Exam 11: Production and Cost Analysis I

Exam 1: Economics and Economic Reasoning158 Questions

Exam 2: The Production Possibility Model, Trade, and Globalization133 Questions

Exam 3: Economic Institutions163 Questions

Exam 4: Supply and Demand182 Questions

Exam 5: Using Supply and Demand163 Questions

Exam 6: Describing Supply and Demand: Elasticities216 Questions

Exam 7: Taxation and Government Intervention201 Questions

Exam 8: Market Failure Versus Government Failure197 Questions

Exam 9: Comparative Advantage, Exchange Rates, and Globalization118 Questions

Exam 10: International Trade Policy99 Questions

Exam 11: Production and Cost Analysis I194 Questions

Exam 12: Production and Cost Analysis II152 Questions

Exam 13: Perfect Competition170 Questions

Exam 14: Monopoly and Monopolistic Competition274 Questions

Exam 15: Oligopoly and Antitrust Policy142 Questions

Exam 16: Real-World Competition and Technology108 Questions

Exam 17: Work and the Labor Market150 Questions

Exam 18: Who Gets What the Distribution of Income131 Questions

Exam 19: The Logic of Individual Choice: the Foundation of Supply and Demand170 Questions

Exam 20: Game Theory, Strategic Decision Making, and Behavioral Economics103 Questions

Exam 21: Thinking Like a Modern Economist97 Questions

Exam 22: Behavioral Economics and Modern Economic Policy126 Questions

Exam 23: Microeconomic Policy, Economic Reasoning, and Beyond134 Questions

Exam 24: Economic Growth, Business Cycles, and Unemployment124 Questions

Exam 25: Measuring and Describing the Aggregate Economy229 Questions

Exam 26: The Keynesian Short-Run Policy Model: Demand-Side Policies220 Questions

Exam 27: The Classical Long-Run Policy Model: Growth and Supply-Side Policies133 Questions

Exam 28: The Financial Sector and the Economy214 Questions

Exam 29: Monetary Policy243 Questions

Exam 30: Financial Crises, Panics, and Unconventional Monetary Policy109 Questions

Exam 31: Deficits and Debt: the Austerity Debate150 Questions

Exam 32: The Fiscal Policy Dilemma119 Questions

Exam 33: Jobs and Unemployment78 Questions

Exam 34: Inflation, Deflation, and Macro Policy175 Questions

Exam 35: International Financial Policy211 Questions

Exam 36: Macro Policy in a Global Setting134 Questions

Exam 37: Structural Stagnation and Globalization125 Questions

Exam 38: Macro Policy in Developing Countries142 Questions

Select questions type

The average total cost of producing electronic calculators in a factory is $20 at the current output level of 100 units per week. If fixed cost is $1,000 per week:

(Multiple Choice)

4.8/5  (30)

(30)

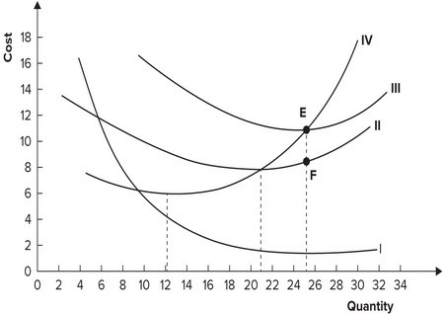

The following graph shows average fixed costs, average variable costs, average total costs, and marginal costs of production.  The distance EF represents:

The distance EF represents:

(Multiple Choice)

4.9/5 (38)

Accounting profit and economic profit differ because economic profit does not take into account opportunity cost.

(True/False)

4.7/5 (43)

Refer to the table shown. If the output of bicycles is 4 per week, the marginal cost of producing another bicycle per week is: Output (bicycles per week) Tatal cast (dallars) 1 100 2 200 3 310 4 440 5 580 6 730 7 900 8 1,200

(Multiple Choice)

4.8/5 (38)

Why do most firms operate at output levels where there is diminishing marginal productivity?

(Essay)

4.8/5 (32)

Refer to the table shown. At what level of employment is the marginal product of labor 7?

Number of workers Total output 1 4 2 10 3 18 4 28 5 35 6 41 7 45 8 48 9 50 10 49

(Multiple Choice)

4.9/5 (36)

What is the law of diminishing marginal productivity? Why does it apply only to the short-run?

(Essay)

4.7/5 (32)

How does accounting profit differ from economic profit? Explain why accounting profit is more useful for paying your taxes while economic profit is more useful for deciding whether you should continue to stay in business.Give an example of an implicit cost and an example of implicit revenue.

(Essay)

4.9/5 (39)

If fixed costs are $960, variable costs are $1,440, and output is 12, then average total cost equals:

(Multiple Choice)

4.7/5 (40)

Fixed costs remain the same regardless of the level of production.

(True/False)

4.7/5 (34)

Refer to the table shown. The marginal product of the sixth worker is:

Number of workers Total output 1 4 2 10 3 18 4 28 5 35 6 41 7 45 8 48 9 50 10 49

(Multiple Choice)

4.8/5 (40)

The only variable input used in producing bicycles in a small factory is labor. Currently four workers are employed; each works 40 hours per week and is paid $10 per hour. If fixed cost is $2,000 per week and total output is 10 bicycles per week, average cost is:

(Multiple Choice)

4.9/5 (33)

Which of the following cost curves is most often drawn with a U shape?

(Multiple Choice)

4.8/5 (37)

The minimum point of the average variable cost curve is reached at the output level where:

(Multiple Choice)

4.7/5 (38)

If the law of diminishing marginal productivity holds true, both average total cost and marginal cost must diminish as output increases.

(True/False)

4.9/5 (27)

The marginal cost curve intersects the average total cost curve when average variable costs are:

(Multiple Choice)

4.9/5 (39)

Which of the following is an example of a short-run decision?

(Multiple Choice)

4.8/5 (42)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)