Exam 13: Current Liabilities and Contingencies

Exam 1: Financial Accounting and Accounting Standards103 Questions

Exam 2: Conceptual Framework for Financial Reporting155 Questions

Exam 3: The Accounting Information System144 Questions

Exam 4: Income Statement and Related Information139 Questions

Exam 5: Balance Sheet and Statement of Cash Flows127 Questions

Exam 6: Accounting and the Time Value of Money152 Questions

Exam 7: Cash and Receivables173 Questions

Exam 8: Valuation of Inventories: a Cost-Basis Approach173 Questions

Exam 9: Inventories: Additional Valuation Issues168 Questions

Exam 10: Acquisition and Disposition of Property, Plant, and Equipment170 Questions

Exam 11: Depreciation, Impairments, and Depletion156 Questions

Exam 12: Intangible Assets171 Questions

Exam 13: Current Liabilities and Contingencies170 Questions

Exam 14: Long-Term Liabilities140 Questions

Exam 15: Stockholders Equity155 Questions

Exam 16: Dilutive Securities and Earnings Per Share160 Questions

Exam 17: Investments141 Questions

Exam 18: Revenue Recognition145 Questions

Exam 19: Accounting for Income Taxes127 Questions

Exam 20: Accounting for Pensions and Postretirement Benefits137 Questions

Exam 21: Accounting for Leases128 Questions

Exam 22: Accounting Changes and Error Analysis103 Questions

Exam 23: Statement of Cash Flows143 Questions

Exam 24: Full Disclosure in Financial Reporting108 Questions

Exam 25: Appendix89 Questions

Select questions type

Among the short-term obligations of Larsen Company as of December 31, the balance sheet date, are notes payable totaling $250,000 with the Dennison National Bank. These are 90-day notes, renewable for another 90-day period. These notes should be classified on the balance sheet of Larsen Company as

(Multiple Choice)

4.7/5  (33)

(33)

To record an asset retirement obligation (ARO), the cost associated with the ARO is

(Multiple Choice)

4.9/5 (41)

Venible newspapers sold 6,000 of annual subscriptions at $125 each on June 1. How much unearned revenue will exist as of December 31?

(Multiple Choice)

4.8/5 (43)

Which of the following is true about accounts payable?1. Accounts payable are also called trade accounts payable.2. When accounts payable are recorded at the net amount, a Purchase Discounts account will be used.3. When accounts payable are recorded at the gross amount, a Purchase Discounts Lost account will be used.

(Multiple Choice)

4.9/5 (40)

Described below are certain transactions of Lamar Company for 2014:1. On May 10, the company purchased goods from Fox Company for $75,000, terms 2/10, n/30. Purchases and accounts payable are recorded at net amounts. The invoice was paid on May 18.2. On June 1, the company purchased equipment for $90,000 from Rao Company, paying $30,000 in cash and giving a one-year, 9% note for the balance."3. On September 30, the company discounted at 10% its $200,000, one-year zero-interest-bearing note at Virginia State Bank.

Instructions

(a) Prepare the journal entries necessary to record the transactions above using appropriate dates.

(b) Prepare the adjusting entries necessary at December 31, 2014 in order to properly report interest expense related to the above transactions. Assume straight-line amortization of discounts.

(c) Indicate the manner in which the above transactions should be reflected in the Current Liabilities section of Lamar Company's December 31, 2014 balance sheet."

(Essay)

4.8/5 (39)

Which of the following contingencies need not be disclosed in the financial statements or the related notes?

(Multiple Choice)

4.8/5 (38)

On September 1, Horton purchased $13,300 of inventory items on credit with the terms 1/15, net 30, FOB destination. Freight charges were $280. Payment for the purchase was made on September 18. Assuming Horton uses the perpetual inventory system and the net method of accounting for purchase discounts, what amount is recorded as inventory from this purchase?

(Multiple Choice)

4.8/5 (34)

Contingent assets are not reported in the statement of financial position.

(True/False)

4.9/5 (32)

Crispy Frosted Flakes Company offers its customers a pottery cereal bowl if they send in 4 boxtops from Crispy Frosted Flakes boxes and $1. The company estimates that 60% of the boxtops will be redeemed. In 2014, the company sold 500,000 boxes of Frosted Flakes and customers redeemed 220,000 boxtops receiving 55,000 bowls. If the bowls cost Crispy Company $3 each, how much liability for outstanding premiums should be recorded at the end of 2014?

(Multiple Choice)

4.8/5 (42)

A short-term obligation can be excluded from current liabilities if the company intends to refinance it on a long-term basis and demonstrates the ability to consummate the refinancing.

(True/False)

4.8/5 (33)

Why is the liability section of the balance sheet of primary importance to bankers?

(Multiple Choice)

4.7/5 (40)

In 2014, Pollard Corporation began selling a new line of products that carry a two-year warranty against defects. Based upon past experience with other products, the estimated warranty costs related to dollar sales are as follows:First year of warranty 3%Second year of warranty 5%Sales and actual warranty expenditures for 2014 and 2015 are presented below:  What is the estimated warranty liability at the end of 2015?(assume the accrual method)

A) $16,000.

B) $64,000.

C) $96,000.

D) $20,000.

What is the estimated warranty liability at the end of 2015?(assume the accrual method)

A) $16,000.

B) $64,000.

C) $96,000.

D) $20,000.

(Short Answer)

4.8/5 (42)

Ebbert Company's salaried employees are paid biweekly. Occasionally, advances made to employees are paid back by payroll deductions. Information relating to salaries for the calendar year 2015 is as follows:  At December 31, 2015, what amount should Ebbert report for accrued salaries payable?

At December 31, 2015, what amount should Ebbert report for accrued salaries payable?

(Multiple Choice)

4.7/5 (37)

The cause for litigation must have occurred on or before the date of the financial statements to report a liability in the financial statements.

(True/False)

4.8/5 (33)

Flavor Food Company distributes to consumers coupons which may be presented (on or before a stated expiration date) to grocers for discounts on certain products of Flavor. The grocers are reimbursed when they send the coupons to Flavor. In Flavor's experience, 50% of such coupons are redeemed, and generally one month elapses between the date a grocer receives a coupon from a consumer and the date Flavor receives it. During 2014 Flavor issued two separate series of coupons as follows:  The only journal entry recorded to date is: debit to coupon expense and credit to cash of $715,000. The December 31, 2014 balance sheet should include a liability for unredeemed coupons of:

The only journal entry recorded to date is: debit to coupon expense and credit to cash of $715,000. The December 31, 2014 balance sheet should include a liability for unredeemed coupons of:

(Multiple Choice)

4.8/5 (32)

The ability to consummate the refinancing of a short-term obligation may be demon- strated by

(Multiple Choice)

4.8/5 (35)

Use the following information for questions 127, 128, and 129.

Muggs Co. includes one coupon in each bag of dog food it sells. In return for eight coupons, customers receive a leash. The leashes cost Muggs $3 each. Muggs estimates that 45 percent of the coupons will be redeemed. Data for 2014 and 2015 are as follows:  -The premium liability at December 31, 2014 is

-The premium liability at December 31, 2014 is

(Multiple Choice)

4.8/5 (45)

Under IFRS, which of the following is used to measure a liability, if a range of estimates is predicted and no amount in the range is more likely than any other amount in the range?

(Multiple Choice)

4.8/5 (39)

Contingent liabilities are not reported in the financial statements but may be disclosed in the notes to the financial statements if the likelihood of an unfavorable outcome is possible.

(True/False)

4.7/5 (41)

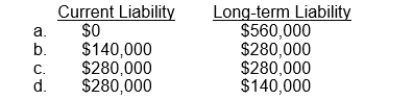

On January 1, 2012, Bacon Co. leased a building to Horner Corp. for a ten-year term at an annual rental of $140,000. At inception of the lease, Bacon received $560,000 covering the first two years' rent of $280,000 and a security deposit of $280,000. This deposit will not be returned to Horner upon expiration of the lease but will be applied to payment of rent for the last two years of the lease. What portion of the $560,000 should be shown as a current and long-term liability, respectively, in Bacon's December 31, 2012 balance sheet?

(Short Answer)

4.9/5 (43)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)