Exam 16: Alternative Exit and Restructuring Strategies

Exam 1: Introduction to Mergers, Acquisitions, and Other Restructuring Activities139 Questions

Exam 2: The Regulatory Environment129 Questions

Exam 3: The Corporate Takeover Market:152 Questions

Exam 4: Planning: Developing Business and Acquisition Plans: Phases 1 and 2 of the Acquisition Process137 Questions

Exam 5: Implementation: Search Through Closing: Phases 310 of the Acquisition Process131 Questions

Exam 6: Postclosing Integration: Mergers, Acquisitions, and Business Alliances138 Questions

Exam 7: Merger and Acquisition Cash Flow Valuation Basics108 Questions

Exam 8: Relative, Asset-Oriented, and Real Option109 Questions

Exam 9: Financial Modeling Basics:97 Questions

Exam 10: Analysis and Valuation127 Questions

Exam 11: Structuring the Deal:138 Questions

Exam 12: Structuring the Deal:125 Questions

Exam 13: Financing the Deal149 Questions

Exam 14: Applying Financial Modeling116 Questions

Exam 15: Business Alliances: Joint Ventures, Partnerships, Strategic Alliances, and Licensing138 Questions

Exam 16: Alternative Exit and Restructuring Strategies152 Questions

Exam 17: Alternative Exit and Restructuring Strategies:118 Questions

Exam 18: Cross-Border Mergers and Acquisitions:120 Questions

Select questions type

Hewlett Packard (HP) announced the spin-off of its Agilent Technologies unit to focus on its main business of computers and printers, where sales have been lagging behind such competitors as Sun Microsystems. Agilent makes test, measurement, and monitoring instruments; semiconductors; and optical components. It also supplies patient-monitoring and ultrasound-imaging equipment to the health care industry. HP will retain an 85% stake in the company. The cash raised through the 15% equity carve-out will be paid to HP as a dividend from the subsidiary to the parent. Hewlett Packard will provide Agilent with $983 million in start-up funding. HP retained a controlling interest until mid-2000, when it spun-off the rest of its shares in Agilent to HP shareholders as a tax-free transaction.

-Discuss the conditions under which this spin-off would constitute a tax-free transaction.

(Essay)

4.9/5  (37)

(37)

Antitrust regulatory agencies may make their approval of a merger contingent on the willingness of the merger partners to divest certain businesses.

(True/False)

4.9/5 (38)

Speculate as to why Northrop Grumman used a spin-off rather than a divestiture, split-off or split up to separate Huntington Ingalls from the rest of its operations? What were the advantages of the spin-off over the other restructuring strategies.

(Essay)

4.8/5 (34)

Gillette Announces Divestiture Plans

With 1998 sales of $10.1 billion, Gillette is the world leader in the production of razor blades, razors, and shaving cream. Gillette also has a leading position in the production of pens and other writing instruments. Gillette's consolidated operating performance during 1999 depended on its core razor blade and razor, Duracell battery, and oral care businesses. Reflecting disappointment in the performance of certain operating units, Gillette's CEO, Michael Hawley, announced in October 1999 his intention to divest poorly performing businesses unless he could be convinced by early 2000 that they could be turned around. The businesses under consideration at that time comprised about 15% of the company's $10 billion in annual sales. Hawley saw the new focus of the company to be in razor blades, batteries, and oral care. To achieve this new focus, Hawley intended to prune the firm's product portfolio. The most likely targets for divestiture at the time included pens (i.e., PaperMate, Parker, and Waterman), with the prospects for operating performance for these units considered dismal. Other units under consideration for divestiture included Braun and toiletries. With respect to these businesses, Hawley apparently intended to be selective. At Braun, where overall operating profits plunged 43% in the first three quarters of 1999, Hawley has announced that Gillette will keep electric shavers and electric toothbrushes. However, the household and personal care appliance units are likely divestiture candidates. The timing of these sales may be poor. A decision to sell Braun at this time would compete against Black & Decker's recently announced decision to sell its appliance business.

Although Gillette would be smaller, the firm believes that its margins will improve and that its earnings growth will be more rapid. Moreover, divesting such problem businesses as pens and appliances would let management focus on the units whose prospects are the brightest. These are businesses that Gillette's previous management was simply not willing to sell because of their perceived high potential.

-Which of the major restructuring motives discussed in this chapter seem to be a work in this business case? Explain your answer.

(Essay)

4.9/5 (31)

Hewlett Packard (HP) announced the spin-off of its Agilent Technologies unit to focus on its main business of computers and printers. Hewlett Packard provided Agilent with $983 million in start-up funding. HP retained a controlling interest until mid-2000, when it spun-off the rest of its shares in Agilent to HP shareholders as a tax-free transaction. Discuss the reasons why HP may have chosen a staged transaction rather than an outright divestiture of the business.

(Essay)

4.8/5 (30)

The Anatomy of a Reverse Morris Trust Transaction:

The Pringles Potato Chip Saga

Greater shareholder value may be created by exiting rather than operating a business.

Deal structures can impose significant limitations on a firm’s future strategies and tactics.

_____________________________________________________________________________________________

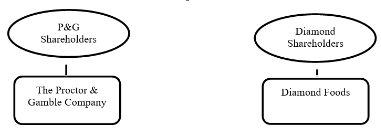

Following a rigorous portfolio review and an informal expression of interest in the Pringles brand by Diamond Foods (Diamond) in late 2009, Proctor & Gamble (P&G), the world’s leading manufacturer of household products, believed that Pringles could be worth more to its shareholders if divested than if retained. Pringles is the iconic potato chip brand, with sales in 140 countries and operations in the United States, Europe, and Asia.

Diamond’s executive management had long viewed the Pringles’ brand as an attractive fit for their strategy of building, acquiring, and energizing brands. The acquisition of Pringles would triple the size of the firm’s snack business and provide greater merchandising influence in the way in which its products are distributed. The merger would also give Diamond a substantial presence in Asia, Latin America, and Central Europe. The increased geographic diversity means the firm would derive almost one-half of its revenue from international sales.

After extended negotiations, Diamond and P&G announced on April 15, 2011, their intent to merge P&G’s Pringles subsidiary into Diamond in a transaction valued at $2.35 billion. The purchase price consisted of $1.5 billion in Diamond common stock, valued at $51.47 per share, and Diamond’s assumption of $850 million in Pringles outstanding debt. The way in which the deal was structured enabled P&G shareholders to defer any gains they realize from the transaction and resulted in a one-time after-tax earnings increase for P&G of $1.5 billion due to the firm’s low tax basis in Pringles.

The offer to exchange Pringle shares for P&G shares reduced the number of outstanding P&G common shares, partially offsetting the impact on P&G’s earnings per share of the loss of Pringles earnings. Diamond agreed to issue one share of its common stock for each Pringles common share. The 29.1 million common shares issued by Diamond resulted in P&G shareholders’ participating in the exchange offer, owning a 57% stake in the combined firms, with Diamond’s shareholders owning the remainder.

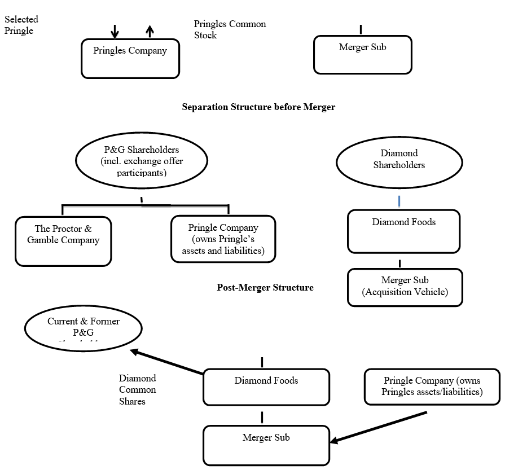

The deal was structured as a reverse Morris Trust acquisition, which combines a divisive reorganization (e.g., a spin-off or a split-off) with an acquisitive reorganization (e.g., a statutory merger) to allow a tax-free transfer of a subsidiary under U.S. law. The use of a divisive reorganization results in the creation of a public company that is subsequently merged into a shell subsidiary (i.e., a privately owned company) of another firm, with the shell surviving.

The structure of the deal involved four discrete steps, outlined in separation and transaction agreements signed by P&G and Diamond. These steps included the following: (1) the creation by P&G of a wholly owned subsidiary containing Pringles’ assets and liabilities; (2) the recapitalization of the wholly owned Pringles subsidiary; (3) the separation of the wholly owned subsidiary through a split-off exchange offer; and (4) a merger with a wholly owned subsidiary of Diamond Foods. The separation agreement covered the first three steps, with the final step detailed in the transaction agreement.

Under the separation agreement, P&G contributed certain Pringles assets and liabilities to the Pringles Company, a newly formed wholly owned subsidiary of P&G. After P&G and Diamond reached a negotiated value for the Pringles Company equity of $1.5 billion, or $51.47 per share, the Pringles Company was subsequently recapitalized by issuing to P&G 29.1 million shares of Pringles Company stock. To complete the separation of Pringles from the parent firm, P&G distributed on the closing date Pringles shares to P&G shareholders participating in a share-exchange offer in which they agreed to exchange their P&G shares for Pringles shares.

In addition, the Pringles Company borrowed $850 million and used the proceeds to pay P&G a cash dividend and to acquire certain Pringles business assets held by P&G affiliates. Since P&G is the sole owner of the Pringles Company, the dividend is tax free to P&G because it is an intracompany transfer. If the exchange offer had not been fully subscribed, P&G would have distributed through a tax-free spin-off the remaining shares as a dividend to P&G shareholders.

The transaction agreement outlined the terms and conditions pertinent to completion of the merger with Diamond Foods. Immediately after the completion of the distribution, the Pringles Company merged with Merger Sub, a wholly owned shell subsidiary of Diamond, with Merger Sub’s continuing as the surviving company. The shares of Pringles Company common stock distributed in connection with the split-off exchange offer automatically converted into the right to receive shares of Diamond common stock on a one-for-one basis. After the merger, Diamond, through Merger Sub, owned and operated Pringles

Prior to the merger, Diamond already had formidable antitakeover defenses in place as part of its charter documents, including a classified board of directors, a prohibition against stockholders’ taking action by written consent (i.e., consent solicitation), and a requirement that stockholders give advance notice before raising matters at a stockholders’ meeting. Following the merger, Diamond adopted a shareholder-rights plan. The plan entitled the holder of such rights to purchase 1/100 of a share of Diamond’s Series A Junior Participating Preferred Stock if a person or group acquires 15% or more of Diamond’s outstanding common stock. Holders of this preferred stock (other than the person or group triggering their exercise) would be able to purchase Diamond common shares (flip-in poison pill) or those of any company into which Diamond is merged (flip-over poison pill) at a price of $60 per share. Such rights would expire in March 2015 unless extended by Diamond’s board of directors.

-The merger of Pringles and Diamond Foods could have been achieved as a result of a P&G spin-off of Pringles. Explain the details of how this might happen.

Prior to the merger, Diamond already had formidable antitakeover defenses in place as part of its charter documents, including a classified board of directors, a prohibition against stockholders’ taking action by written consent (i.e., consent solicitation), and a requirement that stockholders give advance notice before raising matters at a stockholders’ meeting. Following the merger, Diamond adopted a shareholder-rights plan. The plan entitled the holder of such rights to purchase 1/100 of a share of Diamond’s Series A Junior Participating Preferred Stock if a person or group acquires 15% or more of Diamond’s outstanding common stock. Holders of this preferred stock (other than the person or group triggering their exercise) would be able to purchase Diamond common shares (flip-in poison pill) or those of any company into which Diamond is merged (flip-over poison pill) at a price of $60 per share. Such rights would expire in March 2015 unless extended by Diamond’s board of directors.

-The merger of Pringles and Diamond Foods could have been achieved as a result of a P&G spin-off of Pringles. Explain the details of how this might happen.

(Essay)

4.9/5 (41)

A spin-off may create shareholder wealth for all of the following reasons except for

(Multiple Choice)

4.9/5 (27)

Although the parent retains control, the shareholder base of the subsidiary that has undergone an equity carve-out is unlikely to be different than that of the parent as a result of the public sale of equity.

(True/False)

4.8/5 (36)

The Anatomy of a Reverse Morris Trust Transaction:

The Pringles Potato Chip Saga

Greater shareholder value may be created by exiting rather than operating a business.

Deal structures can impose significant limitations on a firm’s future strategies and tactics.

_____________________________________________________________________________________________

Following a rigorous portfolio review and an informal expression of interest in the Pringles brand by Diamond Foods (Diamond) in late 2009, Proctor & Gamble (P&G), the world’s leading manufacturer of household products, believed that Pringles could be worth more to its shareholders if divested than if retained. Pringles is the iconic potato chip brand, with sales in 140 countries and operations in the United States, Europe, and Asia.

Diamond’s executive management had long viewed the Pringles’ brand as an attractive fit for their strategy of building, acquiring, and energizing brands. The acquisition of Pringles would triple the size of the firm’s snack business and provide greater merchandising influence in the way in which its products are distributed. The merger would also give Diamond a substantial presence in Asia, Latin America, and Central Europe. The increased geographic diversity means the firm would derive almost one-half of its revenue from international sales.

After extended negotiations, Diamond and P&G announced on April 15, 2011, their intent to merge P&G’s Pringles subsidiary into Diamond in a transaction valued at $2.35 billion. The purchase price consisted of $1.5 billion in Diamond common stock, valued at $51.47 per share, and Diamond’s assumption of $850 million in Pringles outstanding debt. The way in which the deal was structured enabled P&G shareholders to defer any gains they realize from the transaction and resulted in a one-time after-tax earnings increase for P&G of $1.5 billion due to the firm’s low tax basis in Pringles.

The offer to exchange Pringle shares for P&G shares reduced the number of outstanding P&G common shares, partially offsetting the impact on P&G’s earnings per share of the loss of Pringles earnings. Diamond agreed to issue one share of its common stock for each Pringles common share. The 29.1 million common shares issued by Diamond resulted in P&G shareholders’ participating in the exchange offer, owning a 57% stake in the combined firms, with Diamond’s shareholders owning the remainder.

The deal was structured as a reverse Morris Trust acquisition, which combines a divisive reorganization (e.g., a spin-off or a split-off) with an acquisitive reorganization (e.g., a statutory merger) to allow a tax-free transfer of a subsidiary under U.S. law. The use of a divisive reorganization results in the creation of a public company that is subsequently merged into a shell subsidiary (i.e., a privately owned company) of another firm, with the shell surviving.

The structure of the deal involved four discrete steps, outlined in separation and transaction agreements signed by P&G and Diamond. These steps included the following: (1) the creation by P&G of a wholly owned subsidiary containing Pringles’ assets and liabilities; (2) the recapitalization of the wholly owned Pringles subsidiary; (3) the separation of the wholly owned subsidiary through a split-off exchange offer; and (4) a merger with a wholly owned subsidiary of Diamond Foods. The separation agreement covered the first three steps, with the final step detailed in the transaction agreement.

Under the separation agreement, P&G contributed certain Pringles assets and liabilities to the Pringles Company, a newly formed wholly owned subsidiary of P&G. After P&G and Diamond reached a negotiated value for the Pringles Company equity of $1.5 billion, or $51.47 per share, the Pringles Company was subsequently recapitalized by issuing to P&G 29.1 million shares of Pringles Company stock. To complete the separation of Pringles from the parent firm, P&G distributed on the closing date Pringles shares to P&G shareholders participating in a share-exchange offer in which they agreed to exchange their P&G shares for Pringles shares.

In addition, the Pringles Company borrowed $850 million and used the proceeds to pay P&G a cash dividend and to acquire certain Pringles business assets held by P&G affiliates. Since P&G is the sole owner of the Pringles Company, the dividend is tax free to P&G because it is an intracompany transfer. If the exchange offer had not been fully subscribed, P&G would have distributed through a tax-free spin-off the remaining shares as a dividend to P&G shareholders.

The transaction agreement outlined the terms and conditions pertinent to completion of the merger with Diamond Foods. Immediately after the completion of the distribution, the Pringles Company merged with Merger Sub, a wholly owned shell subsidiary of Diamond, with Merger Sub’s continuing as the surviving company. The shares of Pringles Company common stock distributed in connection with the split-off exchange offer automatically converted into the right to receive shares of Diamond common stock on a one-for-one basis. After the merger, Diamond, through Merger Sub, owned and operated Pringles

Prior to the merger, Diamond already had formidable antitakeover defenses in place as part of its charter documents, including a classified board of directors, a prohibition against stockholders’ taking action by written consent (i.e., consent solicitation), and a requirement that stockholders give advance notice before raising matters at a stockholders’ meeting. Following the merger, Diamond adopted a shareholder-rights plan. The plan entitled the holder of such rights to purchase 1/100 of a share of Diamond’s Series A Junior Participating Preferred Stock if a person or group acquires 15% or more of Diamond’s outstanding common stock. Holders of this preferred stock (other than the person or group triggering their exercise) would be able to purchase Diamond common shares (flip-in poison pill) or those of any company into which Diamond is merged (flip-over poison pill) at a price of $60 per share. Such rights would expire in March 2015 unless extended by Diamond’s board of directors.

-Why did the addition of the shareholder rights plan by Diamond Foods following the merger with Pringles make sense given the type of deal structure used?

(Essay)

4.9/5 (33)

USX Bows to Shareholder Pressure to Split Up the Company

As one of the first firms to issue tracking stocks in the mid-1980s, USX relented to ongoing shareholder pressure to divide the firm into two pieces. After experiencing a sharp "boom/bust" cycle throughout the 1970s, U.S. Steel had acquired Marathon Oil, a profitable oil and gas company, in 1982 in what was at the time the second largest merger in U.S. history. Marathon had shown steady growth in sales and earnings throughout the 1970s. USX Corp. was formed in 1986 as the holding company for both U.S. Steel and Marathon Oil. In 1991, USX issued its tracking stocks to create "pure plays" in its primary businesses-steel and oil-and to utilize USX's steel losses, which could be used to reduce Marathon's taxable income. Marathon shareholders have long complained that Marathon's stock was selling at a discount to its peers because of its association with USX. The campaign to split Marathon from U.S. Steel began in earnest in early 2000.

On April 25, 2001, USX announced its intention to split U.S. Steel and Marathon Oil into two separately traded companies. The breakup gives holders of Marathon Oil stock an opportunity to participate in the ongoing consolidation within the global oil and gas industry. Holders of USX-U.S. Steel Group common stock (target stock) would become holders of newly formed Pittsburgh-based United States Steel Corporation, a return to the original name of the firm formed in 1901. Under the reorganization plan, U.S. Steel and Marathon would retain the same assets and liabilities already associated with each business. However, Marathon will assume $900 million in debt from U.S. Steel, leaving the steelmaker with $1.3 billion of debt. This assumption of debt by Marathon is an attempt to make U.S. Steel, which continued to lose money until 2004, able to stand on its own financially.

The investor community expressed mixed reactions, believing that Marathon would be likely to benefit from a possible takeover attempt, whereas U.S. Steel would not fare as well. Despite the initial investor pessimism, investors in both Marathon and U.S. Steel saw their shares appreciate significantly in the years immediately following the breakup.:

-What other alternatives could USX have pursued to increase shareholder value? Why do you believe they pursued the breakup strategy rather than some of the alternatives?

(Essay)

4.8/5 (36)

Investors often evaluate a firm’s performance in terms of how well it does as compared to its peers.

Activist investors can force an underperforming firm to change its strategy radically.

The Kraft decision to split its businesses is yet another example of the recent trend by highly diversified businesses to increase their product focus.

_____________________________________________________________________________________________________

Following a successful career as CEO of PepsiCo’s Frito-Lay, Irene Rosenfeld became the CEO of Kraft Foods in 2006. As the world’s second-largest packaged foods manufacturer, behind Nestlé, Kraft had stumbled in its efforts to increase its global reach by growing in emerging markets. Its brands tended to be old, and the firm was having difficulty developing new, trendy products. Rosenfeld was tasked by its board of directors with turning the firm around. She reasoned that it would take a complete overhaul of Kraft, including organization, culture, operations, marketing, branding, and the product portfolio, to transform the firm.

In 2010, the firm made what at the time was viewed by top management as its most transformational move by acquiring British confectionery company Cadbury for $19 billion. While the firm became the world’s largest snack company with the completion of the transaction, it was still entrenched in its traditional business, groceries. The company now owned two very different product portfolios.

Between January 2010 and mid-2011, Kraft’s earnings steadily improved, powered by stronger sales. Kraft shares rose almost 25%, more than twice the increase in the S&P 500 stock index. However, it continued to trade throughout this period at a lower price-to-earnings multiple than such competitors as Nestlé and Groupe Danone. Some investors were concerned that Kraft was not realizing the promised synergies from the Cadbury deal. Activist investors (Nelson Peltz’s Trian Fund and Bill Ackman’s Pershing Square Capital Management) had discussions with Kraft’s management about splitting the firm. This plan had the support of Warren Buffett, whose conglomerate, Berkshire Hathaway, was Kraft’s largest investor at that time, with a 6% ownership interest.

To avert a proxy fight, Kraft’s board and management announced on August 4, 2011, its intention to restructure the firm radically by separating it into two distinct businesses. Coming just 18 months after the Cadbury deal, investors were initially stunned by the announcement but appeared to avidly support the proposal avidly by driving up the firm’s share price by the end of the day. The proposal entailed separating its faster-growing global snack food business from its slower-growing, more United States–centered grocery business. The separation was completed through a tax-free spin-off to Kraft Food shareholders of the grocery business on October 1, 2012. The global snack food business will be named Mondelez International, while the North American grocery business will retain the Kraft name.

Management justified the proposed split-up of the firm as a means of increasing focus, providing greater opportunities, and giving investors a choice between the faster-growing snack business and the slower-growing but more predictable grocery operation. Management also argued that the Cadbury acquisition gave the snack business scale to compete against such competitors as Nestlé and PepsiCo.

-There is often a natural tension between so-called activist investors interested in short-term profits and a firm's management interested in pursuing a longer-term vision. When is this tension helpful to shareholders and when does it destroy shareholder value?

(Essay)

4.9/5 (38)

Equity carve-outs have some of the characteristics of both divestitures and spin-offs.

(True/False)

4.9/5 (28)

Anatomy of a Spin-Off

On October 18, 2006, Verizon Communication's board of directors declared a dividend to the firm's shareholders consisting of shares in a company comprising the firm's domestic print and Internet yellow pages directories publishing operations (Idearc Inc.). The dividend consisted of 1 share of Idearc stock for every 20 shares of Verizon common stock. Idearc shares were valued at $34.47 per share. On the dividend payment date, Verizon shares were valued at $36.42 per share. The 1-to-20 ratio constituted a 4.73% yield—that is, $34.47/ ($36.42 × 20)—approximately equal to Verizon's then current cash dividend yield.

Because of the spin-off, Verizon would contribute to Idearc all its ownership interest in Idearc Information Services and other assets, liabilities, businesses, and employees currently employed in these operations. In exchange for the contribution, Idearc would issue to Verizon shares of Idearc common stock to be distributed to Verizon shareholders. In addition, Idearc would issue senior unsecured notes to Verizon in an amount approximately equal to the $9 billion in debt that Verizon incurred in financing Idearc's operations historically. Idearc would also transfer $2.5 billion in excess cash to Verizon. Verizon believed it owned such cash balances, since they were generated while Idearc was part of the parent.

Verizon announced that the spin-off would enable the parent and Idearc to focus on their core businesses, which may facilitate expansion and growth of each firm. The spin-off would also allow each company to determine its own capital structure, enable Idearc to pursue an acquisition strategy using its own stock, and permit Idearc to enhance its equity-based compensation programs offered to its employees. Because of the spin-off, Idearc would become an independent public company. Moreover, no vote of Verizon shareholders was required to approve the spin-off, since it constitutes the payment of a dividend permissible by the board of directors according to the bylaws of the firm. Finally, Verizon shareholders have no appraisal rights in connection with the spin-off.

In late 2009, Idearc entered Chapter 11 bankruptcy because it was unable to meet its outstanding debt obligations. In September 2010, a trustee for Idearc’s creditors filed a lawsuit against Verizon, alleging that the firm breached its fiduciary responsibility by knowingly spinning off a business that was not financially viable. The lawsuit further contends that Verizon benefitted from the spin-off at the expense of the creditors by transferring $9 billion in debt from its books to Idearc and receiving $2.5 billion in cash from Idearc.

-To what extent do you believe that Verizon's activities could be viewed as fraudulent? Explain your answer.

(Essay)

4.9/5 (38)

How might the form of payment affect the abnormal return to sellers and buyers?

(Essay)

4.7/5 (39)

Which of the following is generally not considered a common motive for exiting businesses?

(Multiple Choice)

4.9/5 (33)

Hughes Corporation's Dramatic Transformation

In one of the most dramatic redirections of corporate strategy in U.S. history, Hughes Corporation transformed itself from a defense industry behemoth into the world's largest digital information and communications company. Once California's largest manufacturing employer, Hughes Corporation built spacecraft, the world's first working laser, communications satellites, radar systems, and military weapons systems. However, by the late 1990s, the firm had undergone substantial gut-wrenching change to reposition the firm in what was viewed as a more attractive growth opportunity. This transformation culminated in the firm being acquired in 2004 by News Corp., a global media empire.

To accomplish this transformation, Hughes divested its communications satellite businesses and its auto electronics operation. The corporate overhaul created a firm focused on direct-to-home satellite broadcasting with its DirecTV service offering. DirecTV's introduction to nearly 12 million U.S. homes was a technology made possible by U.S. military spending during the early 1980s. Although military spending had fueled much of Hughes' growth during the decade of the 1980s, it was becoming increasingly clear by 1988 that the level of defense spending of the Reagan years was coming to a close with the winding down of the cold war.

For the next several years, Hughes attempted to find profitable niches in the rapidly consolidating U.S. defense contracting industry. Hughes acquired General Dynamics' missile business and made 15 smaller defense-related acquisitions. Eventually, Hughes' parent firm, General Motors, lost enthusiasm for additional investment in defense-related businesses. GM decided that, if Hughes could not participate in the shrinking defense industry, there was no reason to retain any interests in the industry at all. In November 1995, Hughes initiated discussions with Raytheon, and two years later, it sold its aerospace and defense business to Raytheon for $9.8 billion. The firm also merged its Delco product line with GM's Delphi automotive systems. What remained was the firm's telecommunications division. Hughes had transformed itself from a $16 billion defense contractor to a svelte $4 billion telecommunications business.

Hughes' telecommunications unit was its smallest operation but, with DirecTV, its fastest growing. The transformation was to exact a huge cultural toll on Hughes' employees, most of whom had spent their careers dealing with the U.S. Department of Defense. Hughes moved to hire people aggressively from the cable and broadcast businesses. By the late 1990s, former Hughes' employees constituted only 15-20 percent of DirecTV's total employees.

Restructuring continued through the end of the 1990s. In 2000, Hughes sold its satellite manufacturing operations to Boeing for $3.75 billion. This eliminated the last component of the old Hughes and cut its workforce in half. In December 2000, Hughes paid about $180 million for Telocity, a firm that provides digital subscriber line service through phone lines. This acquisition allowed Hughes to provide high-speed Internet connections through its existing satellite service, mainly in more remote rural areas, as well as phone lines targeted at city dwellers. Hughes now could market the same combination of high-speed Internet services and video offered by cable providers, Hughes' primary competitor.

In need of cash, GM put Hughes up for sale in late 2000, expressing confidence that there would be a flood of lucrative offers. However, the faltering economy and stock market resulted in GM receiving only one serious bid, from media tycoon Rupert Murdoch of News Corp. in February 2001. But, internal discord within Hughes and GM over the possible buyer of Hughes Electronics caused GM to backpedal and seek alternative bidders. In late October 2001, GM agreed to sell its Hughes Electronics subsidiary and its DirecTV home satellite network to EchoStar Communication for $25.8 billion. However, regulators concerned about the antitrust implications of the deal disallowed this transaction. In early 2004, News Corp., General Motors, and Hughes reached a definitive agreement in which News Corp acquired GM's 19.9 percent stake in Hughes and an additional 14.1 percent of Hughes from public shareholders and GM's pension and other benefit plans. News Corp. paid about $14 per share, making the deal worth about $6.6 billion for 34.1 percent of Hughes. The implied value of 100 percent of Hughes was, at that time, $19.4 billion, about three fourths of EchoStar's valuation three years earlier.

-How did changes in Hughes' external environment contribute to its dramatic 20-year restructuring effort? Cite specific influences in answering this question. (Hint: Consider some of the motivations discussed in this chapter for engaging in restructuring activities.). Cite examples of how Hughes took advantage of their core competencies in pursuing other alternatives?

(Essay)

4.8/5 (34)

The Anatomy of a Reverse Morris Trust Transaction:

The Pringles Potato Chip Saga

Greater shareholder value may be created by exiting rather than operating a business.

Deal structures can impose significant limitations on a firm’s future strategies and tactics.

_____________________________________________________________________________________________

Following a rigorous portfolio review and an informal expression of interest in the Pringles brand by Diamond Foods (Diamond) in late 2009, Proctor & Gamble (P&G), the world’s leading manufacturer of household products, believed that Pringles could be worth more to its shareholders if divested than if retained. Pringles is the iconic potato chip brand, with sales in 140 countries and operations in the United States, Europe, and Asia.

Diamond’s executive management had long viewed the Pringles’ brand as an attractive fit for their strategy of building, acquiring, and energizing brands. The acquisition of Pringles would triple the size of the firm’s snack business and provide greater merchandising influence in the way in which its products are distributed. The merger would also give Diamond a substantial presence in Asia, Latin America, and Central Europe. The increased geographic diversity means the firm would derive almost one-half of its revenue from international sales.

After extended negotiations, Diamond and P&G announced on April 15, 2011, their intent to merge P&G’s Pringles subsidiary into Diamond in a transaction valued at $2.35 billion. The purchase price consisted of $1.5 billion in Diamond common stock, valued at $51.47 per share, and Diamond’s assumption of $850 million in Pringles outstanding debt. The way in which the deal was structured enabled P&G shareholders to defer any gains they realize from the transaction and resulted in a one-time after-tax earnings increase for P&G of $1.5 billion due to the firm’s low tax basis in Pringles.

The offer to exchange Pringle shares for P&G shares reduced the number of outstanding P&G common shares, partially offsetting the impact on P&G’s earnings per share of the loss of Pringles earnings. Diamond agreed to issue one share of its common stock for each Pringles common share. The 29.1 million common shares issued by Diamond resulted in P&G shareholders’ participating in the exchange offer, owning a 57% stake in the combined firms, with Diamond’s shareholders owning the remainder.

The deal was structured as a reverse Morris Trust acquisition, which combines a divisive reorganization (e.g., a spin-off or a split-off) with an acquisitive reorganization (e.g., a statutory merger) to allow a tax-free transfer of a subsidiary under U.S. law. The use of a divisive reorganization results in the creation of a public company that is subsequently merged into a shell subsidiary (i.e., a privately owned company) of another firm, with the shell surviving.

The structure of the deal involved four discrete steps, outlined in separation and transaction agreements signed by P&G and Diamond. These steps included the following: (1) the creation by P&G of a wholly owned subsidiary containing Pringles’ assets and liabilities; (2) the recapitalization of the wholly owned Pringles subsidiary; (3) the separation of the wholly owned subsidiary through a split-off exchange offer; and (4) a merger with a wholly owned subsidiary of Diamond Foods. The separation agreement covered the first three steps, with the final step detailed in the transaction agreement.

Under the separation agreement, P&G contributed certain Pringles assets and liabilities to the Pringles Company, a newly formed wholly owned subsidiary of P&G. After P&G and Diamond reached a negotiated value for the Pringles Company equity of $1.5 billion, or $51.47 per share, the Pringles Company was subsequently recapitalized by issuing to P&G 29.1 million shares of Pringles Company stock. To complete the separation of Pringles from the parent firm, P&G distributed on the closing date Pringles shares to P&G shareholders participating in a share-exchange offer in which they agreed to exchange their P&G shares for Pringles shares.

In addition, the Pringles Company borrowed $850 million and used the proceeds to pay P&G a cash dividend and to acquire certain Pringles business assets held by P&G affiliates. Since P&G is the sole owner of the Pringles Company, the dividend is tax free to P&G because it is an intracompany transfer. If the exchange offer had not been fully subscribed, P&G would have distributed through a tax-free spin-off the remaining shares as a dividend to P&G shareholders.

The transaction agreement outlined the terms and conditions pertinent to completion of the merger with Diamond Foods. Immediately after the completion of the distribution, the Pringles Company merged with Merger Sub, a wholly owned shell subsidiary of Diamond, with Merger Sub’s continuing as the surviving company. The shares of Pringles Company common stock distributed in connection with the split-off exchange offer automatically converted into the right to receive shares of Diamond common stock on a one-for-one basis. After the merger, Diamond, through Merger Sub, owned and operated Pringles

Prior to the merger, Diamond already had formidable antitakeover defenses in place as part of its charter documents, including a classified board of directors, a prohibition against stockholders’ taking action by written consent (i.e., consent solicitation), and a requirement that stockholders give advance notice before raising matters at a stockholders’ meeting. Following the merger, Diamond adopted a shareholder-rights plan. The plan entitled the holder of such rights to purchase 1/100 of a share of Diamond’s Series A Junior Participating Preferred Stock if a person or group acquires 15% or more of Diamond’s outstanding common stock. Holders of this preferred stock (other than the person or group triggering their exercise) would be able to purchase Diamond common shares (flip-in poison pill) or those of any company into which Diamond is merged (flip-over poison pill) at a price of $60 per share. Such rights would expire in March 2015 unless extended by Diamond’s board of directors.

-How is value created for the P&G and Diamond shareholders in this type of transaction?

(Essay)

4.8/5 (43)

USX Bows to Shareholder Pressure to Split Up the Company

As one of the first firms to issue tracking stocks in the mid-1980s, USX relented to ongoing shareholder pressure to divide the firm into two pieces. After experiencing a sharp "boom/bust" cycle throughout the 1970s, U.S. Steel had acquired Marathon Oil, a profitable oil and gas company, in 1982 in what was at the time the second largest merger in U.S. history. Marathon had shown steady growth in sales and earnings throughout the 1970s. USX Corp. was formed in 1986 as the holding company for both U.S. Steel and Marathon Oil. In 1991, USX issued its tracking stocks to create "pure plays" in its primary businesses-steel and oil-and to utilize USX's steel losses, which could be used to reduce Marathon's taxable income. Marathon shareholders have long complained that Marathon's stock was selling at a discount to its peers because of its association with USX. The campaign to split Marathon from U.S. Steel began in earnest in early 2000.

On April 25, 2001, USX announced its intention to split U.S. Steel and Marathon Oil into two separately traded companies. The breakup gives holders of Marathon Oil stock an opportunity to participate in the ongoing consolidation within the global oil and gas industry. Holders of USX-U.S. Steel Group common stock (target stock) would become holders of newly formed Pittsburgh-based United States Steel Corporation, a return to the original name of the firm formed in 1901. Under the reorganization plan, U.S. Steel and Marathon would retain the same assets and liabilities already associated with each business. However, Marathon will assume $900 million in debt from U.S. Steel, leaving the steelmaker with $1.3 billion of debt. This assumption of debt by Marathon is an attempt to make U.S. Steel, which continued to lose money until 2004, able to stand on its own financially.

The investor community expressed mixed reactions, believing that Marathon would be likely to benefit from a possible takeover attempt, whereas U.S. Steel would not fare as well. Despite the initial investor pessimism, investors in both Marathon and U.S. Steel saw their shares appreciate significantly in the years immediately following the breakup.:

-Why do you think USX issued separate tracking stocks for its oil and steel businesses?

(Essay)

4.9/5 (39)

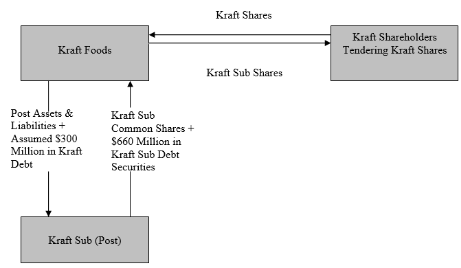

Step 1: Kraft creates a shell subsidiary (Kraft Sub) and transfers Post assets and liabilities and $300 million in Kraft debt into the shell in exchange for Kraft Sub stock plus $660 million in Kraft Sub debt securities. Kraft also implements an exchange offer of Kraft Sub for Kraft common stock.

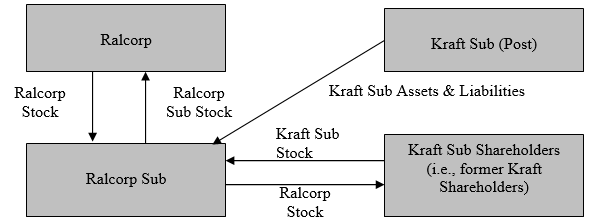

Step 2: Kraft Sub, as an independent company, is merged in a forward triangular tax-free merger with a sub of Ralcorp (Ralcorp Sub) in which Kraft Sub shares are exchanged for Ralcorp shares, with Ralcorp Sub surviving.

Step 2: Kraft Sub, as an independent company, is merged in a forward triangular tax-free merger with a sub of Ralcorp (Ralcorp Sub) in which Kraft Sub shares are exchanged for Ralcorp shares, with Ralcorp Sub surviving.

Sara Lee Attempts to Create Value through Restructuring

After spurning a series of takeover offers, Sara Lee, a global consumer goods company, announced in early 2011 its intention to split the firm into two separate publicly traded companies. The two companies would consist of the firm’s North American retail and food service division and its international beverage business. The announcement comes after a long string of restructuring efforts designed to increase shareholder value. It remains to be seen if the latest effort will be any more successful than earlier efforts.

Reflecting a flawed business strategy, Sara Lee had struggled for more than a decade to create value for its shareholders by radically restructuring its portfolio of businesses. The firm’s business strategy had evolved from one designed in the mid-1980s to market a broad array of consumer products from baked goods to coffee to underwear under the highly recognizable brand name of Sara Lee into one that was designed to refocus the firm on the faster-growing food and beverage and apparel businesses. Despite acquiring several European manufacturers of processed meats in the early 1990s, the company’s profits and share price continued to flounder.

In September 1997, Sara Lee embarked on a major restructuring effort designed to boost both profits, which had been growing by about 6% during the previous five years, and the company’s lagging share price. The restructuring program was intended to reduce the firm’s degree of vertical integration, shifting from a manufacturing and sales orientation to one focused on marketing the firm’s top brands. The firm increasingly viewed itself as more of a marketing than a manufacturing enterprise.

Sara Lee outsourced or sold 110 manufacturing and distribution facilities over the next two years. Nearly 10,000 employees, representing 7% of the workforce, were laid off. The proceeds from the sale of facilities and the cost savings from outsourcing were either reinvested in the firm’s core food businesses or used to repurchase $3 billion in company stock. 1n 1999 and 2000, the firm acquired several brands in an effort to bolster its core coffee operations, including such names as Chock Full o’Nuts, Hills Bros, and Chase & Sanborn.

Despite these restructuring efforts, the firm’s stock price continued to drift lower. In an attempt to reverse the firm’s misfortunes, the firm announced an even more ambitious restructuring plan in 2000. Sara Lee would focus on three main areas: food and beverages, underwear, and household products. The restructuring efforts resulted in the shutdown of a number of meat packing plants and a number of small divestitures, resulting in a 10% reduction (about 13,000 people) in the firm’s workforce. Sara Lee also completed the largest acquisition in its history, purchasing The Earthgrains Company for $1.9 billion plus the assumption of $0.9 billion in debt. With annual revenue of $2.6 billion, Earthgrains specialized in fresh packaged bread and refrigerated dough. However, despite ongoing restructuring activities, Sara Lee continued to underperform the broader stock market indices.

In February 2005, Sara Lee executed its most ambitious plan to transform the firm into a company focused on the global food, beverage, and household and body care businesses. To this end, the firm announced plans to dispose of 40% of its revenues, totaling more than $8 billion, including its apparel, European packaged meats, U.S. retail coffee, and direct sales businesses.

In 2006, the firm announced that it had completed the sale of its branded apparel business in Europe, Global Body Care and European Detergents units, and its European meat processing operations. Furthermore, the firm spun off its U.S. Branded Apparel unit into a separate publicly traded firm called HanesBrands Inc. The firm raised more than $3.7 billion in cash from the divestitures. The firm was now focused on its core businesses: food, beverages, and household and body care.

In late 2008, Sara Lee announced that it would close its kosher meat processing business and sold its retail coffee business. In 2009, the firm sold its Household and Body Care business to Unilever for $1.6 billion and its hair care business to Procter & Gamble for $0.4 billion.

In 2010, the proceeds of the divestitures made the prior year were used to repurchase $1.3 billion of Sara Lee’s outstanding shares. The firm also announced its intention to repurchase another $3 billion of its shares during the next three years. If completed, this would amount to about one-third of its approximate $10 billion market capitalization at the end of 2010.

What remains of the firm are food brands in North America, including Hillshire Farm, Ball Park, and Jimmy Dean processed meats and Sara Lee baked goods and Earthgrains. A food distribution unit will also remain in North America, as will its beverage and bakery operations. Sara Lee is rapidly moving to become a food, beverage, and bakery firm. As it becomes more focused, it could become a takeover target.

Has the 2005 restructuring program worked? To answer this question, it is necessary to determine the percentage change in Sara Lee’s share price from the announcement date of the restructuring program to the end of 2010, as well as the percentage change in the share price of HanesBrands Inc., which was spun off on August 18, 2006. Sara Lee shareholders of record received one share of HanesBrands Inc. for every eight Sara Lee shares they held.

Sara Lee’s share price jumped by 6% on the February 21, 2004 announcement date, closing at $19.56. Six years later, the stock price ended 2010 at $14.90, an approximate 24% decline since the announcement of the restructuring program in early 2005. Immediately following the spinoff, HanesBrands’ stock traded at $22.06 per share; at the end of 2010, the stock traded at $25.99, a 17.8% increase.

A shareholder owning 100 Sara Lee shares when the spin-off was announced would have been entitled to 12.5 HanesBrands shares. However, they would have actually received 12 shares plus $11.03 for fractional shares (i.e., 0.5 × $22.06).

A shareholder of record who had 100 Sara Lee shares on the announcement date of the restructuring program and held their shares until the end of 2010 would have seen their investment decline 24% from $1,956 (100 shares × $19.56 per share) to $1,486.56 by the end of 2010. However, this would have been partially offset by the appreciation of the HanesBrands shares between 2006 and 2010. Therefore, the total value of the hypothetical shareholder’s investment would have decreased by 7.5% from $1,956 to $1,809.47 (i.e., $1,486.56 + 12 HanesBrands shares × $25.99 + $11.03). This compares to a more modest 5% loss for investors who put the same $1,956 into a Standard & Poor’s 500 stock index fund during the same period.

Why did Sara Lee underperform the broader stock market indices during this period? Despite the cumulative buyback of more than $4 billion of its outstanding stock, Sara Lee’s fully diluted earnings per share dropped from $0.90 per share in 2005 to $0.52 per share in 2009. Furthermore, the book value per share, a proxy for the breakup or liquidation value of the firm, dropped from $3.28 in 2005 to $2.93 in 2009, reflecting the ongoing divestiture program. While the HanesBrands spin-off did create value for the shareholder, the amount was far too modest to offset the decline in Sara Lee’s market value. During the same period, total revenue grew at a tepid average annual rate of about 3% to about $13 billion in 2009.

-Why is a breakup strategy conceptually simple to explain but often difficult to implement? Be specific.

Sara Lee Attempts to Create Value through Restructuring

After spurning a series of takeover offers, Sara Lee, a global consumer goods company, announced in early 2011 its intention to split the firm into two separate publicly traded companies. The two companies would consist of the firm’s North American retail and food service division and its international beverage business. The announcement comes after a long string of restructuring efforts designed to increase shareholder value. It remains to be seen if the latest effort will be any more successful than earlier efforts.

Reflecting a flawed business strategy, Sara Lee had struggled for more than a decade to create value for its shareholders by radically restructuring its portfolio of businesses. The firm’s business strategy had evolved from one designed in the mid-1980s to market a broad array of consumer products from baked goods to coffee to underwear under the highly recognizable brand name of Sara Lee into one that was designed to refocus the firm on the faster-growing food and beverage and apparel businesses. Despite acquiring several European manufacturers of processed meats in the early 1990s, the company’s profits and share price continued to flounder.

In September 1997, Sara Lee embarked on a major restructuring effort designed to boost both profits, which had been growing by about 6% during the previous five years, and the company’s lagging share price. The restructuring program was intended to reduce the firm’s degree of vertical integration, shifting from a manufacturing and sales orientation to one focused on marketing the firm’s top brands. The firm increasingly viewed itself as more of a marketing than a manufacturing enterprise.

Sara Lee outsourced or sold 110 manufacturing and distribution facilities over the next two years. Nearly 10,000 employees, representing 7% of the workforce, were laid off. The proceeds from the sale of facilities and the cost savings from outsourcing were either reinvested in the firm’s core food businesses or used to repurchase $3 billion in company stock. 1n 1999 and 2000, the firm acquired several brands in an effort to bolster its core coffee operations, including such names as Chock Full o’Nuts, Hills Bros, and Chase & Sanborn.

Despite these restructuring efforts, the firm’s stock price continued to drift lower. In an attempt to reverse the firm’s misfortunes, the firm announced an even more ambitious restructuring plan in 2000. Sara Lee would focus on three main areas: food and beverages, underwear, and household products. The restructuring efforts resulted in the shutdown of a number of meat packing plants and a number of small divestitures, resulting in a 10% reduction (about 13,000 people) in the firm’s workforce. Sara Lee also completed the largest acquisition in its history, purchasing The Earthgrains Company for $1.9 billion plus the assumption of $0.9 billion in debt. With annual revenue of $2.6 billion, Earthgrains specialized in fresh packaged bread and refrigerated dough. However, despite ongoing restructuring activities, Sara Lee continued to underperform the broader stock market indices.

In February 2005, Sara Lee executed its most ambitious plan to transform the firm into a company focused on the global food, beverage, and household and body care businesses. To this end, the firm announced plans to dispose of 40% of its revenues, totaling more than $8 billion, including its apparel, European packaged meats, U.S. retail coffee, and direct sales businesses.

In 2006, the firm announced that it had completed the sale of its branded apparel business in Europe, Global Body Care and European Detergents units, and its European meat processing operations. Furthermore, the firm spun off its U.S. Branded Apparel unit into a separate publicly traded firm called HanesBrands Inc. The firm raised more than $3.7 billion in cash from the divestitures. The firm was now focused on its core businesses: food, beverages, and household and body care.

In late 2008, Sara Lee announced that it would close its kosher meat processing business and sold its retail coffee business. In 2009, the firm sold its Household and Body Care business to Unilever for $1.6 billion and its hair care business to Procter & Gamble for $0.4 billion.

In 2010, the proceeds of the divestitures made the prior year were used to repurchase $1.3 billion of Sara Lee’s outstanding shares. The firm also announced its intention to repurchase another $3 billion of its shares during the next three years. If completed, this would amount to about one-third of its approximate $10 billion market capitalization at the end of 2010.

What remains of the firm are food brands in North America, including Hillshire Farm, Ball Park, and Jimmy Dean processed meats and Sara Lee baked goods and Earthgrains. A food distribution unit will also remain in North America, as will its beverage and bakery operations. Sara Lee is rapidly moving to become a food, beverage, and bakery firm. As it becomes more focused, it could become a takeover target.

Has the 2005 restructuring program worked? To answer this question, it is necessary to determine the percentage change in Sara Lee’s share price from the announcement date of the restructuring program to the end of 2010, as well as the percentage change in the share price of HanesBrands Inc., which was spun off on August 18, 2006. Sara Lee shareholders of record received one share of HanesBrands Inc. for every eight Sara Lee shares they held.

Sara Lee’s share price jumped by 6% on the February 21, 2004 announcement date, closing at $19.56. Six years later, the stock price ended 2010 at $14.90, an approximate 24% decline since the announcement of the restructuring program in early 2005. Immediately following the spinoff, HanesBrands’ stock traded at $22.06 per share; at the end of 2010, the stock traded at $25.99, a 17.8% increase.

A shareholder owning 100 Sara Lee shares when the spin-off was announced would have been entitled to 12.5 HanesBrands shares. However, they would have actually received 12 shares plus $11.03 for fractional shares (i.e., 0.5 × $22.06).

A shareholder of record who had 100 Sara Lee shares on the announcement date of the restructuring program and held their shares until the end of 2010 would have seen their investment decline 24% from $1,956 (100 shares × $19.56 per share) to $1,486.56 by the end of 2010. However, this would have been partially offset by the appreciation of the HanesBrands shares between 2006 and 2010. Therefore, the total value of the hypothetical shareholder’s investment would have decreased by 7.5% from $1,956 to $1,809.47 (i.e., $1,486.56 + 12 HanesBrands shares × $25.99 + $11.03). This compares to a more modest 5% loss for investors who put the same $1,956 into a Standard & Poor’s 500 stock index fund during the same period.

Why did Sara Lee underperform the broader stock market indices during this period? Despite the cumulative buyback of more than $4 billion of its outstanding stock, Sara Lee’s fully diluted earnings per share dropped from $0.90 per share in 2005 to $0.52 per share in 2009. Furthermore, the book value per share, a proxy for the breakup or liquidation value of the firm, dropped from $3.28 in 2005 to $2.93 in 2009, reflecting the ongoing divestiture program. While the HanesBrands spin-off did create value for the shareholder, the amount was far too modest to offset the decline in Sara Lee’s market value. During the same period, total revenue grew at a tepid average annual rate of about 3% to about $13 billion in 2009.

-Why is a breakup strategy conceptually simple to explain but often difficult to implement? Be specific.

(Essay)

4.8/5 (31)

Viacom to Spin Off Blockbuster

After months of trying to sell its 81% stake in Blockbuster Inc. undertook a tax-free spin-off in mid 2004. Viacom shareholders will have the option to swap their Viacom shares for Blockbuster shares and a special cash payout. Blockbuster had been hurt by competition from low-priced rivals and the erosion of video rentals by accelerating DVD sales. Despite Blockbuster's steady contribution to Viacom's overall cash flow, Viacom believed that the growth prospects for the unit were severely limited. In preparation for the spin-off, Viacom had reported a $1.3 billion charge to earnings in the fourth quarter of 2003 in writing down goodwill associated with its acquisition of Blockbuster. By spinning off Blockbuster, Viacom Chairman and ECO Sumner Redstone statd that the firm would now be able to focus on its core TV (i.e., CBS and MTV) and movie (i.e., Paramount Studios) businesses. Blockbuster shares fell by 4% and Viacom shares rose by 1% on the day of the announcement.

-Why would Viacom choose to spin-off rather than divest its Blockbuster unit? Explain your answer.

(Essay)

4.7/5 (40)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)