Exam 8: Profit Maximization and Competitive Supply

Exam 1: Preliminaries77 Questions

Exam 2: The Basics of Supply and Demand135 Questions

Exam 3: Consumer Behavior146 Questions

Exam 4: Individual and Market Demand173 Questions

Exam 5: Uncertainty and Consumer Behavior177 Questions

Exam 6: Production123 Questions

Exam 7: The Cost of Production166 Questions

Exam 8: Profit Maximization and Competitive Supply149 Questions

Exam 9: The Analysis of Competitive Markets177 Questions

Exam 10: Market Power: Monopoly and Monopsony158 Questions

Exam 11: Pricing With Market Power122 Questions

Exam 12: Monopolistic Competition and Oligopoly113 Questions

Exam 13: Game Theory and Competitive Strategy150 Questions

Exam 14: Markets for Factor Inputs123 Questions

Exam 15: Investment, Time, and Capital Markets153 Questions

Exam 16: General Equilibrium and Economic Efficiency111 Questions

Exam 17: Markets With Asymmetric Information130 Questions

Exam 18: Externalities and Public Goods123 Questions

Select questions type

If current output is less than the profit-maximizing output, then the next unit produced

Free

(Multiple Choice)

4.7/5  (38)

(38)

Correct Answer: Verified

Verified

C

Which of the following costs may provide barriers to entry in a market?

Free

(Multiple Choice)

4.9/5 (35)

Correct Answer:Verified

D

An industry analyst observes that in response to a small increase in price, a competitive firm's output sometimes rises a little and sometimes a lot. The best explanation for this finding is that

Free

(Multiple Choice)

4.9/5 (39)

Correct Answer:Verified

D

The textbook for your class was not produced in a perfectly competitive industry because

(Multiple Choice)

4.8/5 (40)

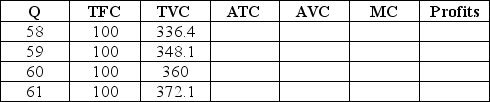

The table below lists the short-run costs for One Guy's Pizza. If One Guy's can sell all the output they produce for $12 per unit, how much should One Guy's produce to maximize profits? Does One Guy's Pizza earn an economic profit in the short-run?

(Essay)

4.9/5 (22)

Suppose a technological innovation shifts the marginal cost curve downward. Which one of the following cost curves does NOT shift?

(Multiple Choice)

4.7/5 (43)

Several years ago, Alcoa was effectively the sole seller of aluminum because the firm owned nearly all of the aluminum ore reserves in the world. This market was not perfectly competitive because this situation violated the:

(Multiple Choice)

4.9/5 (32)

If a competitive firm has a U-shaped marginal cost curve then

(Multiple Choice)

4.7/5 (32)

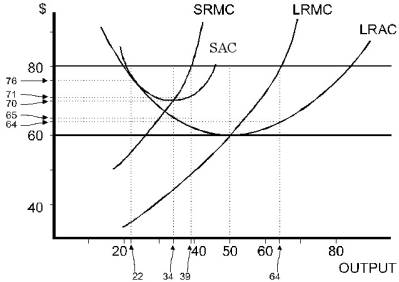

Figure 8.2

-Refer to Figure 8.2. At P = $80, how much is profit in the short run?

Figure 8.2

-Refer to Figure 8.2. At P = $80, how much is profit in the short run?

(Multiple Choice)

5.0/5 (35)

Consider the following statements when answering this question

I. In the long-run equilibrium of a perfectly competitive market, a firm's producer surplus equals the sum of the economic rents earned on its inputs to production.

II. In the long-run equilibrium of a perfectly competitive market, the amount of economic profit earned can differ across firms, but not the amount of producer surplus.

(Multiple Choice)

4.9/5 (35)

Ronny's Pizza House is a profit maximizing firm in a perfectly competitive local restaurant market, and their optimal output is 80 pizzas per day. The local government imposes a new tax of $250 per year on all restaurants that operate in the city. How does this affect Ronny's profit maximizing decisions?

(Multiple Choice)

4.9/5 (28)

The "perfect information" assumption of perfect competition includes all of the following except one. Which one?

(Multiple Choice)

4.8/5 (29)

In the short run, a perfectly competitive firm earning positive economic profit is

(Multiple Choice)

4.8/5 (29)

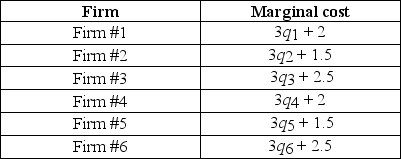

The marginal cost curves of six firms in an industry appear in the table below. If these firms behave competitively, determine the market supply curve. Calculate the elasticity of market supply at $5.

(Essay)

4.8/5 (38)

In the short run, a perfectly competitive profit maximizing firm that has not shut down

(Multiple Choice)

4.9/5 (25)

If price is between AVC and ATC, the best and most practical thing for a perfectly competitive firm to do is

(Multiple Choice)

4.7/5 (31)

One practical implication of a kinked market supply curve is that:

(Multiple Choice)

4.8/5 (39)

Use the following statements to answer this question:

I. An increase in the firm's fixed costs will also shift the firm's short-run supply curve to the left.

II. An increase in the firm's fixed costs will not shift the firm's short-run supply curve to the right or left, but it may alter how much of the marginal cost curve is used to form the short-run supply curve.

(Multiple Choice)

4.9/5 (35)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)