Exam 10: Arbitrage Pricing Theory and Multifactor Models of Risk and Return

Exam 1: The Investment Environment51 Questions

Exam 2: Financial Markets, Asset Classes and Financial Instruments82 Questions

Exam 3: How Securities Are Traded65 Questions

Exam 4: Mutual Funds and Other Investment Companies59 Questions

Exam 5: Risk, Return, and the Historical Record64 Questions

Exam 6: Capital Allocation to Risky Assets59 Questions

Exam 7: Optimal Risky Portfolios63 Questions

Exam 8: Index Models76 Questions

Exam 9: The Capital Asset Pricing Model71 Questions

Exam 10: Arbitrage Pricing Theory and Multifactor Models of Risk and Return62 Questions

Exam 11: The Efficient Market Hypothesis42 Questions

Exam 12: Behavioural Finance and Technical Analysis41 Questions

Exam 13: Empirical Evidence on Security Returns41 Questions

Exam 14: Bond Prices and Yields110 Questions

Exam 15: The Term Structure of Interest Rates58 Questions

Exam 16: Managing Bond Portfolios69 Questions

Exam 17: Macroeconomic and Industry Analysis67 Questions

Exam 18: Equity Valuation Models106 Questions

Exam 19: Financial Statement Analysis71 Questions

Exam 20: Options Markets: Introduction88 Questions

Exam 21: Option Valuation85 Questions

Exam 22: Futures Markets85 Questions

Exam 23: Futures, Swaps, and Risk Management51 Questions

Exam 24: Portfolio Performance Evaluation68 Questions

Exam 25: International Diversification48 Questions

Exam 26: Hedge Funds46 Questions

Exam 27: The Theory of Active Portfolio Management48 Questions

Exam 28: Investment Policy and the Framework of the Cfa Institute76 Questions

Select questions type

Consider the one-factor APT.Assume that two portfolios, A and B, are well diversified.The betas of portfolios A and B are 1.0 and 1.5, respectively.The expected returns on portfolios A and B are 19% and 24%, respectively.Assuming no arbitrage opportunities exist, the risk-free rate of return must be

(Multiple Choice)

4.8/5  (19)

(19)

The ____________ provides an unequivocal statement on the expected return-beta relationship for all assets, whereas the _____________ implies that this relationship holds for all but perhaps a small number of securities.

(Multiple Choice)

4.7/5 (36)

Consider a single factor APT.Portfolio A has a beta of 1.0 and an expected return of 16%.Portfolio B has a beta of 0.8 and an expected return of 12%.The risk-free rate of return is 6%.If you wanted to take advantage of an arbitrage opportunity, you should take a short position in portfolio __________ and a long position in portfolio _______.

(Multiple Choice)

4.7/5 (33)

Consider the multifactor model APT with three factors.Portfolio A has a beta of 0.8 on factor 1, a beta of 1.1 on factor 2, and a beta of 1.25 on factor 3.The risk premiums on the factor 1, factor 2, and factor 3 are 3%, 5%, and 2%, respectively.The risk-free rate of return is 3%.The expected return on portfolio A is __________ if no arbitrage opportunities exist.

(Multiple Choice)

4.9/5 (32)

Consider the one-factor APT.The standard deviation of returns on a well-diversified portfolio is 19%.The standard deviation on the factor portfolio is 12%.The beta of the well-diversified portfolio is approximately

(Multiple Choice)

4.7/5 (27)

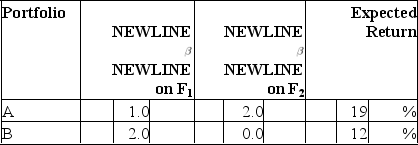

Consider the multifactor APT.There are two independent economic factors, F1andF2.The risk-free rate of return is 6%.The following information is available about two well-diversified portfolios:  Assuming no arbitrage opportunities exist, the risk premium on the factorF1portfolio should be

Assuming no arbitrage opportunities exist, the risk premium on the factorF1portfolio should be

(Multiple Choice)

4.9/5 (39)

Consider the one-factor APT.The variance of returns on the factor portfolio is 9%.The beta of a well-diversified portfolio on the factor is 1.25.The variance of returns on the well-diversified portfolio is approximately

(Multiple Choice)

4.9/5 (36)

Consider the multifactor APT with two factors.Stock A has an expected return of 17.6%, a beta of 1.45 on factor 1, and a beta of.86 on factor 2.The risk premium on the factor 1 portfolio is 3.2%.The risk-free rate of return is 5%.What is the risk-premium on factor 2 if no arbitrage opportunities exist?

(Multiple Choice)

4.8/5 (36)

In a multifactor APT model, the coefficients on the macro factors are often called

(Multiple Choice)

4.8/5 (42)

Black argues that past risk premiums on firm-characteristic variables, such as those described by Fama and French, are problematic because

(Multiple Choice)

4.9/5 (35)

A professional who searches for mispriced securities in specific areas such as merger-target stocks, rather than one who seeks strict (risk-free) arbitrage opportunities is engaged in

(Multiple Choice)

4.8/5 (35)

Consider the multifactor APT with two factors.The risk premiums on the factor 1 and factor 2 portfolios are 5% and 6%, respectively.Stock A has a beta of 1.2 on factor-1, and a beta of 0.7 on factor-2.The expected return on stock A is 17%.If no arbitrage opportunities exist, the risk-free rate of return is

(Multiple Choice)

4.8/5 (34)

A zero-investment portfolio with a positive expected return arises when

(Multiple Choice)

4.8/5 (35)

In a factor model, the return on a stock in a particular period will be related to

(Multiple Choice)

4.7/5 (38)

In the context of the Arbitrage Pricing Theory, as a well-diversified portfolio becomes larger, its nonsystematic risk approaches

(Multiple Choice)

4.8/5 (35)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)