Exam 8: An Introduction to Asset Pricing Models

Exam 1: The Investment Setting78 Questions

Exam 2: The Asset Allocation Decision80 Questions

Exam 3: Selecting Investments in a Global Market80 Questions

Exam 4: Organization and Functioning of Securities Markets91 Questions

Exam 5: Security-Market Indexes84 Questions

Exam 6: Efficient Capital Markets90 Questions

Exam 7: An Introduction to Portfolio Management97 Questions

Exam 8: An Introduction to Asset Pricing Models119 Questions

Exam 9: Multifactor Models of Risk and Return59 Questions

Exam 10: Analysis of Financial Statements89 Questions

Exam 11: Introduction to Security Valuation86 Questions

Exam 12: Macroanalysis and Microvaluation of the Stock Market119 Questions

Exam 13: Industry Analysis90 Questions

Exam 14: Company Analysis and Stock Valuation133 Questions

Exam 15: Technical Analysis83 Questions

Exam 16: Equity Portfolio Management Strategies58 Questions

Exam 17: Bond Fundamentals89 Questions

Exam 18: The Analysis and Valuation of Bonds108 Questions

Exam 19: Bond Portfolio Management Strategies87 Questions

Exam 20: An Introduction to Derivative Markets and Securities108 Questions

Exam 21: Forward and Futures Contracts99 Questions

Exam 22: Option Contracts106 Questions

Exam 23: Swap Contracts, Convertible Securities, and Other Embedded Derivatives87 Questions

Exam 24: Professional Money Management, Alternative Assets, and Industry Ethics102 Questions

Exam 25: Evaluation of Portfolio Performance96 Questions

Select questions type

Exhibit 8.5

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 8.5. Which of the three portfolios are most likely to be the market portfolio?

-Refer to Exhibit 8.5. Which of the three portfolios are most likely to be the market portfolio?

(Multiple Choice)

4.9/5  (38)

(38)

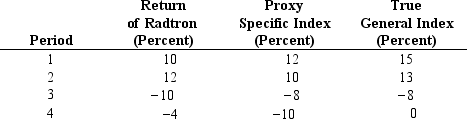

Exhibit 8.3

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 8.3. The covariance between Radtron and the true index is

-Refer to Exhibit 8.3. The covariance between Radtron and the true index is

(Multiple Choice)

4.8/5 (38)

Which of the following is not an assumption of the Capital Market Theory?

(Multiple Choice)

4.8/5 (36)

The correlation coefficient between the market return and a risk-free asset would

(Multiple Choice)

4.7/5 (31)

The expected return for a stock, calculated using the CAPM, is 25%. The risk free rate is 7.5% and the beta of the stock is 0.80. Calculate the implied return on the market.

(Multiple Choice)

4.9/5 (31)

Calculate the expected return for E Services which has a beta of 1.5 when the risk free rate is 0.05 and you expect the market return to be 0.11.

(Multiple Choice)

4.8/5 (41)

All of the following are assumptions of the Capital Asset Pricing Model (CAPM) except

(Multiple Choice)

4.9/5 (37)

The Capital Market Line (CML) can be thought of as the new Efficient Frontier.

(True/False)

4.9/5 (42)

Exhibit 8.4

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 8.4. If the expected return on the market is 11.5% and the risk-free rate of return is 4.5%, then what are the required rates of return for stocks X, Y, and Z based on the CAPM? X Y Z

-Refer to Exhibit 8.4. If the expected return on the market is 11.5% and the risk-free rate of return is 4.5%, then what are the required rates of return for stocks X, Y, and Z based on the CAPM? X Y Z

(Multiple Choice)

4.8/5 (34)

Calculate the expected return for C Inc. which has a beta of 0.8 when the risk free rate is 0.04 and you expect the market return to be 0.12.

(Multiple Choice)

4.9/5 (41)

Theoretically, the correlation coefficient between a completely diversified portfolio and the market portfolio should be

(Multiple Choice)

4.9/5 (47)

Exhibit 8.3

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 8.3. The covariance between Radtron and the proxy index is

(Multiple Choice)

4.8/5 (45)

The ____ the number of stocks in a portfolio and the ____ the time period the ____ the portfolio beta.

(Multiple Choice)

4.9/5 (34)

Consider a risky asset that has a standard deviation of returns of 15. Calculate the correlation between the risky asset and a risk free asset.

(Multiple Choice)

4.7/5 (44)

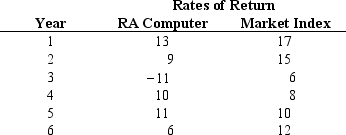

Exhibit 8.1

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 8.1. Compute the correlation coefficient between RA Computer and the Market Index.

-Refer to Exhibit 8.1. Compute the correlation coefficient between RA Computer and the Market Index.

(Multiple Choice)

4.9/5 (34)

A friend has some reliable information that the stock of Puddles Company is going to rise from $43.00 to $50.00 per share over the next year. You know that the annual return on the S&P 500 has been 11% and the 90-day T-bill rate has been yielding 5% per year over the past 10 years. If beta for Puddles is 1.5, will you purchase the stock?

(Multiple Choice)

4.7/5 (40)

The usefulness of CAPM theory is limited in practice due to benchmark error.

(True/False)

4.8/5 (33)

If the market portfolio is mean-variance efficient it has the lowest risk for a given level of return among the attainable set of portfolios.

(True/False)

4.8/5 (35)

The fact that tests have shown the CAPM intercept to be greater than the RFR is consistent with a(n)

(Multiple Choice)

4.8/5 (47)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)