Exam 23: Associates and Joint Ventures

Exam 1: Nature and Regulation of Companies50 Questions

Exam 2: Financing Company Operations48 Questions

Exam 3: Company Operations49 Questions

Exam 4: Fundamental Concepts of Corporate Governance50 Questions

Exam 5: Fair Value Measurement50 Questions

Exam 6: Accounting for Company Income Tax18 Questions

Exam 7: Financial Instruments20 Questions

Exam 8: Foreign Currency Transactions and Forward Exchange Contracts20 Questions

Exam 9: Property, Plant and Equipment47 Questions

Exam 10: Leases18 Questions

Exam 11: Intangible Assets50 Questions

Exam 12: Business Combinations49 Questions

Exam 13: Impairment of Assets49 Questions

Exam 14: Disclosure: Legal Requirements and Accounting Polices50 Questions

Exam 15: Disclosure: Presentation of Financial Statements50 Questions

Exam 16: Disclosure: Statement of Cash Flows18 Questions

Exam 17: Disclosure: Translation of Financial Statements Into a Presentation Currency29 Questions

Exam 18: Consolidation: Controlled Entities49 Questions

Exam 19: Consolidation: Wholly Owned Subsidiaries47 Questions

Exam 20: Consolidation: Intragroup Transactions47 Questions

Exam 21: Consolidation: Non-Controlling Interest50 Questions

Exam 22: Consolidation: Other Issues48 Questions

Exam 23: Associates and Joint Ventures48 Questions

Exam 24: Investments in Joint Arrangements23 Questions

Exam 25: Insolvency and Liquidation46 Questions

Select questions type

Which of the following is not one of the three levels of control that one entity can exercise over another?

(Multiple Choice)

4.9/5  (29)

(29)

Where an entity prepares consolidated financial statements and has an investment in an associate,they have a choice of applying the equity method on consolidation or directly in their own books.

(True/False)

4.9/5 (37)

For the purposes of equity accounting,significant influence is defined as the power of an investor to:

(Multiple Choice)

4.7/5 (33)

When goodwill in an associate is acquired by an investor,the amortisation of goodwill is:

(Multiple Choice)

4.8/5 (42)

A joint arrangement is defined in AASB 128 Investments in Associates as an arrangement between two or more entities whereby the entities have joint control of another entity.

(True/False)

4.8/5 (35)

Where the investor does not prepare consolidated financial statements and a dividend is received from an associate,the entry in the investor's books on receipt of the dividend involves a credit adjustment against dividend revenue.

(True/False)

4.8/5 (45)

Where there are transactions between the investor and associate that result in an unrealised profit,the investor's share of the associate's profit is:

(Multiple Choice)

4.7/5 (35)

Fair value and goodwill adjustments arising on the acquisition of an associate are recognised separately in the books of the investor.

(True/False)

4.9/5 (35)

Equity adjustments must be made for transactions between the associate and the investor that give rise to unrealised profits or losses.

(True/False)

4.8/5 (42)

The basic premise under the equity method is that the investor is entitled to a share of the post-acquisition movements in the net assets of the associate.

(True/False)

4.8/5 (32)

Where an investor sells inventory to an associate in a prior year and the inventory is sold by the associate during the current year,the investment in associate account is:

(Multiple Choice)

4.9/5 (34)

An associate is defined in AASB 128 Investments in Associates as an entity over which the investor has control.

(True/False)

4.8/5 (48)

It is possible for more than one entity to exercise significant influence over an entity.

(True/False)

4.8/5 (41)

The investor recognises its shares of an associate's losses only to the point where the carrying amount of the investment reaches zero.

(True/False)

4.8/5 (27)

Where an investor sells inventory to an associate and the inventory is still on hand at the end of the year,the investor's share of the associate's profit is:

(Multiple Choice)

4.9/5 (39)

Only upstream transactions are adjusted for when making notional adjustment to post-acquisition profits of an associate prior to calculating the investor's share..

(True/False)

4.9/5 (40)

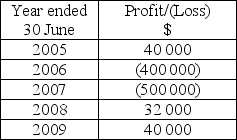

On 1 July 2004 Girls Ltd acquired 25% of the shares of Spice Ltd for $200 000.At that date the equity of Spice Ltd was $800 000,with all identifiable assets and liabilities being measured at fair value.Profits/(losses)made since the date of acquisition are as follows.

There have been no dividends paid or movements in reserves since the date of acquisition.

At 30 June 2009 the equity accounted balance of the investment in Spice was:

There have been no dividends paid or movements in reserves since the date of acquisition.

At 30 June 2009 the equity accounted balance of the investment in Spice was:

(Multiple Choice)

4.9/5 (44)

The equity method of accounting for an investment in an associate includes which of the following steps?

I II III IV

Recognise the initial investment at cost Yes Yes No No

Recognise the initial investment at fair value Yes No Yes No

Reduce the carrying amount by any dividends No Yes No Yes

Adjust the carrying amount by the investor's

Share of the associate's profit or loss No Yes Yes No

(Multiple Choice)

4.8/5 (30)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)