Exam 3: Consolidations-Subsequent to the Date of Acquisition

Exam 1: The Equity Method of Accounting for Investments119 Questions

Exam 2: Consolidation of Financial Information115 Questions

Exam 3: Consolidations-Subsequent to the Date of Acquisition120 Questions

Exam 4: Consolidated Financial Statements and Outside Ownership117 Questions

Exam 5: Consolidated Financial Statements - Intra-Entity Asset Transactions127 Questions

Exam 6: Variable Interest Entities, Intra-Entity Debt, Consolidated Cash Flo115 Questions

Exam 7: Consolidated Financial Statements - Ownership Patterns and Income118 Questions

Exam 8: Segment and Interim Reporting113 Questions

Exam 9: Foreign Currency Transactions and Hedging Foreign Exchange Risk93 Questions

Exam 10: Translation of Foreign Currency Financial Statements97 Questions

Exam 11: Worldwide Accounting Diversity and International Standards60 Questions

Exam 12: Financial Reporting and the Securities and Exchange Commission77 Questions

Exam 13: Accounting for Legal Reorganizations and Liquidations82 Questions

Exam 14: Partnerships: Formation and Operations88 Questions

Exam 15: Partnerships: Termination and Liquidation70 Questions

Exam 16: Accounting for State and Local Governments78 Questions

Exam 17: Accounting for State and Local Governments46 Questions

Exam 18: Accounting and Reporting for Private Not-For-Profit Organizations62 Questions

Exam 19: Accounting for Estates and Trusts80 Questions

Select questions type

Figure:

Watkins, Inc. acquires all of the outstanding stock of Glen Corporation on January 1, 2010. At that date, Glen owns only three assets and has no liabilities: Book Fair Value Value Inventory (FIFO method) \ 40,000 \ 50,000 Equipment (10-year life) 80,000 75,000 Building (20-year life) 200,000 300,000

-If Watkins pays $450,000 in cash for Glen, and Glen earns $50,000 in net income and pays $20,000 in dividends during 2010, what amount would be reflected in consolidated net income for 2010 as a result of the acquisition?

(Multiple Choice)

4.9/5  (39)

(39)

Which one of the following varies between the equity, initial value, and partial equity methods of accounting for an investment?

(Multiple Choice)

4.8/5 (34)

Harrison, Inc. acquires 100% of the voting stock of Rhine Company on January 1, 2010 for $400,000 cash. A contingent payment of $16,500 will be paid on April 15, 2011 if Rhine generates cash flows from operations of $27,000 or more in the next year. Harrison estimates that there is a 20% probability that Rhine will generate at least $27,000 next year, and uses an interest rate of 5% to incorporate the time value of money. The fair value of $16,500 at 5%, using a probability weighted approach, is $3,142.

-What will Harrison record as its Investment in Rhine on January 1, 2010?

(Multiple Choice)

4.9/5 (42)

When a company applies the partial equity method in accounting for its investment in a subsidiary and the subsidiary's equipment has a fair value greater than its book value, what consolidation worksheet entry is made in a year subsequent to the initial acquisition of the subsidiary? A) Retained earnings Investment in subsidiary B) Investment in subsidiary Retained earnings C) Investment in subsidiary Equity in subsidiary's income D) Equity in subsidiary's income Investment in subsidiary E) Retained earnings Additional paid-in capital

(Multiple Choice)

4.8/5 (43)

Kaye Company acquired 100% of Fiore Company on January 1, 2011. Kaye paid $1,000 excess consideration over book value which is being amortized at $20 per year. Fiore reported net income of $400 in 2011 and paid dividends of $100.

-Hoyt Corporation agreed to the following terms in order to acquire the net assets of Brown Company on January 1, 2011:

(1) To issue 400 shares of common stock ($10 par) with a fair value of $45 per share.

(2) To assume Brown's liabilities which have a fair value of $1,500.

On the date of acquisition, the consideration transferred for Hoyt's acquisition of Brown would be

(Multiple Choice)

4.9/5 (43)

When a company applies the initial method in accounting for its investment in a subsidiary and the subsidiary reports income in excess of dividends paid, what entry would be made for a consolidation worksheet? A) Retained earnings Investment in subsidiary B) Investment in subsidiary Retained earnings C) Investment in subsidiary Equity in subsidiary's income D) Equity in subsidiary's income Investment in subsidiary E) Additional paid-in capital Retained earnings

(Multiple Choice)

4.8/5 (35)

Fesler Inc. acquired all of the outstanding common stock of Pickett Company on January 1, 2010. Annual amortization of $22,000 resulted from this transaction. On the date of the acquisition, Fesler reported retained earnings of $520,000 while Pickett reported a $240,000 balance for retained earnings. Fesler reported net income of $100,000 in 2010 and $68,000 in 2011, and paid dividends of $25,000 in dividends each year. Pickett reported net income of $24,000 in 2010 and $36,000 in 2011, and paid dividends of $10,000 in dividends each year. Assume that Fesler's reported net income includes Equity in Subsidiary Income.

-If the parent's net income reflected use of the initial value method, what were the consolidated retained earnings on December 31, 2011?

(Essay)

4.8/5 (37)

One company acquires another company in a combination accounted for as an acquisition. The acquiring company decides to apply the equity method in accounting for the combination. What is one reason the acquiring company might have made this decision?

(Multiple Choice)

4.8/5 (28)

How is the fair value allocation of an intangible asset allocated to expense when the asset has no legal, regulatory, contractual, competitive, economic, or other factors that limit its life?

(Multiple Choice)

4.8/5 (30)

Figure:

Watkins, Inc. acquires all of the outstanding stock of Glen Corporation on January 1, 2010. At that date, Glen owns only three assets and has no liabilities: Book Fair Value Value Inventory (FIFO method) \ 40,000 \ 50,000 Equipment (10-year life) 80,000 75,000 Building (20-year life) 200,000 300,000

-If Watkins pays $450,000 in cash for Glen, what amount would be represented as the subsidiary's Equipment in a consolidation at December 31, 2012, assuming the book value of the equipment at that date is still $80,000?

(Multiple Choice)

4.9/5 (40)

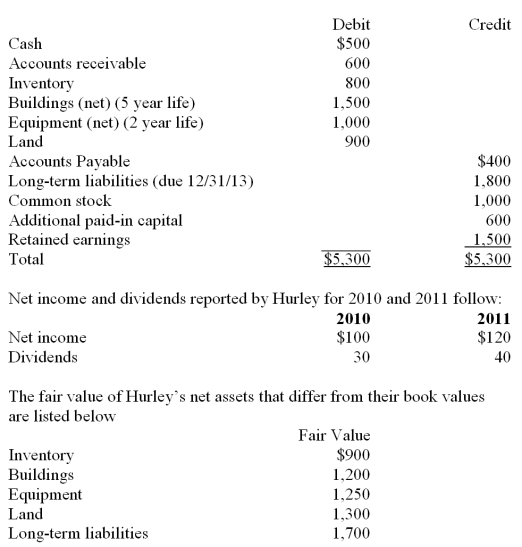

Figure:

Perry Company acquires 100% of the stock of Hurley Corporation on January 1, 2010, for $3,800 cash. As of that date Hurley has the following trial balance;  Any excess of consideration transferred over fair value of net assets acquired is considered goodwill with an indefinite life. FIFO inventory valuation method is used.

-Compute the amount of Hurley's inventory that would be reported in a January 1, 2010, consolidated balance sheet.

Any excess of consideration transferred over fair value of net assets acquired is considered goodwill with an indefinite life. FIFO inventory valuation method is used.

-Compute the amount of Hurley's inventory that would be reported in a January 1, 2010, consolidated balance sheet.

(Multiple Choice)

4.8/5 (34)

Which of the following will result in the recognition of an impairment loss on goodwill?

(Multiple Choice)

4.8/5 (42)

Figure:

On January 1, 2010, Cale Corp. paid $1,020,000 to acquire Kaltop Co. Kaltop maintained separate incorporation. Cale used the equity method to account for the investment. The following information is available for Kaltop's assets, liabilities, and stockholders' equity accounts: Book Value Fair Value Current assets \ 120,000 \ 120,000 Land 72,000 192,000 Building (twenty year life) 240,000 268,000 Equipment (ten year life) 540,000 516,000 Current liabilities 24,000 24,000 Long-term liabilities 120,000 120,000 Common stock 228,000 Additional paid-in capital 384,000 Retained earnings 216,000 Kaltop earned net income for 2010 of $126,000 and paid dividends of $48,000 during the year.

-The 2010 total amortization of allocations is calculated to be

(Multiple Choice)

4.8/5 (30)

Under the initial value method, when accounting for an investment in a subsidiary,

(Multiple Choice)

4.9/5 (31)

Beatty, Inc. acquires 100% of the voting stock of Gataux Company on January 1, 2010 for $500,000 cash. A contingent payment of $12,000 will be paid on April 1, 2011 if Gataux generates cash flows from operations of $26,500 or more in the next year. Beatty estimates that there is a 30% probability that Gataux will generate at least $26,500 next year, and uses an interest rate of 4% to incorporate the time value of money. The fair value of $12,000 at 4%, using a probability weighted approach, is $3,461.

-What will Beatty record as its Investment in Gataux on January 1, 2010?

(Multiple Choice)

4.8/5 (29)

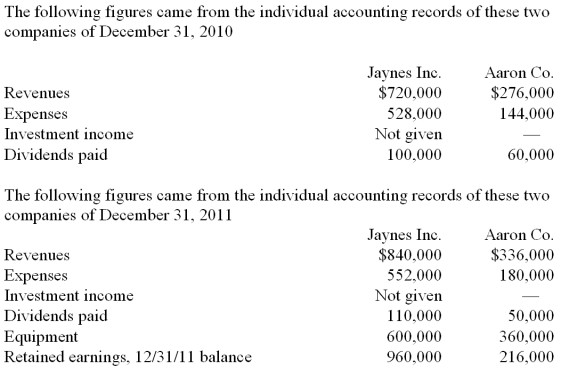

Jaynes Inc. acquired all of Aaron Co.'s common stock on January 1, 2010, by issuing 11,000 shares of $1 par value common stock. Jaynes' shares had a $17 per share fair value. On that date, Aaron reported a net book value of $120,000. However, its equipment (with a five-year remaining life) was undervalued by $6,000 in the company's accounting records. Any excess of consideration transferred over fair value of assets and liabilities is assigned to an unrecorded patent to be amortized over ten years.  -What was consolidated equipment as of December 31, 2011?

-What was consolidated equipment as of December 31, 2011?

(Essay)

4.9/5 (39)

Cashen Co. paid $2,400,000 to acquire all of the common stock of Janex Corp. on January 1, 2010. Janex's reported earnings for 2010 totaled $432,000, and it paid $120,000 in dividends during the year. The amortization of allocations related to the investment was $24,000. Cashen's net income, not including the investment, was $3,180,000, and it paid dividends of $900,000.

-On the consolidated financial statements for 2010, what amount should have been shown for consolidated dividends?

(Multiple Choice)

4.8/5 (29)

Figure:

On January 1, 2010, Cale Corp. paid $1,020,000 to acquire Kaltop Co. Kaltop maintained separate incorporation. Cale used the equity method to account for the investment. The following information is available for Kaltop's assets, liabilities, and stockholders' equity accounts: Book Value Fair Value Current assets \ 120,000 \ 120,000 Land 72,000 192,000 Building (twenty year life) 240,000 268,000 Equipment (ten year life) 540,000 516,000 Current liabilities 24,000 24,000 Long-term liabilities 120,000 120,000 Common stock 228,000 Additional paid-in capital 384,000 Retained earnings 216,000 Kaltop earned net income for 2010 of $126,000 and paid dividends of $48,000 during the year.

-At the end of 2010, the consolidation entry to eliminate Cale's accrual of Kaltop's earnings would include a credit to Investment in Kaltop Co. for

(Multiple Choice)

4.9/5 (40)

Yules Co. acquired Noel Co. in an acquisition transaction. Yules decided to use the partial equity method to account for the investment. The current balance in the investment account is $416,000. Describe in words how this balance was derived.

(Essay)

4.9/5 (37)

Avery Company acquires Billings Company in a combination accounted for as an acquisition and adopts the equity method to account for Investment in Billings. At the end of four years, the Investment in Billings account on Avery's books is $198,984. What items constitute this balance?

(Essay)

4.8/5 (36)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)