Exam 11: Production and Cost Analysis I

Exam 1: Economics and Economic Reasoning158 Questions

Exam 2: The Production Possibility Model, Trade, and Globalization133 Questions

Exam 3: Economic Institutions163 Questions

Exam 4: Supply and Demand182 Questions

Exam 5: Using Supply and Demand163 Questions

Exam 6: Describing Supply and Demand: Elasticities216 Questions

Exam 7: Taxation and Government Intervention201 Questions

Exam 8: Market Failure Versus Government Failure197 Questions

Exam 9: Comparative Advantage, Exchange Rates, and Globalization118 Questions

Exam 10: International Trade Policy99 Questions

Exam 11: Production and Cost Analysis I194 Questions

Exam 12: Production and Cost Analysis II152 Questions

Exam 13: Perfect Competition170 Questions

Exam 14: Monopoly and Monopolistic Competition274 Questions

Exam 15: Oligopoly and Antitrust Policy142 Questions

Exam 16: Real-World Competition and Technology108 Questions

Exam 17: Work and the Labor Market150 Questions

Exam 18: Who Gets What the Distribution of Income131 Questions

Exam 19: The Logic of Individual Choice: the Foundation of Supply and Demand170 Questions

Exam 20: Game Theory, Strategic Decision Making, and Behavioral Economics103 Questions

Exam 21: Thinking Like a Modern Economist97 Questions

Exam 22: Behavioral Economics and Modern Economic Policy126 Questions

Exam 23: Microeconomic Policy, Economic Reasoning, and Beyond134 Questions

Exam 24: Economic Growth, Business Cycles, and Unemployment124 Questions

Exam 25: Measuring and Describing the Aggregate Economy229 Questions

Exam 26: The Keynesian Short-Run Policy Model: Demand-Side Policies220 Questions

Exam 27: The Classical Long-Run Policy Model: Growth and Supply-Side Policies133 Questions

Exam 28: The Financial Sector and the Economy214 Questions

Exam 29: Monetary Policy243 Questions

Exam 30: Financial Crises, Panics, and Unconventional Monetary Policy109 Questions

Exam 31: Deficits and Debt: the Austerity Debate150 Questions

Exam 32: The Fiscal Policy Dilemma119 Questions

Exam 33: Jobs and Unemployment78 Questions

Exam 34: Inflation, Deflation, and Macro Policy175 Questions

Exam 35: International Financial Policy211 Questions

Exam 36: Macro Policy in a Global Setting134 Questions

Exam 37: Structural Stagnation and Globalization125 Questions

Exam 38: Macro Policy in Developing Countries142 Questions

Select questions type

A business produces eight items and sells them for $25 each. The total cost of producing the items is $190 for explicit costs and $200 for implicit costs. Accounting profit is:

(Multiple Choice)

4.9/5  (39)

(39)

The law of diminishing marginal productivity implies that the marginal product of a variable input:

(Multiple Choice)

4.8/5 (32)

Give the definition of marginal product and average product and explain why if the marginal product is smaller than the average product,the average product must be decreasing.

(Essay)

4.8/5 (44)

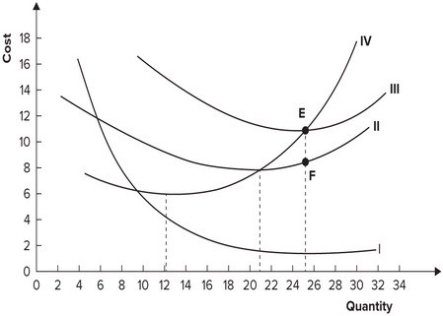

The following graph shows average fixed costs, average variable costs, average total costs, and marginal costs of production.  Average variable cost is minimized when output equals:

Average variable cost is minimized when output equals:

(Multiple Choice)

4.9/5 (43)

Refer to the table shown. If the average product is 6, the number of workers could equal:

Number of workers Total output 1 4 2 10 3 18 4 28 5 35 6 41 7 45 8 48 9 50 10 49

(Multiple Choice)

4.8/5 (31)

Which of the following is the best example of a long-run decision?

(Multiple Choice)

4.9/5 (33)

If marginal costs are rising, average total costs must be rising.

(True/False)

4.8/5 (40)

Mr. Woodard's cabinet shop is experiencing rapid growth in sales. As sales have increased, Mr. Woodard has found it necessary to hire more workers. However, he has observed that doubling the number of workers has less than doubled his output. What is the likely explanation?

(Multiple Choice)

4.8/5 (31)

Refer to the table shown. If the average product is 8, the number of workers is:

Number of workers Marginal product of workers 1 5 2 7 3 8 4 10 5 11 6 7 7 5 8 3 9 0 10 -1

(Multiple Choice)

4.9/5 (44)

How is accounting profit different from economic profit? How are they the same?

(Essay)

4.8/5 (40)

The following graph shows average fixed costs, average variable costs, average total costs, and marginal costs of production.  The average fixed cost curve is represented by which curve?

The average fixed cost curve is represented by which curve?

(Multiple Choice)

4.9/5 (32)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)