Exam 4: Further Development and Analysis of the Classical Linear Regression Model

Exam 1: Introduction12 Questions

Exam 2: Mathematical and Statistical Foundations9 Questions

Exam 3: A Brief Overview of the Classical Linear Regression Model28 Questions

Exam 4: Further Development and Analysis of the Classical Linear Regression Model25 Questions

Exam 5: Classical Linear Regression Model Assumptions and Diagnostic Tests20 Questions

Exam 6: Univariate Time Series Modelling and Forecasting29 Questions

Exam 7: Multivariate Models30 Questions

Exam 8: Modelling Long-Run Relationships in Finance18 Questions

Exam 9: Modelling Volatility and Correlation22 Questions

Exam 10: Switching Models19 Questions

Exam 11: Panel Data and Limited Dependent Variable Models12 Questions

Select questions type

Two researchers have identical models, data, coefficients and standard error estimates. They test the same hypothesis using a two-sided alternative, but researcher 1 uses a 5% size of test while researcher 2 uses a 10% test. Which one of the following statements is correct?

(Multiple Choice)

4.8/5  (35)

(35)

Consider a bivariate regression model with coefficient standard errors calculated using the usual formulae. Which of the following statements is/are correct regarding the standard error estimator for the slope coefficient?

(I) It varies positively with the square root of the residual variance (s)

(ii) It varies positively with the spread of X about its mean value

(iii) It varies positively with the spread of X about zero

(iv) It varies positively with the sample size T

(Multiple Choice)

4.7/5 (46)

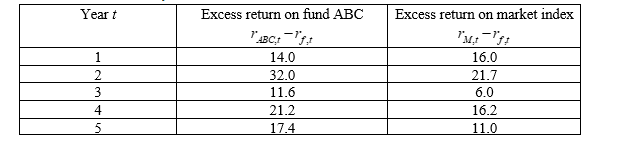

Suppose you have 5-year annual data on the excess returns on a fund manager’s portfolio (“fund ABC”) and the excess returns on a market index (where  is the return on fund ABC,

is the return on fund ABC,  is the risk-free rate and

is the risk-free rate and  is the return on the market index):

is the return on the market index):

-Given the data in question 6, what is the estimated beta (

-Given the data in question 6, what is the estimated beta (  ) of Fund ABC?

) of Fund ABC?

(Multiple Choice)

4.8/5 (42)

Which one of the following is NOT an assumption of the classical linear regression model?

(Multiple Choice)

4.7/5 (35)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)