Exam 8: Applications: The Costs of Taxation

Exam 1: Ten Principles of Economics220 Questions

Exam 2: Thinking Like an Economist284 Questions

Exam 3: Interdependence and the Gains From Trade192 Questions

Exam 4: The Market Forces of Supply and Demand277 Questions

Exam 5: Elasticity and Its Application222 Questions

Exam 6: Supply, Demand, and Government Policies321 Questions

Exam 7: Consumers, Producers, and the Efficiency of Markets218 Questions

Exam 8: Applications: The Costs of Taxation203 Questions

Exam 9: Application: International Trade214 Questions

Exam 10: Externalities204 Questions

Exam 11: Public Goods and Common Resources182 Questions

Exam 12: The Design of the Tax System225 Questions

Exam 13: The Costs of Production261 Questions

Exam 14: Firms in Competitive Markets243 Questions

Exam 15: Monopoly231 Questions

Exam 16: Monopolistic Competition246 Questions

Exam 17: Oligopoly204 Questions

Exam 18: The Markets for the Factors of Production232 Questions

Exam 19: Earnings and Discrimination230 Questions

Exam 20: Income Inequality and Poverty194 Questions

Exam 21: The Theory of Consumer Choice209 Questions

Exam 22: Frontiers in Microeconomics185 Questions

Exam 23: Measuring a Nations Income231 Questions

Exam 24: Measuring the Cost of Living214 Questions

Exam 25: Production and Growth187 Questions

Exam 26: Saving, Investment, and the Financial System225 Questions

Exam 27: Tools of Finance198 Questions

Exam 28: Unemployment and Its Natural Rate361 Questions

Exam 29: The Monetary System210 Questions

Exam 30: Money Growth and Inflation201 Questions

Exam 31: Open-Economy Macroeconomics: Basic Concepts194 Questions

Exam 32: A Macroeconomic Theory of the Open Economy188 Questions

Exam 33: Aggregate Demand and Aggregate Supply189 Questions

Exam 34: The Influence of Monetary and Fiscal Policy on Aggregate Demand207 Questions

Exam 35: The Short-Run Tradeoff Between Inflation and Unemployment223 Questions

Exam 36: Six Debates Over Macroeconomic Policy154 Questions

Select questions type

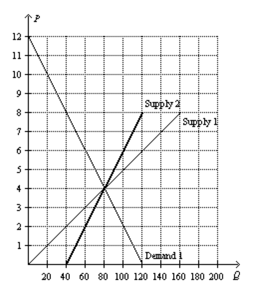

Figure 8-12

-Refer to Figure 8-12. Suppose that Market A is characterized by Demand 1 and Supply 1, and Market B is characterized by Demand 1 and Supply 2. If an identical tax is imposed on each market, the tax will create a larger deadweight loss in which market? Explain.

-Refer to Figure 8-12. Suppose that Market A is characterized by Demand 1 and Supply 1, and Market B is characterized by Demand 1 and Supply 2. If an identical tax is imposed on each market, the tax will create a larger deadweight loss in which market? Explain.

(Essay)

4.7/5  (37)

(37)

Total surplus in a market does not change when the government imposes a tax on that market because the loss of consumer surplus and producer surplus is equal to the gain of government revenue.

(True/False)

4.9/5 (36)

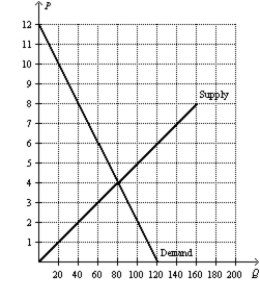

Figure 8-10

-Refer to Figure 8-10. Suppose the government places a $3 tax per unit on this good. How many units of this good will be bought and sold after the tax is imposed?

-Refer to Figure 8-10. Suppose the government places a $3 tax per unit on this good. How many units of this good will be bought and sold after the tax is imposed?

(Essay)

4.7/5 (34)

The more inelastic are demand and supply, the greater is the deadweight loss of a tax.

(True/False)

4.9/5 (33)

Suppose that instead of a supply-demand diagram, you are given the following information:

Qs = 100 + 3P

Qd = 400 - 2P

From this information compute equilibrium price and quantity. Now suppose that a tax is placed on buyers so that

Qd = 400 - 2(P + T).

If T = 15, solve for the new equilibrium price and quantity. (Note: P is the price received by sellers and P + T is the price paid by buyers.) Compare these answers for equilibrium price and quantity with your first answers. What does this show you?

(Essay)

4.8/5 (41)

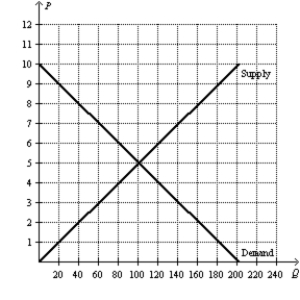

Figure 8-9

-Refer to Figure 8-9. How much is consumer surplus at the market equilibrium?

-Refer to Figure 8-9. How much is consumer surplus at the market equilibrium?

(Essay)

4.9/5 (38)

The result of the large tax cuts in the first Reagan Administration demonstrated very convincingly that Arthur Laffer was correct when he asserted that cuts in tax rates would increase tax revenue.

(True/False)

4.9/5 (37)

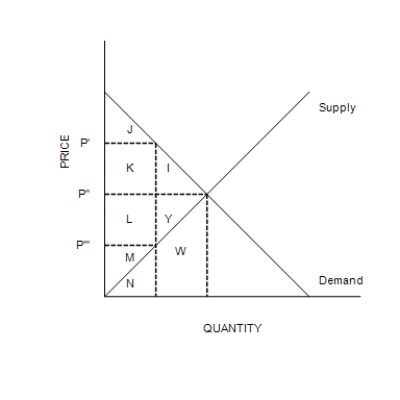

Figure 8-1  -Refer to Figure 8-1. Suppose the government imposes a tax of P' - P'''. The area measured by I + Y represents the

-Refer to Figure 8-1. Suppose the government imposes a tax of P' - P'''. The area measured by I + Y represents the

(Multiple Choice)

4.8/5 (31)

Figure 8-9

-Refer to Figure 8-9. Suppose the government places a $4 tax per unit on this good. How much is producer surplus after the tax is imposed?

(Essay)

4.8/5 (28)

When the government imposes taxes on buyers and sellers of a good, society loses some of the benefits of market efficiency.

(True/False)

4.8/5 (48)

Figure 8-2

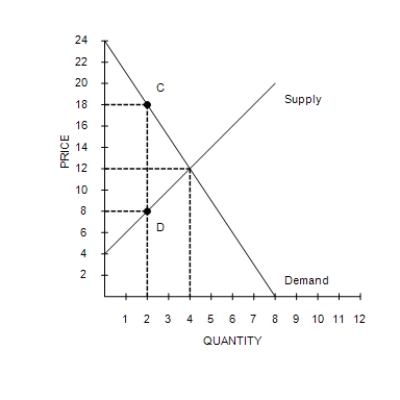

The vertical distance between points C and D represents a tax in the market.

-Refer to Figure 8-2. The imposition of the tax causes the quantity sold to

-Refer to Figure 8-2. The imposition of the tax causes the quantity sold to

(Multiple Choice)

4.7/5 (36)

Figure 8-10

-Refer to Figure 8-10. Suppose the government places a $3 tax per unit on this good. How much is the deadweight loss from this tax?

(Essay)

4.8/5 (42)

The deadweight loss from a tax per unit of good will be smallest in a market with

(Multiple Choice)

4.9/5 (41)

Assume the price of gasoline is $2.00 per gallon, and the equilibrium quantity of gasoline is 10 million gallons per day with no tax on gasoline. Starting from this initial situation, which of the following scenarios would result in the largest deadweight loss?

(Multiple Choice)

4.7/5 (39)

Taxes cause deadweight losses because they prevent buyers and sellers from realizing some of the gains from trade.

(True/False)

4.9/5 (49)

In terms of gains from trade, why is it true that taxes cause deadweight losses?

(Essay)

4.9/5 (40)

Economists use the government's tax revenue to measure the public benefit from a tax.

(True/False)

4.9/5 (36)

Figure 8-9

-Refer to Figure 8-9. Suppose the government places a $4 tax per unit on this good. How much is consumer surplus after the tax is imposed?

(Essay)

4.9/5 (43)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)