Exam 11: Technology, Production, and Costs

Exam 1: Economics: Foundations and Models444 Questions

Exam 2: Trade-Offs, Comparative Advantage, and the Market System498 Questions

Exam 3: Where Prices Come From: the Interaction of Demand and Supply475 Questions

Exam 4: Economic Efficiency, Government Price Setting, and Taxes419 Questions

Exam 5: Externalities, Environmental Policy, and Public Goods266 Questions

Exam 6: Elasticity: the Responsiveness of Demand and Supply295 Questions

Exam 7: The Economics of Health Care334 Questions

Exam 8: Firms, the Stock Market, and Corporate Governance278 Questions

Exam 9: Comparative Advantage and the Gains From International Trade379 Questions

Exam 10: Consumer Choice and Behavioral Economics302 Questions

Exam 11: Technology, Production, and Costs330 Questions

Exam 12: Firms in Perfectly Competitive Markets298 Questions

Exam 13: Monopolistic Competition: the Competitive Model in a More Realistic Setting276 Questions

Exam 14: Oligopoly: Firms in Less Competitive Markets262 Questions

Exam 15: Monopoly and Antitrust Policy271 Questions

Exam 16: Pricing Strategy263 Questions

Exam 17: The Markets for Labor and Other Factors of Production286 Questions

Exam 18: Public Choice, Taxes, and the Distribution of Income258 Questions

Exam 19: GDP: Measuring Total Production and Income266 Questions

Exam 20: Unemployment and Inflation292 Questions

Exam 21: Economic Growth, the Financial System, and Business Cycles257 Questions

Exam 22: Long-Run Economic Growth: Sources and Policies268 Questions

Exam 23: Aggregate Expenditure and Output in the Short Run306 Questions

Exam 24: Aggregate Demand and Aggregate Supply Analysis284 Questions

Exam 25: Money, Banks, and the Federal Reserve System280 Questions

Exam 26: Monetary Policy277 Questions

Exam 27: Fiscal Policy303 Questions

Exam 28: Inflation, Unemployment, and Federal Reserve Policy257 Questions

Exam 29: Macroeconomics in an Open Economy278 Questions

Exam 30: The International Financial System262 Questions

Select questions type

Is it possible for technological change to be negative? If so, give an example.

Free

(Essay)

4.9/5  (31)

(31)

Correct Answer: Verified

Verified

Technological change could be negative, for instance, when a natural disaster hits, or when a firm hires less-experienced workers. In these cases, the firm would produce a lower level of output with the same inputs.

Assume that you observe the long-run average cost curve of ACME Bookstores, a national chain. Starting from the point on the curve where output is zero and moving to the right which of the following lists the behavior of long-run average costs in the correct sequence (that is, which will be observed first, second, etc.)?

Free

(Multiple Choice)

4.9/5 (30)

Correct Answer:Verified

D

If the marginal cost curve is below the average variable cost curve, then

Free

(Multiple Choice)

4.8/5 (30)

Correct Answer:Verified

B

If 11 workers can produce 53 units of output while 12 workers can produce 56 units of output, what is the marginal product of the 12th worker?

(Multiple Choice)

4.8/5 (27)

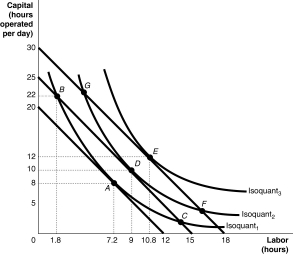

Figure 11-18  -Refer to Figure 11-18. Starting from point d a movement along isoquant1 to point f

-Refer to Figure 11-18. Starting from point d a movement along isoquant1 to point f

(Multiple Choice)

4.8/5 (32)

Figure 11-18

-Refer to Figure 11-18. Starting from point e, a movement along the isocost to point f

(Multiple Choice)

4.8/5 (30)

If a firm decreases its plant size and finds that its long-run average costs have decreased, then

(Multiple Choice)

4.8/5 (32)

The ABC Company manufactures routers that are used to provide high-speed Internet service. ABC sells an average of 1,000 routers each month, but to exhaust economies of scale in its industry ABC would have to sell 3,000 routers each month. Therefore,

(Multiple Choice)

4.8/5 (35)

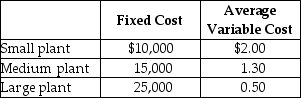

Table 11-9

-Refer to Table 11-9. Clock It To Me manufactures clock radios. The table above shows estimates of fixed cost per period and average variable cost for three possible plant sizes.

a. You are employed as the company's cost accountant and have been asked to prepare cost estimates for various output levels for each of the three possible plant sizes. Record your calculations in the table below.

Average Cost of Production

-Refer to Table 11-9. Clock It To Me manufactures clock radios. The table above shows estimates of fixed cost per period and average variable cost for three possible plant sizes.

a. You are employed as the company's cost accountant and have been asked to prepare cost estimates for various output levels for each of the three possible plant sizes. Record your calculations in the table below.

Average Cost of Production

b. For each of the three output levels, which plant size will generate the lowest average total cost of production?

c. Suppose the firm currently sells 8,000 clock radios per period (using the optimal plant size for this output level). Now, however, it has just secured a long-term contract to supply 20,000 clock radios per period. In the short run, what is the average total cost of producing 20,000 clock radios? Provide a numerical value based on your answer in part a.

d. What happens to average total cost of production in the long run? Provide a numerical value based on your answer in part a.

b. For each of the three output levels, which plant size will generate the lowest average total cost of production?

c. Suppose the firm currently sells 8,000 clock radios per period (using the optimal plant size for this output level). Now, however, it has just secured a long-term contract to supply 20,000 clock radios per period. In the short run, what is the average total cost of producing 20,000 clock radios? Provide a numerical value based on your answer in part a.

d. What happens to average total cost of production in the long run? Provide a numerical value based on your answer in part a.

(Essay)

4.9/5 (31)

Marginal cost is calculated for a particular increase in output by

(Multiple Choice)

4.9/5 (29)

If a firm is experiencing diseconomies of scale, its long-run average cost curve is increasing.

(True/False)

5.0/5 (35)

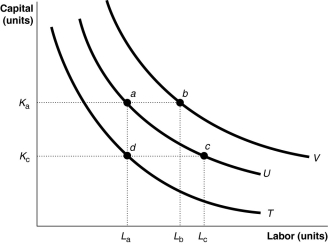

Figure 11-12  -Refer to Figure 11-12. Which of the following statements about the input combinations shown in the diagram is false?

-Refer to Figure 11-12. Which of the following statements about the input combinations shown in the diagram is false?

(Multiple Choice)

4.8/5 (34)

Who was the economist who first analyzed the advantages of specialization and the division of labor?

(Multiple Choice)

4.9/5 (32)

Use a long-run average cost curve graph to illustrate how diseconomies of scale would not make it beneficial for two companies to go through with a merger.

(Essay)

4.9/5 (38)

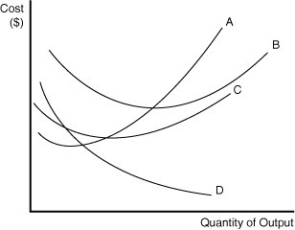

Figure 11-6  Figure 11-6 contains information about the short-run cost structure of a firm.

-Refer to Figure 11-6. In the figure above, which letter represents the marginal cost curve?

Figure 11-6 contains information about the short-run cost structure of a firm.

-Refer to Figure 11-6. In the figure above, which letter represents the marginal cost curve?

(Multiple Choice)

4.8/5 (27)

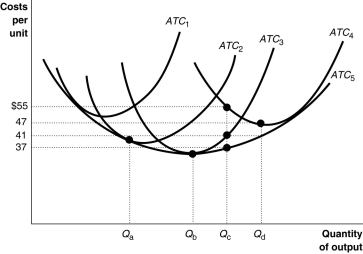

Figure 11-10  -Refer to Figure 11-10. Identify the minimum efficient scale of production.

-Refer to Figure 11-10. Identify the minimum efficient scale of production.

(Multiple Choice)

4.8/5 (29)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)