Exam 7: Inventory

Exam 1: An Overview of the Australian External Reporting Environment50 Questions

Exam 2: The Conceptual Framework of Accounting and Its Relevance to Financ62 Questions

Exam 3: Theories of Financial Accounting61 Questions

Exam 4: An Overview of Accounting for Assets62 Questions

Exam 5: Depreciation of Property, Plant and Equipment62 Questions

Exam 6: Revaluation and Impairment Testing of Non-Current Assets59 Questions

Exam 7: Inventory60 Questions

Exam 8: Accounting for Intangibles63 Questions

Exam 9: Accounting for Heritage Assets and Biological Assets61 Questions

Exam 10: An Overview of Accounting for Liabilities58 Questions

Exam 11: Accounting for Lease66 Questions

Exam 12: Set-Off and Extinguishment of Debt47 Questions

Exam 13: Accounting for Employee Benefits67 Questions

Exam 14: Share Capital and Reserves66 Questions

Exam 15: Accounting for Financial Instruments72 Questions

Exam 16: Revenue Recognition Issues64 Questions

Exam 17: The Statement of Comprehensive Income and Statement of Changes in E62 Questions

Exam 18: Accounting for Share-Based Payments62 Questions

Exam 19: Accounting for Income Taxes65 Questions

Exam 20: Cash-Flow Statements60 Questions

Exam 21: Accounting for the Extractive Industries60 Questions

Exam 22: Accounting for General Insurance Contracts58 Questions

Exam 23: Accounting for Superannuation Plans62 Questions

Exam 24: Events Occurring After Balance Sheet Date62 Questions

Exam 25: Segment Reporting61 Questions

Exam 26: Related-Party Disclosures60 Questions

Exam 27: Earnings Per Share62 Questions

Exam 28: Accounting for Group Structures69 Questions

Exam 29: Further Consolidation Issues I: Accounting for Intragroup Transact46 Questions

Exam 30: Further Consolidation Issues Ii: Accounting for Minority Interests34 Questions

Exam 31: Further Consolidation Issues Iii: Accounting for Indirect Ownershi38 Questions

Exam 32: Further Consolidation Issues Iv: Accounting for Changes in the Deg39 Questions

Exam 33: Accounting for Equity Investments67 Questions

Exam 33: Accounting for Equity Investments59 Questions

Exam 35: Accounting for Foreign Currency Transactions59 Questions

Exam 36: Translation of the Accounts of Foreign Operations42 Questions

Exam 37: Accounting for Corporate Social Responsibility59 Questions

Select questions type

Which accounting policy for manufacturing fixed costs is likely to favour managers whose firms are subject to political scrutiny?

(Multiple Choice)

4.8/5  (39)

(39)

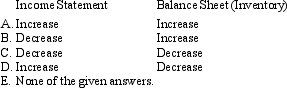

Kensington Ltd is an importer and retailer of European made glass crystals. For the year ended 30 June 2008, Kensington Ltd still holds 30 units of an item originally purchased for $10,000 each and a net realisable value of $8,000. On 1 June 2009 the TV show "Home Improvement" featured a similar item prompting an increase in demand for this glass crystal. Management believes that the net realisable value of this item is now $15,000. All 30 items remain unsold on 30 June 2009. What is the effect of holding this inventory on the income statement of Heffron Ltd for the years ended 30 June 2008 and 2009?

(Multiple Choice)

4.8/5 (43)

Bondi Ltd is a small sports shop. At the beginning of the period, Bondi Ltd had 30 tennis racquets on hand costing $50 each. On 31 October 2009, the shop sold 20 racquets to a tennis instructor for $80. A delivery of 50 racquets was received on 15 November 2009 at $50 but received 2% discount if the account is paid within 30 days. What are the appropriate journal entries to recognise above transactions using the periodic system?

(Multiple Choice)

4.8/5 (37)

Standard costs may be used to arrive at the cost of inventory only where standards are set at ideal levels and any costs arising from exceptional wastage are excluded from the cost of inventories:

(True/False)

4.8/5 (39)

Some biological assets may be covered by AASB 102 "Inventories":

(True/False)

4.8/5 (31)

Randwick Ltd has a year-end of 30 June 2009. During the year the following errors were discovereD.

-Merchandise inventory at the factory had been understated by $44,000.

-Goods on consignment from a supplier for $13,000 were included in inventory at the shops.

-Physical inventory for one warehouse had a shortage of $58,000

What is the net effect of above errors in the income statement and balance sheet (inventory) accounts of Randwick Ltd?

(Short Answer)

4.7/5 (34)

Use of the LIFO method has been deemed unacceptable under AASB 102 because?

(Multiple Choice)

4.8/5 (38)

The two main methods for dealing with fixed costs in relation to the production of inventory are:

(Multiple Choice)

4.8/5 (37)

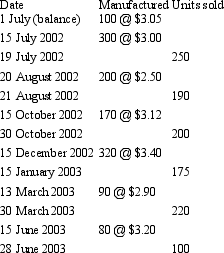

Rectangle Ltd manufactures cardboard boxes for a variety of purposes. The following information relates to the production of the extra large packing boxes used by removalists for the period ended 30 June 2003.

The company uses a perpetual inventory system. The net realisable value per extra large cardboard box is $3.15 at the end of the period. What are the costs of goods sold and the value of ending inventory for Rectangle Ltd assuming the LIFO cost-flow assumption is used?

The company uses a perpetual inventory system. The net realisable value per extra large cardboard box is $3.15 at the end of the period. What are the costs of goods sold and the value of ending inventory for Rectangle Ltd assuming the LIFO cost-flow assumption is used?

(Multiple Choice)

4.8/5 (33)

Las Vegas Ltd sells second hand luxury cars of various makes and models, and uses the FIFO cost flow assumption to ascertain the cost of ending inventory. This would be incorrect because:

(Multiple Choice)

4.9/5 (45)

The first-in, first-out (FIFO) method assumes that items remaining in inventory at the end of the period are those most recently purchased or produced.

(True/False)

4.8/5 (37)

Which of the following statements is correct with respect to positive accounting theory?

(Multiple Choice)

4.8/5 (37)

Paris Merchandising Ltd sells ladies skirts. The opening stock consisted of 300 skirts with purchase price of $50 each. Subsequent purchases during the period include: 400 at $60 each and another 200 for $70 each. A total of 700 skirts were sold during the period. What is ending inventory using FIFO method?

(Multiple Choice)

4.7/5 (34)

AASB 102 requires that the specific identification method of assigning cost to items of inventory be applieD.

(Multiple Choice)

4.7/5 (41)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)