Exam 3: Basics of Interest Rate Risk Management

Exam 1: An Introduction to Fixed Income Markets17 Questions

Exam 2: Basics of Fixed Income Securities20 Questions

Exam 3: Basics of Interest Rate Risk Management17 Questions

Exam 4: Basic Refinements in Interest Rate Risk Management18 Questions

Exam 5: Interest Rate Derivatives: Forwards and Swaps15 Questions

Exam 6: Interest Rate Derivatives: Futures and Options15 Questions

Exam 7: Inflation, Monetary Policy, and the Federal Funds Rate15 Questions

Exam 8: Basics of Residential Mortgage Backed Securities21 Questions

Exam 9: One Step Binomial Trees15 Questions

Exam 10: Multi-Step Binomial Trees15 Questions

Exam 11: Risk Neutral Trees and Derivative Pricing18 Questions

Exam 12: American Options19 Questions

Exam 13: Monte Carlo Simulations on Trees18 Questions

Exam 14: Interest Rate Models in Continuous Time15 Questions

Exam 15: No Arbitrage and the Pricing of Interest Rate Securities17 Questions

Exam 16: Dynamic Hedging and Relative Value Trades13 Questions

Exam 17: Dynamic Hedging and Relative Value Trades18 Questions

Exam 18: The Risk and Return of Interest Rate Securities11 Questions

Exam 19: No Arbitrage Models and Standard Derivatives20 Questions

Exam 20: The Market Model for Standard Derivatives19 Questions

Exam 21: Forward Risk Neutral Pricing and the Libor Market Model14 Questions

Exam 22: Multifactor Models16 Questions

Select questions type

Calculate the Modified Duration for the same security.

Free

(Essay)

4.8/5  (33)

(33)

Correct Answer: Verified

Verified

The Modified Duration for the bond is 0.9533.

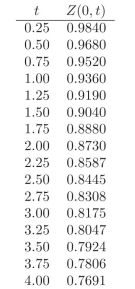

Use the following discount factors when needed.  -Calculate the duration of the following security: 5-year zero coupon bond.

-Calculate the duration of the following security: 5-year zero coupon bond.

Free

(Short Answer)

4.8/5 (38)

Correct Answer:Verified

The duration of the security is 5.00.

Compute the 95% VaR for the following portfolio:

i. A 1.5-year ?xed rate bond paying 2% quarterly.

ii. A 0.75-year ?oating rate bond paying ?oat plus 80 basis points semi- annually. You know that the reference rate was set to 6% six months ago.

iii. A 0.25 zero coupon bond. Additionally you know that ?dr =0and?dr =0.4233.

Free

(Short Answer)

4.8/5 (41)

Correct Answer:Verified

The 95%VaR=1.3116.

What is the dollar duration of the following portfolio:

i. Long a 2-year ?xed coupon bond paying 7% quarterly.

ii. Short three 1.25-year ?oating rate bonds paying ?oat plus 80 bps semiannually. You know that the reference rate was set at 7% six months ago.

iii. Short two 0.5-year zero coupon bonds.

(Short Answer)

4.9/5 (45)

You have two bond coupon with the same maturity, one has a 9% coupon paid semiannually and the other a 8% coupon paid semiannually. Which one has a higher duration?

(Essay)

4.9/5 (29)

Calculate the MacCaulay Duration for the following security: 1-year fixed rate coupon bond paying 6% semiannually. You know that the yield of the bond is 6.72%.

(Essay)

4.9/5 (38)

Suppose that you calculate VaR from Duration. In your many results you ?nd that:

i. using historical data (of whatever length) or a normal distribution does not a?ect the result; 11

ii. you ?nd that kurtosis between historical data and the normal distri- bution is almost identical;

iii. You ?nd the expected change in the portfolio ?P = 0, with very small standard errors. Given the above, can you say that this Duration based VaR is an appro- priate approach to measure risk?

(Essay)

5.0/5 (40)

What is the dollar duration of the following portfolio:

i. Long a 1-year ?xed coupon bond paying 4% quarterly.

ii. Long a 1.75-year ?oating rate bond paying ?oat plus 80 bps semian- nually. You know that the reference rate was set at 6% six months ago.

iii. Short a 2-year zero coupon bond. 10

(Essay)

4.7/5 (39)

What is the PV01 of the following portfolio?

i. Long a 2-year ?xed coupon bond paying 7% quarterly.

ii. Short three 1.25-year ?oating rate bonds paying ?oat plus 80 bps semiannually. You know that the reference rate was set at 7% six months ago.

iii. Short two 0.5-year zero coupon bonds.

(Short Answer)

4.9/5 (42)

Use the following discount factors when needed.

-Calculate the duration of the following security: 1.25-year ?oating coupon paying ?oat + 50 bps semiannually. You know that last quarter the semi- annual rate was 6.4%.

(Short Answer)

4.7/5 (31)

What is the PV01 of the following portfolio?

i. Long a 1-year ?xed coupon bond paying 4% quarterly.

ii. Long a 1.75-year ?oating rate bond paying ?oat plus 80 bps semian- nually. You know that the reference rate was set at 6% six months ago.

iii. Short a 2-year zero coupon bond.

(Short Answer)

4.9/5 (27)

Use the following discount factors when needed.

-Calculate the duration of the following portfolio:

i. 3 units of a 0.75-year ?xed rate bond paying 6% quarterly.

ii. 4 units of a 2-year ?xed rate bond paying 3% semiannually.

iii. 7 units of a 1.75-year zero coupon bond.

iv. 1 unit of a 2-year ?oating rate bond with no spread paid semiannually.

(Short Answer)

4.8/5 (27)

Use the following discount factors when needed.

-Calculate the duration of the following portfolio:

i. 5 units of a 2-year ?xed rate bond paying 6% quarterly.

ii. 2 units of a 1.75-year ?oating rate bond paying ?oat + 80 bps semi- annually. You know that the reference rate was 6.5% three months ago.

iii. 6 units of a 1-year zero coupon bond.

iv. 5 units of a 1.5-year ?oating rate bond with no spread paid semian- nually.

(Short Answer)

4.9/5 (37)

What is the dollar duration of the following portfolio?

i. Long a 1.5-year zero coupon bond.

ii. Short a 2-year ?xed coupon bond paying 1% quarterly.

(Essay)

4.8/5 (33)

What is the duration of the following portfolio?

i. Long a 1.5-year zero coupon bond.

ii. Short a 2-year ?xed coupon bond paying 1% quarterly.

(Essay)

4.8/5 (40)

Use the following discount factors when needed.

-Calculate the duration of the following security: 2-year ?xed coupon pay- ing 5% quarterly.

(Short Answer)

4.8/5 (34)

Mr. Brown wants to invest $100,000 for the next ?ve years. He purchases an annuity from a ?nancial institution. Currently the term structure is ?at at 10% (yearly compounded).

i. If the payments are made yearly, what is the amount that the ?nan- cial institution will agree to pay Mr. Brown?

ii. Assume that there is a 5-year ?xed coupon bond that pays 12% coupon every year. What is the price and duration of the bond?

iii. How much must the ?nancial institution invest in the long-term bond in order to hedge the position? What should it do with the remainder of the money?

(Essay)

4.8/5 (38)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)