Exam 7: Fraud, Internal Control, and Cash

Exam 1: Accounting in Action243 Questions

Exam 2: The Recording Process195 Questions

Exam 3: Adjusting the Accounts219 Questions

Exam 4: Completing the Accounting Cycle225 Questions

Exam 5: Accounting for Merchandising Operations Perpetual Approach209 Questions

Exam 6: Inventories Periodic Approach203 Questions

Exam 7: Fraud, Internal Control, and Cash229 Questions

Exam 8: Accounting for Receivables238 Questions

Exam 9: Plant Assets, Natural Resources, and Intangible Assets291 Questions

Exam 10: Liabilities267 Questions

Exam 11: Corporations: Organization, Stock Transactions, and Stockholders Equity341 Questions

Exam 12: Statement of Cash Flows161 Questions

Exam 13: Financial Statement Analysis259 Questions

Exam 14: Managerial Accounting213 Questions

Exam 15: Job Order Costing205 Questions

Exam 16: Process Costing182 Questions

Exam 17: Activity-Based Costing185 Questions

Exam 18: Cost-Volume-Profit210 Questions

Exam 19: Cost-Volume-Profit Analysis: Additional Issues102 Questions

Exam 20: Incremental Analysis203 Questions

Exam 21: Pricing144 Questions

Exam 22: Budgetary Planning213 Questions

Exam 23: Budgetary Control and Responsibility Accounting210 Questions

Exam 24: Standard Costs and Balanced Scorecard204 Questions

Exam 25: Planning for Capital Investments192 Questions

Exam 26: Time Value of Money46 Questions

Exam 27: Investments202 Questions

Exam 28: Payroll Accounting38 Questions

Exam 29: Subsidiary Ledgers and Special Journals87 Questions

Exam 30: Other Significant Liabilities40 Questions

Select questions type

For accounting purposes, postdated checks (checks payable in the future) are considered to be

(Multiple Choice)

5.0/5  (40)

(40)

Identify the internal control procedures applicable to cash disbursements followed by Downey Company in each of the following cases.

1. Company checks are pre-numbered.

2. Only the treasurer is authorized to sign checks.

3. All employees are required to take vacations.

4. Blank checks are stored in a locked safe.

5. The bookkeeper, not the treasurer, records cash disbursements.

(Essay)

4.8/5 (45)

Harnish Company needs to make adjusting entries for each of the following reconciling items. Identify the account to be debited and the account to be credited in each case.

1. A check for $127 written to the company by J. Chandler was returned NSF.

2. The monthly service charge by the bank was $20.

3. The bank collected a $1,000 note plus interest of $100 on the company's behalf. The company had not accrued the interest.

(Essay)

4.8/5 (37)

Checks from customers who pay their accounts promptly are called outstanding checks.

(True/False)

4.9/5 (42)

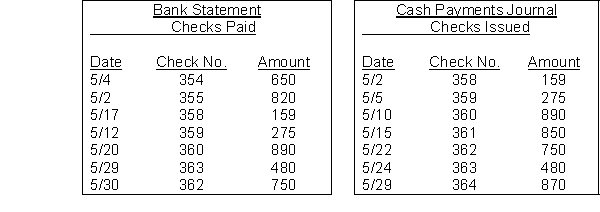

On April 30, the bank reconciliation of Baxter Company shows three outstanding checks: no. 354, $650, no. 355, $820, and no. 357, $615. The May bank statement and the May cash payments journal show the following.  Instructions

Using step 2 in the reconciliation procedure, list the outstanding checks at May 31.

Instructions

Using step 2 in the reconciliation procedure, list the outstanding checks at May 31.

(Essay)

4.7/5 (39)

Internal control is most effective when several people are responsible for a given task.

(True/False)

4.9/5 (41)

Cash registers are an important internal control device used in controlling over-the-counter receipts.

(True/False)

4.9/5 (49)

Identify whether each of the following items would be (a) added to the book balance, or (b) deducted from the book balance in a bank reconciliation.

1. EFT transfer to a supplier

2. Bank service charge

3. Check printing charge

4. Error recording check # 214 which was written for $450 but recorded for $540

5. Collection of note and interest by bank on company's behalf

(Short Answer)

4.8/5 (35)

A bank reconciliation is generally prepared by the bank and sent to the depositor along with cancelled checks.

(True/False)

4.8/5 (40)

In the month of November, Kinsey Company Inc. wrote checks in the amount of $18,500. In December, checks in the amount of $25,316 were written. In November, $16,936 of these checks were presented to the bank for payment, and $21,766 were presented in December. What is the amount of outstanding checks at the end of November?

(Multiple Choice)

4.9/5 (36)

Bell Food Store developed the following information in recording its bank statement for the month of March.  (1) Checks written in March but still outstanding $7,000.

(2) Checks written in February but still outstanding $3,100.

(3) Deposits of March 30 and 31 not yet recorded by bank $5,200.

(4) NSF check of customer returned by bank $1,200.

(5) Check No. 210 for $593 was correctly issued and paid by bank but incorrectly entered in the cash payments journal as payment on account for $539.

(6) Bank service charge for March was $50.

(7) A payment on account was incorrectly entered in the cash payments journal and posted to the accounts payable subsidiary ledger for $824 when Check No. 318 was correctly prepared for $284. The check cleared the bank in March.

(8) The bank collected a note receivable for the company for $3,000 plus $100 interest revenue.

Instructions

Prepare a bank reconciliation at March 31.

(1) Checks written in March but still outstanding $7,000.

(2) Checks written in February but still outstanding $3,100.

(3) Deposits of March 30 and 31 not yet recorded by bank $5,200.

(4) NSF check of customer returned by bank $1,200.

(5) Check No. 210 for $593 was correctly issued and paid by bank but incorrectly entered in the cash payments journal as payment on account for $539.

(6) Bank service charge for March was $50.

(7) A payment on account was incorrectly entered in the cash payments journal and posted to the accounts payable subsidiary ledger for $824 when Check No. 318 was correctly prepared for $284. The check cleared the bank in March.

(8) The bank collected a note receivable for the company for $3,000 plus $100 interest revenue.

Instructions

Prepare a bank reconciliation at March 31.

(Essay)

4.9/5 (32)

A __________________ fund is used to pay relatively small expenditures.

(Short Answer)

4.8/5 (31)

The petty cash fund eliminates the need for a bank checking account.

(True/False)

4.8/5 (39)

In the month of May, Kijak Company Inc. wrote checks in the amount of $56,000. In June, checks in the amount of $76,000 were written. In May, $50,000 of these checks were presented to the bank for payment, and $66,000 in June. What is the amount of outstanding checks at the end of June?

(Multiple Choice)

4.7/5 (38)

When two or more people get together for the purpose of circumventing prescribed controls, it is called

(Multiple Choice)

4.7/5 (42)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)