 units.

-Refer to Table 8-1.If the market price of each camera case is $8,what is the firm's total revenue?

(Multiple Choice)

5.0/5 (34)

When firms exit a perfectly competitive industry,the market supply curve shifts to the left.

(True/False)

4.8/5 (36)

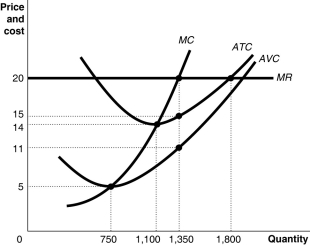

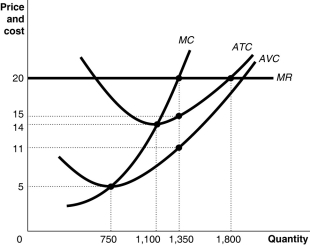

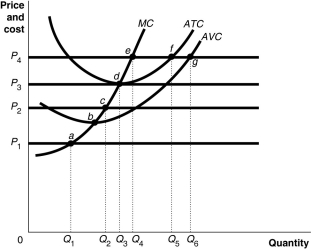

Figure 8-9  -Refer to Figure 8-9.Suppose the prevailing price is $20 and the firm is currently producing 1350 units.In the long-run equilibrium

-Refer to Figure 8-9.Suppose the prevailing price is $20 and the firm is currently producing 1350 units.In the long-run equilibrium

(Multiple Choice)

5.0/5 (40)

Figure 8-11  -Refer to Figure 8-11.Suppose the prevailing price is P1 and the firm is currently producing its loss-minimising quantity.If the firm represented in the diagram continues to stay in business,in the long-run equilibrium

-Refer to Figure 8-11.Suppose the prevailing price is P1 and the firm is currently producing its loss-minimising quantity.If the firm represented in the diagram continues to stay in business,in the long-run equilibrium

(Multiple Choice)

4.7/5 (31)

In the long run,perfectly competitive firms earn zero economic profit.Why do firms enter an industry when they know that in the long run they will not earn any profit?

(Essay)

4.8/5 (42)

Suppose Veronica sells teapots in the perfectly competitive teapot market.Her output per day and her costs are as follows:

Suppose the current equilibrium price in the teapot market is $20.To maximise profit,how many teapots will Veronica produce,what price will she charge,and how much profit (or loss)will she make? Draw a graph to illustrate your answer.Your graph should include Veronica's demand,ATC,AVC,MC,and MR curves,the price she is charging,the quantity she is producing,and the area representing her profit (or loss).

Suppose the current equilibrium price in the teapot market is $20.To maximise profit,how many teapots will Veronica produce,what price will she charge,and how much profit (or loss)will she make? Draw a graph to illustrate your answer.Your graph should include Veronica's demand,ATC,AVC,MC,and MR curves,the price she is charging,the quantity she is producing,and the area representing her profit (or loss).

(Essay)

4.9/5 (31)

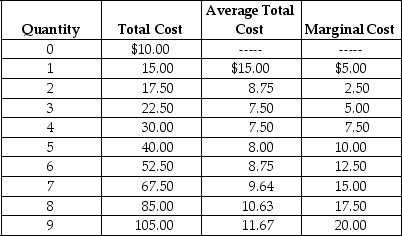

Table 8-3

Arnie sells basketballs in a perfectly competitive market.Table 8-3 summarises Arnie's output per day (Q),total cost (TC),average total cost (ATC)and marginal cost (MC).

-Refer to Table 8-3.What price (P)will Arnie charge and how much profit will he earn if the market price of basketballs is $12.50?

Arnie sells basketballs in a perfectly competitive market.Table 8-3 summarises Arnie's output per day (Q),total cost (TC),average total cost (ATC)and marginal cost (MC).

-Refer to Table 8-3.What price (P)will Arnie charge and how much profit will he earn if the market price of basketballs is $12.50?

(Multiple Choice)

4.8/5 (42)

If,for a perfectly competitive firm,price exceeds the marginal cost of production,the firm should

(Multiple Choice)

4.9/5 (37)

Perfectly competitive industries tend to produce low-priced,low-technology products.

(True/False)

4.9/5 (34)

Figure 8-7  Figure 8-7 shows cost and demand curves facing a profit-maximising,perfectly competitive firm.

-Refer to Figure 8-7.Identify the firm's short-run supply curve.

Figure 8-7 shows cost and demand curves facing a profit-maximising,perfectly competitive firm.

-Refer to Figure 8-7.Identify the firm's short-run supply curve.

(Multiple Choice)

4.9/5 (42)

If a firm in a perfectly competitive industry introduces a lower-cost way of producing an existing product,the firm will be able to earn economic profits in the long run.

(True/False)

4.8/5 (36)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)