Exam 12: Firms in Perfectly Competitive Markets

Exam 1: Economics: Foundations and Models444 Questions

Exam 2: Trade-Offs, Comparative Advantage, and the Market System498 Questions

Exam 3: Where Prices Come From: the Interaction of Demand and Supply475 Questions

Exam 4: Economic Efficiency, Government Price Setting, and Taxes419 Questions

Exam 5: Externalities, Environmental Policy, and Public Goods266 Questions

Exam 6: Elasticity: the Responsiveness of Demand and Supply295 Questions

Exam 7: The Economics of Health Care334 Questions

Exam 8: Firms, the Stock Market, and Corporate Governance278 Questions

Exam 9: Comparative Advantage and the Gains From International Trade379 Questions

Exam 10: Consumer Choice and Behavioral Economics302 Questions

Exam 11: Technology, Production, and Costs330 Questions

Exam 12: Firms in Perfectly Competitive Markets298 Questions

Exam 13: Monopolistic Competition: the Competitive Model in a More Realistic Setting276 Questions

Exam 14: Oligopoly: Firms in Less Competitive Markets262 Questions

Exam 15: Monopoly and Antitrust Policy271 Questions

Exam 16: Pricing Strategy263 Questions

Exam 17: The Markets for Labor and Other Factors of Production286 Questions

Exam 18: Public Choice, Taxes, and the Distribution of Income258 Questions

Exam 19: GDP: Measuring Total Production and Income266 Questions

Exam 20: Unemployment and Inflation292 Questions

Exam 21: Economic Growth, the Financial System, and Business Cycles257 Questions

Exam 22: Long-Run Economic Growth: Sources and Policies268 Questions

Exam 23: Aggregate Expenditure and Output in the Short Run306 Questions

Exam 24: Aggregate Demand and Aggregate Supply Analysis284 Questions

Exam 25: Money, Banks, and the Federal Reserve System280 Questions

Exam 26: Monetary Policy277 Questions

Exam 27: Fiscal Policy303 Questions

Exam 28: Inflation, Unemployment, and Federal Reserve Policy257 Questions

Exam 29: Macroeconomics in an Open Economy278 Questions

Exam 30: The International Financial System262 Questions

Select questions type

In the mid-1990s, cattle ranchers in the United States kept raising cattle even though prices were at a ten-year low and below average total cost. What is the likely explanation for this?

Free

(Multiple Choice)

4.8/5  (36)

(36)

Correct Answer: Verified

Verified

A

In an increasing-cost industry, the long-run supply curve is upward sloping.

Free

(True/False)

5.0/5 (28)

Correct Answer:Verified

True

Which of the following is a characteristic of a monopoly?

Free

(Multiple Choice)

4.8/5 (45)

Correct Answer:Verified

B

Figure 12-14  -If, in a perfectly competitive industry, the market price facing a firm is below its average total cost but above average variable cost at the output where marginal cost equals marginal revenue,

-If, in a perfectly competitive industry, the market price facing a firm is below its average total cost but above average variable cost at the output where marginal cost equals marginal revenue,

(Multiple Choice)

4.9/5 (42)

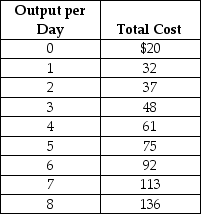

Suppose Veronica sells teapots in the perfectly competitive teapot market. Her output per day and her costs are as follows:

Suppose the current equilibrium price in the teapot market is $15. To maximize profit, how many teapots will Veronica produce, what price will she charge, and how much profit (or loss) will she make? Draw a graph to illustrate your answer. Your graph should include Veronica's demand, ATC, AVC, MC, and MR curves, the price she is charging, the quantity she is producing, and the area representing her profit (or loss).

Suppose the current equilibrium price in the teapot market is $15. To maximize profit, how many teapots will Veronica produce, what price will she charge, and how much profit (or loss) will she make? Draw a graph to illustrate your answer. Your graph should include Veronica's demand, ATC, AVC, MC, and MR curves, the price she is charging, the quantity she is producing, and the area representing her profit (or loss).

(Essay)

5.0/5 (29)

In a graph that illustrates a perfectly competitive firm, marginal revenue is

(Multiple Choice)

4.8/5 (36)

Figure 12-4  Figure 12-4 shows the cost and demand curves for a profit-maximizing firm in a perfectly competitive market.

-Refer to Figure 12-4. What is the amount of its total fixed cost?

Figure 12-4 shows the cost and demand curves for a profit-maximizing firm in a perfectly competitive market.

-Refer to Figure 12-4. What is the amount of its total fixed cost?

(Multiple Choice)

4.9/5 (41)

In August 2008, Ethan Nicholas developed the iShoot application for the apple iPhone 3G, and within five months had earned $800,000 from this program. By May 2009, Nicholas had dropped the price from $4.99 to $1.99 in an attempt to maintain sales. This example indicates that in a competitive market,

(Multiple Choice)

4.8/5 (34)

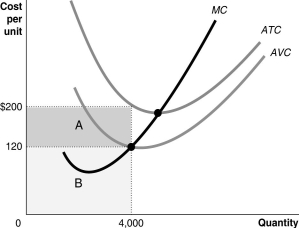

Figure 12-8  -Refer to Figure 12-8. Suppose the firm produces 4,000 units. What does the shaded area labeled B represent?

-Refer to Figure 12-8. Suppose the firm produces 4,000 units. What does the shaded area labeled B represent?

(Multiple Choice)

4.8/5 (41)

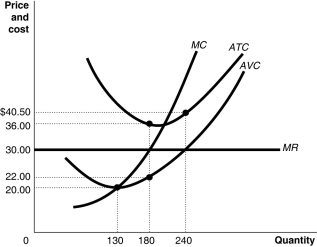

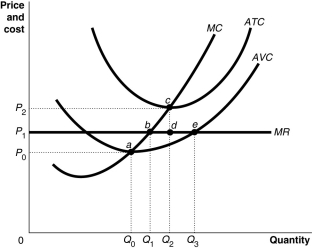

Figure 12-18  -Use the figure above to answer the following questions.

a. How can you determine that the figure represents a graph of a perfectly competitive firm? Be specific; indicate which curve gives you the information and how you use this information to arrive at your conclusion.

b. What is the market price?

c. What is the profit-maximizing output?

d. What is total revenue at the profit-maximizing output?

e. What is the total cost at the profit-maximizing output?

f. What is the profit or loss at the profit-maximizing output?

g. What is the firm's total fixed cost?

h. What is the total variable cost?

i. Identify the firm's short-run supply curve.

j. Is the industry in a long-run equilibrium?

k. If it is not in long-run equilibrium, what will happen in this industry to restore long-run equilibrium?

l. In long-run equilibrium, what is the firm's profit maximizing quantity?

-Use the figure above to answer the following questions.

a. How can you determine that the figure represents a graph of a perfectly competitive firm? Be specific; indicate which curve gives you the information and how you use this information to arrive at your conclusion.

b. What is the market price?

c. What is the profit-maximizing output?

d. What is total revenue at the profit-maximizing output?

e. What is the total cost at the profit-maximizing output?

f. What is the profit or loss at the profit-maximizing output?

g. What is the firm's total fixed cost?

h. What is the total variable cost?

i. Identify the firm's short-run supply curve.

j. Is the industry in a long-run equilibrium?

k. If it is not in long-run equilibrium, what will happen in this industry to restore long-run equilibrium?

l. In long-run equilibrium, what is the firm's profit maximizing quantity?

(Essay)

4.9/5 (43)

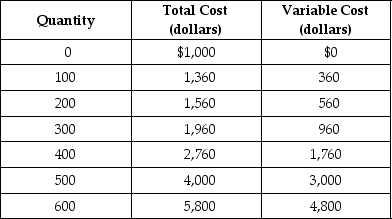

Table 12-1

Table 12-1 shows the short-run cost data of a perfectly competitive firm that produces plastic camera cases. Assume that output can only be increased in batches of 100 units.

-Refer to Table 12-1. Suppose the fixed cost of production rises by $500 and the price per unit is still $8. What happens to the firm's profit-maximizing output level?

Table 12-1 shows the short-run cost data of a perfectly competitive firm that produces plastic camera cases. Assume that output can only be increased in batches of 100 units.

-Refer to Table 12-1. Suppose the fixed cost of production rises by $500 and the price per unit is still $8. What happens to the firm's profit-maximizing output level?

(Multiple Choice)

4.8/5 (28)

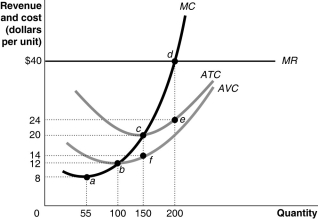

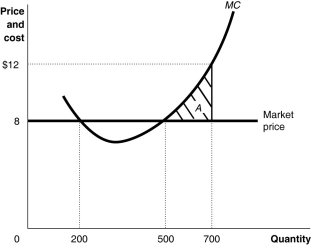

Figure 12-9  Figure 12-9 shows cost and demand curves facing a profit-maximizing, perfectly competitive firm.

-A perfectly competitive firm produces 3,000 units of a good at a total cost of $36,000. The fixed cost of production is $20,000. The price of each good is $10. Should the firm continue to produce in the short run?

Figure 12-9 shows cost and demand curves facing a profit-maximizing, perfectly competitive firm.

-A perfectly competitive firm produces 3,000 units of a good at a total cost of $36,000. The fixed cost of production is $20,000. The price of each good is $10. Should the firm continue to produce in the short run?

(Multiple Choice)

4.9/5 (39)

Why would a company continue to operate for many years while never once turning a profit rather than shut down immediately? Using revenue and cost analysis, explain when the company would shut down.

(Essay)

4.8/5 (33)

Suppose the equilibrium price in a perfectly competitive industry is $10 and a firm in the industry charges $12. Which of the following will happen?

(Multiple Choice)

4.8/5 (39)

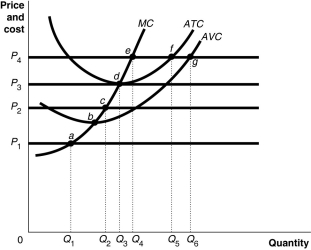

Figure 12-13  -In long-run perfectly competitive equilibrium, which of the following is false?

-In long-run perfectly competitive equilibrium, which of the following is false?

(Multiple Choice)

4.8/5 (38)

Figure 12-4 Figure 12-4 shows the cost and demand curves for a profit-maximizing firm in a perfectly competitive market.

-Refer to Figure 12-4. If the market price is $30 and if the firm is producing output, what is the amount of its total variable cost?

(Multiple Choice)

4.9/5 (33)

If a typical firm in a perfectly competitive industry is earning profits, then

(Multiple Choice)

4.8/5 (27)

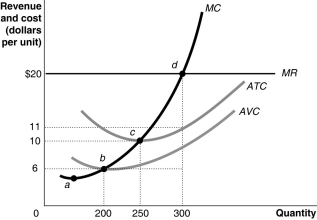

Figure 12-1  -Refer to Figure 12-1. If the firm is producing 200 units,

-Refer to Figure 12-1. If the firm is producing 200 units,

(Multiple Choice)

4.8/5 (39)

Figure 12-10  -In the short run, a firm that incurs losses might choose to produce rather than shut down if the amount of its revenue is less than its fixed cost.

-In the short run, a firm that incurs losses might choose to produce rather than shut down if the amount of its revenue is less than its fixed cost.

(True/False)

4.8/5 (38)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)