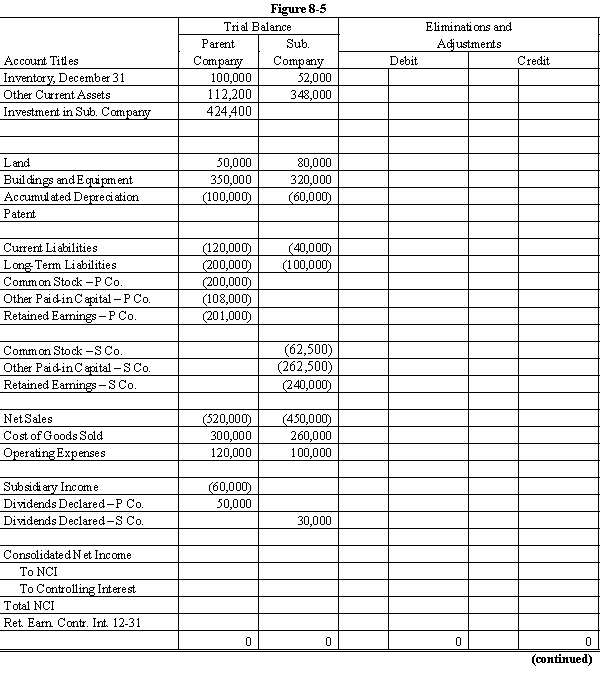

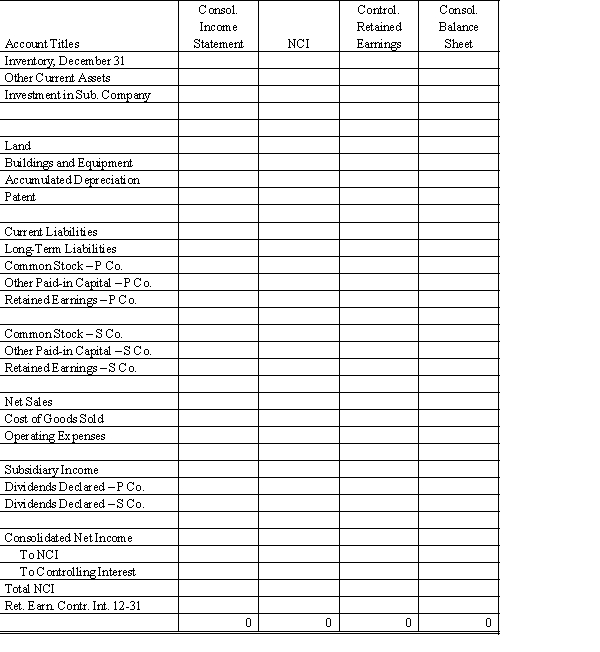

Essay

On January 1, 20X1, Parent Company purchased 8,000 shares of the common stock of Subsidiary Company for $350,000. On this date, Subsidiary had 20,000 shares of $5 par common stock authorized, 10,000 shares issued and outstanding. Other paid-in capital and retained earnings were $150,000 and $200,000 respectively. On January 1, 20X1, any excess of cost over book value is due to a patent, to be amortized over 15 years. Parent Company uses the simple equity method to account for its investment in Sub.

Subsidiary's net income and dividends for two years were:

On January 1, 20X2, Subsidiary Company sold an additional 2,500 shares of common stock to noncontrolling shareholders for $50 per share.

In the last quarter of 20X2, Subsidiary Company sold goods to Parent Company for $40,000. Subsidiary's usual gross profit on intercompany sales is 40%. On December 31, $7,500 of these goods are still in Parent's ending inventory.

Required:

Complete the Figure 8-5 worksheet for consolidated financial statements for 20X2.

Correct Answer:

Verified

Correct Answer:

Verified

Q1: On January 1, 20X1, Parent Company purchased

Q2: Which of the following situations is a

Q4: Paula Inc. purchased an 80% interest

Q6: Able Company owns an 80% interest in

Q7: On 1/1/X1 Poncho acquired an 80%

Q8: Apple Inc. owns a 90% interest in

Q9: Able Company owns an 80% interest in

Q10: Paul & Stephan: On January 1,

Q11: On January 1, 20X1, Parent Company purchased

Q21: Two types of intercompany stock purchases significantly