Exam 8: Profit Maximization and Competitive Supply

Exam 1: Preliminaries77 Questions

Exam 2: The Basics of Supply and Demand135 Questions

Exam 3: Consumer Behavior146 Questions

Exam 4: Individual and Market Demand173 Questions

Exam 5: Uncertainty and Consumer Behavior177 Questions

Exam 6: Production123 Questions

Exam 7: The Cost of Production166 Questions

Exam 8: Profit Maximization and Competitive Supply149 Questions

Exam 9: The Analysis of Competitive Markets177 Questions

Exam 10: Market Power: Monopoly and Monopsony158 Questions

Exam 11: Pricing With Market Power122 Questions

Exam 12: Monopolistic Competition and Oligopoly113 Questions

Exam 13: Game Theory and Competitive Strategy150 Questions

Exam 14: Markets for Factor Inputs123 Questions

Exam 15: Investment, Time, and Capital Markets153 Questions

Exam 16: General Equilibrium and Economic Efficiency111 Questions

Exam 17: Markets With Asymmetric Information130 Questions

Exam 18: Externalities and Public Goods123 Questions

Select questions type

Although the long-run equilibrium price of oil is $80 per barrel, some producers have much lower costs because their oil reserves are relatively close to the surface and are easier to extract. If the low-cost producers have a minimum LAC equal to $20 per barrel, then the difference ($60 per barrel) is:

(Multiple Choice)

4.8/5  (36)

(36)

Use the following statements to answer this question:

I. Markets that have only a few sellers cannot be highly competitive.

II. Markets with many sellers are always perfectly competitive.

(Multiple Choice)

4.8/5 (45)

An association of businesses that are jointly owned and operated by members for mutual benefit is a:

(Multiple Choice)

4.9/5 (38)

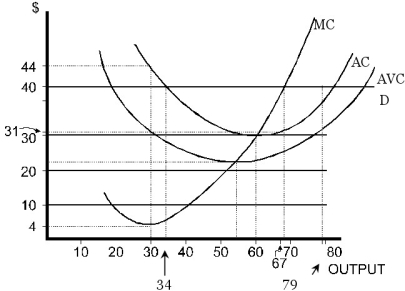

Consider the following diagram where a perfectly competitive firm faces a price of $40.  Figure 8.1

-Refer to Figure 8.1. The firm earns zero profit at what output?

Figure 8.1

-Refer to Figure 8.1. The firm earns zero profit at what output?

(Multiple Choice)

4.8/5 (35)

In the long-run equilibrium of a competitive market, the market supply and demand are:

Supply: P = 30 + 0.50Q

Demand: P = 100 - 1.5Q,

where P is dollars per unit and Q is rate of production and sales in hundreds of units per day. A typical firm in this market has a marginal cost of production expressed as:

MC = 3.0 + 15q.

a. Determine the market equilibrium rate of sales and price.

b. Determine the rate of sales by the typical firm.

c. Determine the economic rent that the typical firm enjoys. (Hint: Note that the marginal cost function is linear.)

d. If an output tax is imposed on ONE firm's output such that the ONE firm has a new marginal cost (including the tax) of:

MCt = 5 + 15q,

what will the firm's new rate of production be after the tax is imposed? How does this new production rate compare with the pre-tax rate? Is it as expected? Explain. Would the effect have been the same if the tax had been imposed on all firms equally? Explain.

(Essay)

4.8/5 (38)

In a supply-and-demand graph, producer surplus can be pictured as the

(Multiple Choice)

4.8/5 (36)

Consider the following diagram where a perfectly competitive firm faces a price of $40. Figure 8.1

-Refer to Figure 8.1. At the profit-maximizing level of output, total revenue is

(Multiple Choice)

4.8/5 (39)

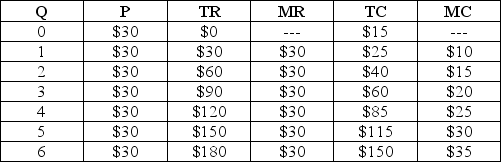

Table 8.1

-Refer to Table 8.1. The maximum profit available to the firm is

-Refer to Table 8.1. The maximum profit available to the firm is

(Multiple Choice)

4.9/5 (32)

A competitive firm sells its product at a price of $0.10 per unit. Its total and marginal cost functions are:

TC = 5 - 0.5Q + 0.001Q2

MC = -0.5 + 0.002Q,

where TC is total cost ($) and Q is output rate (units per time period).

a. Determine the output rate that maximizes profit or minimizes losses in the shortterm.

b. If input prices increase and cause the cost functions to become

TC = 5 - 0.10Q + 0.002Q2

MC = -0.10 + 0.004Q,

what will the new equilibrium output rate be? Explain what happened to the profit maximizing output rate when input prices were increased.

(Essay)

4.7/5 (37)

Sarah's Pretzel plant has the following short-run cost function: C(q, K) =  + 50K where q is Sarah's output level, w is the cost of a labor hour, and K is the number of pretzel machines Sarah leases. Sarah's short-run marginal cost curve is MC(q, K) =

+ 50K where q is Sarah's output level, w is the cost of a labor hour, and K is the number of pretzel machines Sarah leases. Sarah's short-run marginal cost curve is MC(q, K) =  . At the moment, Sarah leases 10 pretzel machines, the cost of a labor hour is $6.85, and she can sell all the output she produces at $35 per unit. If the cost per labor hour rises to $7.50, what happens to Sarah's optimal level of output and profits?

. At the moment, Sarah leases 10 pretzel machines, the cost of a labor hour is $6.85, and she can sell all the output she produces at $35 per unit. If the cost per labor hour rises to $7.50, what happens to Sarah's optimal level of output and profits?

(Essay)

4.9/5 (32)

Imposition of an output tax on all firms in a competitive industry will result in

(Multiple Choice)

4.8/5 (38)

When the price faced by a competitive firm was $5, the firm produced nothing in the short run. However, when the price rose to $10, the firm produced 100 tons of output. From this we can infer that

(Multiple Choice)

4.7/5 (26)

If the market price for a competitive firm's output doubles then

(Multiple Choice)

4.8/5 (35)

Suppose we plot the total revenue curve with quantity on the horizontal axis and revenue on the vertical axis (as in Figure 8.1 in the book). Under price-taking behavior, the total revenue curve should be:

(Multiple Choice)

4.7/5 (39)

Three hundred firms supply the market for paint. For fifty of the firms, their short-run average variable costs are minimized at $10 and short-run total costs are minimized at $15. For the remaining firms, the short-run average variable costs and short-run average total costs are minimized at $20 and $25, respectively. If each firm has a U-shaped marginal cost curve then the short-run market supply curve is

(Multiple Choice)

4.7/5 (32)

Consider the following statements when answering this question

I. In the long run, if a firm wants to remain in a competitive industry, then it needs to own resources that are in limited supply.

II. In this competitive market our firm's long-run survival depends only on the efficiency of our production process.

(Multiple Choice)

4.8/5 (33)

Suppose the state legislature in your state imposes a state licensing fee of $100 per year to be paid by all firms that file state tax revenue reports. This new business tax:

(Multiple Choice)

4.9/5 (43)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)