Exam 19: Corporations: Distributions Not in Complete Liquidation

Exam 1: An Introduction to Taxation and Understanding the Federal Tax Law211 Questions

Exam 2: Working with the Tax Law102 Questions

Exam 3: Computing the Tax180 Questions

Exam 4: Gross Income: Concepts and Inclusions125 Questions

Exam 5: Gross Income: Exclusions113 Questions

Exam 6: Deductions and Losses: In General156 Questions

Exam 7: Deductions and Losses: Certain Business Expenses and Losses94 Questions

Exam 8: Depreciation, Cost Recovery, Amortization, and Depletion120 Questions

Exam 9: Deductions: Employee and Self-Employed-Related Expenses153 Questions

Exam 10: Deductions and Losses: Certain Itemized Deductions104 Questions

Exam 11: Investor Losses130 Questions

Exam 12: Tax Credits and Payments111 Questions

Exam 13: Property Transactions: Determination of Gain or Loss, Basis Considerations, and Nontaxable Exchanges285 Questions

Exam 14: Property Transactions: Capital Gains and Losses, Section 1231, and Recapture Provisions167 Questions

Exam 15: Taxing Business Income60 Questions

Exam 16: Accounting Periods and Methods88 Questions

Exam 17: Corporations: Introduction and Operating Rules108 Questions

Exam 18: Corporations: Organization and Capital Structure109 Questions

Exam 19: Corporations: Distributions Not in Complete Liquidation185 Questions

Exam 20: Corporations: Distributions in Complete Liquidation and an Overview of Reorganizations71 Questions

Exam 21: Partnerships248 Questions

Exam 22: S Corporations129 Questions

Exam 23: Exempt Entities153 Questions

Exam 24: Multistate Corporate Taxation204 Questions

Exam 25: Taxation of International Transactions146 Questions

Exam 26: Tax Practice and Ethics184 Questions

Exam 27: The Federal Gift and Estate Taxes141 Questions

Exam 28: Income Taxation of Trusts and Estates161 Questions

Select questions type

Corporate shareholders generally receive less favorable tax treatment from a qualifying stock redemption than from a dividend distribution.

(True/False)

4.9/5  (37)

(37)

Silver Corporation, a calendar year taxpayer, has taxable income of $550,000. Among its transactions for the year are the following:  Disregarding any provision for Federal income taxes, Silver Corporation's current E & P is:

Disregarding any provision for Federal income taxes, Silver Corporation's current E & P is:

(Multiple Choice)

4.8/5 (43)

To determine current E & P, taxable income must be increased for any dividends received deduction.

(True/False)

4.9/5 (28)

Briefly describe the reason a corporation might distribute a property dividend to a shareholder in lieu of a cash distribution. Describe the tax effects of the property distribution on the shareholder and on the corporation.

(Essay)

4.8/5 (24)

Tracy and Lance, equal shareholders in Macaw Corporation, receive $600,000 each in distributions on December 31 of the current year. Macaw's current year taxable income is $1 million and it has no accumulated E & P. Last year, Macaw sold an appreciated asset for $1,200,000 (basis of $400,000). Payment for one-half of the sale of the asset was made this year. How much of Tracy's distribution will be taxed as a dividend?

(Multiple Choice)

4.8/5 (37)

Using the legend provided, classify each statement accordingly. In All cases, assume that taxable income is being adjusted to arrive at current E & P for 2018.

a. Increase

b. Decrease

c. No effect

-Penalties paid to state government for failure to comply with state law.

(Short Answer)

4.8/5 (37)

Hawk Corporation has 2,000 shares of stock outstanding: Marina owns 800 shares, Russell owns 500 shares, Velvet Partnership owns 400 shares, and Yellow Corporation owns 300 shares. Marina and Russell, unrelated individuals, are equal partners of Velvet Partnership. Marina owns 35% of the stock in Yellow Corporation.

a. Applying the § 318 stock attribution rules, determine how many shares in Hawk Corporation each shareholder owns, directly and indirectly:

Marina: Russell:

Velvet Partnership: Yellow Corporation:

b. Assume, instead, that Marina owns 60% of Yellow Corporation. How many shares does

Marina own, directly and indirectly, in Hawk Corporation?

(Essay)

4.8/5 (42)

Purple Corporation has accumulated E & P of $100,000 on January 1, 2018. In 2018, Purple has current E & P of $130,000 (before any distribution). On December 31, 2018, the corporation distributes $250,000 to its sole shareholder, Cindy (an individual). Purple Corporation's E & P as of January 1, 2019 is:

(Multiple Choice)

4.9/5 (32)

Pink Corporation declares a nontaxable dividend payable in rights to subscribe to common stock. Each right entitles the holder to purchase one share of stock for $25. One right is issued for every two shares of stock owned. Jocelyn owns 100 shares of stock in Pink, which she purchased three years ago for $3,000. At the time of the distribution, the value of the stock is $45 per share and the value of the rights is $2 per share. Jocelyn receives 50 rights. She exercises 25 rights and sells the remaining 25 rights three months later for $2.50 per right.

(Multiple Choice)

4.9/5 (30)

What are the requirements that must be satisfied for a distribution to qualify under § 302(b)(2) as a disproportionate redemption?

(Essay)

4.8/5 (47)

If there is sufficient E & P, a distribution of nonconvertible preferred stock to common shareholders is taxable.

(True/False)

4.8/5 (30)

Do noncorporate and corporate shareholders typically have the same preference for the tax treatment of a stock redemption? Explain.

(Essay)

4.9/5 (27)

Maria and Christopher each own 50% of Cockatoo Corporation, a calendar year taxpayer. Distributions fromCockatoo are: $750,000 to Maria on April 1 and $250,000 to Christopher on May 1. Cockatoo's current E & P is $300,000 and its accumulated E & P is $600,000. How much of the accumulated E & P is allocated to Christopher's distribution?

(Multiple Choice)

4.9/5 (38)

The rules used to determine the taxability of stock dividends also apply to distributions of stock rights.

(True/False)

5.0/5 (41)

Constructive dividends do not need to satisfy the legal requirements for a dividend as set forth by applicable state law.

(True/False)

4.8/5 (35)

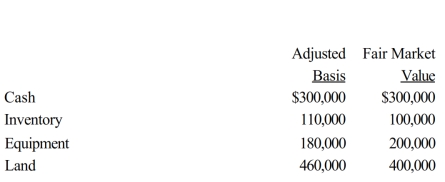

The stock in Crimson Corporation is owned by Angel and Melawi, who are unrelated. Angel owns 60% and Melawi owns 40% of the stock. All of Crimson Corporation's assets were acquired by purchase. The following assets are to be distributed in complete liquidation of Crimson Corporation:

a. What gain or loss, if any, would Crimson Corporation recognize if it distributes the cash, inventory, and equipment to Angel and the land to Melawi?

b. What gain or loss, if any, would Crimson Corporation recognize if it distributes the equipment and land to Angel and the cash and inventory to Melawi?

a. What gain or loss, if any, would Crimson Corporation recognize if it distributes the cash, inventory, and equipment to Angel and the land to Melawi?

b. What gain or loss, if any, would Crimson Corporation recognize if it distributes the equipment and land to Angel and the cash and inventory to Melawi?

(Essay)

4.7/5 (34)

In a property distribution, the amount of dividend income recognized by a shareholder is always reduced by the amount of liability assumed by a shareholder.

(True/False)

4.9/5 (37)

Using the legend provided, classify each statement accordingly. In all cases, assume that taxable income is being adjusted to arrive at current E & P for 2018.

a. Increase

b. Decrease

c. No effect

-Meal expense not deducted in 2018 because of the 50% limitation.

(Short Answer)

4.8/5 (36)

Corporate distributions are presumed to be paid out of E & P and are treated as dividends unless the parties to the transaction can show otherwise.

(True/False)

4.8/5 (44)

Gold Corporation has accumulated E & P of $2 million as of January 1 of the current year. During the year, it expects to have earnings from operations of $1,680,000 and to distribute $900,000 in cash to shareholders. Gold Corporation also expects to sell an asset for a loss of $2 million. Thus, it anticipates incurring a deficit of $320,000 for the year. What can Gold do to minimize the amount of dividend income to its shareholders?

(Essay)

5.0/5 (47)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)