Exam 8: An Introduction to Asset Pricing Models

Exam 1: The Investment Setting78 Questions

Exam 2: The Asset Allocation Decision80 Questions

Exam 3: Selecting Investments in a Global Market80 Questions

Exam 4: Organization and Functioning of Securities Markets91 Questions

Exam 5: Security-Market Indexes84 Questions

Exam 6: Efficient Capital Markets90 Questions

Exam 7: An Introduction to Portfolio Management97 Questions

Exam 8: An Introduction to Asset Pricing Models119 Questions

Exam 9: Multifactor Models of Risk and Return59 Questions

Exam 10: Analysis of Financial Statements89 Questions

Exam 11: Introduction to Security Valuation86 Questions

Exam 12: Macroanalysis and Microvaluation of the Stock Market119 Questions

Exam 13: Industry Analysis90 Questions

Exam 14: Company Analysis and Stock Valuation133 Questions

Exam 15: Technical Analysis83 Questions

Exam 16: Equity Portfolio Management Strategies58 Questions

Exam 17: Bond Fundamentals89 Questions

Exam 18: The Analysis and Valuation of Bonds108 Questions

Exam 19: Bond Portfolio Management Strategies87 Questions

Exam 20: An Introduction to Derivative Markets and Securities108 Questions

Exam 21: Forward and Futures Contracts99 Questions

Exam 22: Option Contracts106 Questions

Exam 23: Swap Contracts, Convertible Securities, and Other Embedded Derivatives87 Questions

Exam 24: Professional Money Management, Alternative Assets, and Industry Ethics102 Questions

Exam 25: Evaluation of Portfolio Performance96 Questions

Select questions type

An investor wishes to construct a portfolio consisting of a 70% allocation to a stock index and a 30% allocation to a risk free asset. The return on the risk-free asset is 4.5% and the expected return on the stock index is 12%. The standard deviation of returns on the stock index is 6%. Calculate the expected standard deviation of the portfolio.

(Multiple Choice)

4.9/5  (38)

(38)

Exhibit 8.6

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Jonathan Crowley is a portfolio manager for a large pension fund. Last year his portfolio had an actual return of 12.6% with a standard deviation of 13% and a beta of 1.3. The market risk premium for this period of time was 6% and the risk-free rate of return was 5%.

-Refer to Exhibit 8.6. How does Jonathan Crowley's portfolio compare to the market portfolio?

(Multiple Choice)

4.8/5 (32)

The error caused by not using the true market portfolio has become known as the

(Multiple Choice)

4.8/5 (40)

Exhibit 8.4

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 8.4. Which of the following statements is correct?

-Refer to Exhibit 8.4. Which of the following statements is correct?

(Multiple Choice)

4.8/5 (44)

A portfolio manager uses two different proxies for the market portfolio, the S&P 500 index and the MSCI World index. Differences in the manager's portfolio performance resulting from the different market portfolios is referred to as

(Multiple Choice)

4.9/5 (36)

The only way to estimate a beta for a security is to calculate the covariance of the security with the market.

(True/False)

4.8/5 (37)

The variance of returns for a risky asset is 25%. The variance of the error term, Var(e), is 8%. What portion of the total risk of the asset, as measured by variance, is systematic?

(Multiple Choice)

4.9/5 (39)

Calculate the expected return for F Inc. which has a beta of 1.3 when the risk free rate is 0.06 and you expect the market return to be 0.125.

(Multiple Choice)

4.9/5 (35)

The capital market line (CML) uses ____ as a risk measurement, whereas the capital asset pricing model (CAPM) uses ____.

(Multiple Choice)

4.8/5 (38)

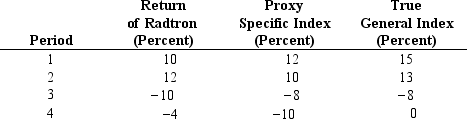

Exhibit 8.3

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 8.3. The average return for Radtron is

-Refer to Exhibit 8.3. The average return for Radtron is

(Multiple Choice)

4.8/5 (36)

Exhibit 8.6

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Jonathan Crowley is a portfolio manager for a large pension fund. Last year his portfolio had an actual return of 12.6% with a standard deviation of 13% and a beta of 1.3. The market risk premium for this period of time was 6% and the risk-free rate of return was 5%.

-Refer to Exhibit 8.6. Based on the Capital Asset Pricing Model (CAPM), what is the required rate of return for this portfolio?

(Multiple Choice)

4.9/5 (29)

Which of the following variables were found to be important in explaining return based upon a study of Fama and French (covering the period 1963 to 1990)?

(Multiple Choice)

4.7/5 (42)

Consider an asset that has a beta of 1.5. The return on the risk-free asset is 6.5% and the expected return on the stock index is 15%. The estimated return on the asset is 20%. Calculate the alpha for the asset.

(Multiple Choice)

4.9/5 (33)

Utilizing the security market line an investor owning a stock with a beta of -2 would expect the stock's return to ____ in a market that was expected to decline 15 percent.

(Multiple Choice)

4.9/5 (36)

Assume that as a portfolio manager the beta of your portfolio is 1.15 and that your performance is exactly on target with the SML data under condition 1. If the true SML data is given by condition 2, how much does your performance differ from the true SML?

(Multiple Choice)

4.9/5 (32)

When identifying undervalued and overvalued assets, which of the following statements is false?

(Multiple Choice)

4.8/5 (39)

An investor constructs a portfolio with a 75% allocation to a stock index and a 25% allocation to a risk free asset. The expected returns on the risk-free asset and the stock index are 3% and 10%, respectively. The standard deviation of returns on the stock index is 14%. Calculate the expected standard deviation of the portfolio.

(Multiple Choice)

4.9/5 (42)

The existence of transaction costs indicates that at some point the additional cost of diversification relative to its benefit would be excessive for most investors.

(True/False)

4.8/5 (37)

Calculate the expected return for A Industries which has a beta of 1.75 when the risk free rate is 0.03 and you expect the market return to be 0.11.

(Multiple Choice)

4.9/5 (31)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)