Exam 8: Output, Price, and Profit: the Importance of Marginal Analysis

Exam 1: What Is Economics254 Questions

Exam 2: The Economony: Myth and Reality184 Questions

Exam 3: The Fundamental Economic Problem: Scarcity and Choice278 Questions

Exam 4: Supply and Demand: an Initial Look297 Questions

Exam 5: Consumer Choice: Individual and Market Demand213 Questions

Exam 6: Demand and Elasticity247 Questions

Exam 7: Production, Inputs, and Cost: Building Blocks for Supply Analysis246 Questions

Exam 8: Output, Price, and Profit: the Importance of Marginal Analysis232 Questions

Exam 9: The Financial Markets and the Economy: the Tail That Wags the Dog225 Questions

Exam 10: The Firm and the Industry Under Perfect Competition219 Questions

Exam 11: The Case for Free Markets: the Price System251 Questions

Exam 12: Monopoly236 Questions

Exam 13: Between Competition and Monopoly248 Questions

Exam 14: Limiting Market Power: Antitrust and Regulation152 Questions

Exam 15: The Shortcomings of Free Markets210 Questions

Exam 16: The Economics of the Environment, and Natural Resources218 Questions

Exam 17: Taxation and Resource Allocation218 Questions

Exam 18: Pricing the Factors of Production230 Questions

Exam 19: Labor and Entrepreneurship: the Human Inputs267 Questions

Exam 20: Poverty, Inequality, and Discrimination167 Questions

Exam 21: An Introduction to Macroeconomics212 Questions

Exam 22: The Goals of Macroeconomic Policy212 Questions

Exam 23: Economic Growth: Theory and Policy226 Questions

Exam 24: Aggregate Demand and the Powerful Consumer216 Questions

Exam 25: Demand-Side Equilibrium: Unemployment or Inflation215 Questions

Exam 26: Bringing in the Supply Side: Unemployment and Inflation228 Questions

Exam 27: Managing Aggregate Demand: Fiscal Policy207 Questions

Exam 28: Money and the Banking System222 Questions

Exam 29: Monetary Policy: Conventional and Unconventional208 Questions

Exam 30: The Financial Crisis and the Great Recession64 Questions

Exam 31: The Debate Over Monetary and Fiscal Policy216 Questions

Exam 32: Budget Deficits in the Short and Long Run214 Questions

Exam 33: The Trade-Off Between Inflation and Unemployment218 Questions

Exam 34: International Trade and Comparative Advantage215 Questions

Exam 35: The International Monetary System: Order or Disorder216 Questions

Exam 36: Exchange Rates and the Macroeconomy215 Questions

Exam 37: Contemporary Issues in the Useconomy23 Questions

Select questions type

Anna is a tax accountant and she left her job with a large public accounting company to start her own accounting office.In doing this, Anna gave up her salary of $120,000 and took $60,000 out of her savings (which was earning a return of 5 percent) to fund her startup.Her first year, she had $180,000 in revenues and had $40,000 in operating expenses.Anna's tax accounting business earned economic profits of

(Multiple Choice)

4.9/5  (36)

(36)

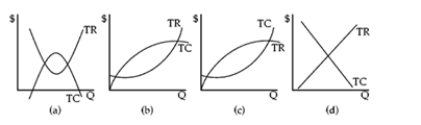

Figure 8-1  -Which graph in Figure 8-1 shows a typical firm's total revenue and total cost curves?

-Which graph in Figure 8-1 shows a typical firm's total revenue and total cost curves?

(Multiple Choice)

4.7/5 (30)

According to the text, when management selects a price or quantity, it also selects the other.Explain why this is true.

(Essay)

4.8/5 (33)

Profit can be maximized only where marginal revenue equals

(Multiple Choice)

4.8/5 (32)

A firm should keep producing output as long as the marginal profit is greater than zero, no matter how small it is.

(True/False)

4.9/5 (40)

Ski resorts have begun to offer activities in the summer, like music festivals and mountain biking, rather than closing down the facilities for the season.This a good decision for a ski resort when

(Multiple Choice)

4.9/5 (33)

The typical total profit graphical presentation is shown as

(Multiple Choice)

4.9/5 (38)

Sally leaves her $24,000 secretarial position with a company and invests her savings of $15,000 (on which she was earning 6 percent interest) in her own Ready Sec agency.After expenses, her net income was $28,900.Her economic profit was

(Multiple Choice)

4.7/5 (32)

Economists use a model that is a literal description of business' behavior.

(True/False)

4.8/5 (34)

If a firm's fixed cost (overhead) increases, what happens to its profit-maximizing price and output?

(Essay)

4.9/5 (40)

Thomas Edison once said that he began making real profit on light bulbs when he dumped his surplus on the European market at less than the "cost of production." From this we can deduce Edison

(Multiple Choice)

4.8/5 (28)

If the marginal profit of the next unit is negative, the firm should produce more output in order to generate greater profit.

(True/False)

4.8/5 (40)

Since the demand curve is downward sloping, the graph of total profits is also has a negative slope.

(True/False)

4.9/5 (43)

Total revenue is equal to quantity multiplied by average revenue.

(True/False)

4.9/5 (41)

A cellphone maker sells 6,000 units per month at $600 each.The firm is investigating whether a price cut to $500 is warranted.The firm's marginal cost of production of each phone is a constant $400 per unit.To maintain profits at their current level, quantity sold must increase to at least

(Multiple Choice)

4.8/5 (42)

The marginal cost of Alexa's Guide to Street People and Their Pets is constant at $5.Alexa sells 5,000 copies per year at $20 per copy.She would like to increase readership and hold total profit constant.If the price goes to $15, how many copies must she sell?

(Multiple Choice)

4.8/5 (35)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)