Exam 9: Multifactor Models of Risk and Return

Exam 1: The Investment Setting78 Questions

Exam 2: The Asset Allocation Decision80 Questions

Exam 3: Selecting Investments in a Global Market80 Questions

Exam 4: Organization and Functioning of Securities Markets91 Questions

Exam 5: Security-Market Indexes84 Questions

Exam 6: Efficient Capital Markets90 Questions

Exam 7: An Introduction to Portfolio Management97 Questions

Exam 8: An Introduction to Asset Pricing Models119 Questions

Exam 9: Multifactor Models of Risk and Return59 Questions

Exam 10: Analysis of Financial Statements89 Questions

Exam 11: Introduction to Security Valuation86 Questions

Exam 12: Macroanalysis and Microvaluation of the Stock Market119 Questions

Exam 13: Industry Analysis90 Questions

Exam 14: Company Analysis and Stock Valuation133 Questions

Exam 15: Technical Analysis83 Questions

Exam 16: Equity Portfolio Management Strategies58 Questions

Exam 17: Bond Fundamentals89 Questions

Exam 18: The Analysis and Valuation of Bonds108 Questions

Exam 19: Bond Portfolio Management Strategies87 Questions

Exam 20: An Introduction to Derivative Markets and Securities108 Questions

Exam 21: Forward and Futures Contracts99 Questions

Exam 22: Option Contracts106 Questions

Exam 23: Swap Contracts, Convertible Securities, and Other Embedded Derivatives87 Questions

Exam 24: Professional Money Management, Alternative Assets, and Industry Ethics102 Questions

Exam 25: Evaluation of Portfolio Performance96 Questions

Select questions type

A study by Chen, Roll, and Ross in 1986 examined all of the following factors in applying the Arbitrage Pricing Theory (APT) except the

(Multiple Choice)

4.9/5  (36)

(36)

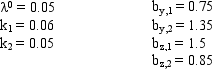

Exhibit 9.2

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Consider the three stocks, stock X, stock Y and stock Z, that have the following factor loadings (or factor betas).

The zero-beta return ( 0) = 3%, and the risk premia are 1 = 10%, 2 = 8%. Assume that all three stocks are currently priced at $50.

-Refer to Exhibit 9.2. Assume that you wish to create a portfolio with no net wealth invested and the portfolio that achieves this has 50% in stock X, -100% in stock Y, and 50% in stock Z. The net arbitrage profit is

The zero-beta return ( 0) = 3%, and the risk premia are 1 = 10%, 2 = 8%. Assume that all three stocks are currently priced at $50.

-Refer to Exhibit 9.2. Assume that you wish to create a portfolio with no net wealth invested and the portfolio that achieves this has 50% in stock X, -100% in stock Y, and 50% in stock Z. The net arbitrage profit is

(Multiple Choice)

4.8/5 (40)

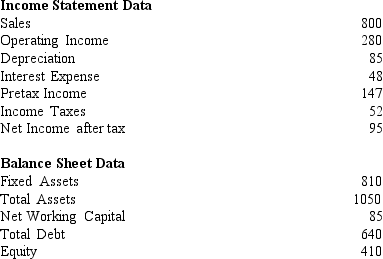

Exhibit 10.9

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

-Multifactor models of risk and return can be broadly grouped into models that use macroeconomic factors and models that use microeconomic factors.

-Multifactor models of risk and return can be broadly grouped into models that use macroeconomic factors and models that use microeconomic factors.

(True/False)

4.7/5 (36)

Exhibit 9.2

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Consider the three stocks, stock X, stock Y and stock Z, that have the following factor loadings (or factor betas).

The zero-beta return ( 0) = 3%, and the risk premia are 1 = 10%, 2 = 8%. Assume that all three stocks are currently priced at $50.

-Refer to Exhibit 9.2. The new prices now for stocks X, Y, and Z that will not allow for arbitrage profits are

(Multiple Choice)

4.7/5 (35)

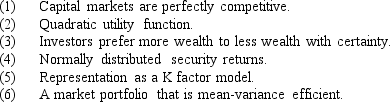

Exhibit 9.1

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Cho, Elton, and Gruber tested the APT by examining the number of factors in the return generating process and found that

-Cho, Elton, and Gruber tested the APT by examining the number of factors in the return generating process and found that

(Multiple Choice)

4.8/5 (35)

Under the following conditions, what are the expected returns for stocks Y and Z?

(Multiple Choice)

4.7/5 (42)

The table below provides factor risk sensitivities and factor risk premia for a three factor model for a particular asset where factor 1 is MP the growth rate in U.S. industrial production, factor 2 is UI the difference between actual and expected inflation, and factor 3 is UPR the unanticipated change in bond credit spread.  Calculate the expected excess return for the asset.

Calculate the expected excess return for the asset.

(Multiple Choice)

4.7/5 (37)

In a macro-economic based risk factor model the following factor would be one of many appropriate factors:

(Multiple Choice)

4.7/5 (34)

Exhibit 10.9

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

-The APT does not require a market portfolio.

(True/False)

4.7/5 (43)

Exhibit 10.9

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

-Two approaches to defining factors for multifactor models are to use macroeconomic variables or individual characteristics of the securities.

(True/False)

4.8/5 (38)

Exhibit 9.2

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Consider the three stocks, stock X, stock Y and stock Z, that have the following factor loadings (or factor betas).

The zero-beta return ( 0) = 3%, and the risk premia are 1 = 10%, 2 = 8%. Assume that all three stocks are currently priced at $50.

-Refer to Exhibit 9.2. Assume that you wish to create a portfolio with no net wealth invested. The portfolio that achieves this has 50% in stock X, -100% in stock Y, and 50% in stock Z. The weighted exposure to risk factor 2 for stocks X, Y, and Z are

(Multiple Choice)

4.8/5 (41)

Fama and French suggest a three factor model approach. Which of the following is not included in their approach?

(Multiple Choice)

4.9/5 (38)

Under the following conditions, what are the expected returns for stocks Y and Z?

(Multiple Choice)

4.8/5 (32)

Exhibit 9.1

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 9.1. In the list above which are assumptions of the Arbitrage Pricing Model?

(Multiple Choice)

4.8/5 (40)

Exhibit 10.9

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

-The APT assumes that capital markets are perfectly competitive.

(True/False)

4.8/5 (27)

Exhibit 10.9

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

-Arbitrage Pricing Theory (APT) specifies the exact number of risk factors and their identity

(True/False)

4.8/5 (42)

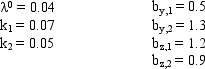

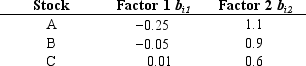

Exhibit 9.3

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Stocks A, B, and C have two risk factors with the following beta coefficients. The zero-beta return ( 0) = .025 and the risk premiums for the two factors are ( 1) = .12 and ( 0) = .10.

-Refer to Exhibit 9.3. Calculate the expected returns for stocks A, B, C. A B C

-Refer to Exhibit 9.3. Calculate the expected returns for stocks A, B, C. A B C

(Multiple Choice)

4.7/5 (28)

Exhibit 9.1

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Dhrymes, Friend, and Gultekin, in their study of the APT, found that

(Multiple Choice)

4.7/5 (36)

Exhibit 9.3

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Stocks A, B, and C have two risk factors with the following beta coefficients. The zero-beta return ( 0) = .025 and the risk premiums for the two factors are ( 1) = .12 and ( 0) = .10.

-Refer to Exhibit 9.3. Assume that stocks A, B, and C never pay dividends and stocks A, B, and C are currently trading at $10, $20, and $30, respectively. What is the expected price next year for each stock? A B C

(Multiple Choice)

4.9/5 (34)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)