Exam 8: Output, Price, and Profit: the Importance of Marginal Analysis

Exam 1: What Is Economics254 Questions

Exam 2: The Economony: Myth and Reality184 Questions

Exam 3: The Fundamental Economic Problem: Scarcity and Choice278 Questions

Exam 4: Supply and Demand: an Initial Look297 Questions

Exam 5: Consumer Choice: Individual and Market Demand213 Questions

Exam 6: Demand and Elasticity247 Questions

Exam 7: Production, Inputs, and Cost: Building Blocks for Supply Analysis246 Questions

Exam 8: Output, Price, and Profit: the Importance of Marginal Analysis232 Questions

Exam 9: The Financial Markets and the Economy: the Tail That Wags the Dog225 Questions

Exam 10: The Firm and the Industry Under Perfect Competition219 Questions

Exam 11: The Case for Free Markets: the Price System251 Questions

Exam 12: Monopoly236 Questions

Exam 13: Between Competition and Monopoly248 Questions

Exam 14: Limiting Market Power: Antitrust and Regulation152 Questions

Exam 15: The Shortcomings of Free Markets210 Questions

Exam 16: The Economics of the Environment, and Natural Resources218 Questions

Exam 17: Taxation and Resource Allocation218 Questions

Exam 18: Pricing the Factors of Production230 Questions

Exam 19: Labor and Entrepreneurship: the Human Inputs267 Questions

Exam 20: Poverty, Inequality, and Discrimination167 Questions

Exam 21: An Introduction to Macroeconomics212 Questions

Exam 22: The Goals of Macroeconomic Policy212 Questions

Exam 23: Economic Growth: Theory and Policy226 Questions

Exam 24: Aggregate Demand and the Powerful Consumer216 Questions

Exam 25: Demand-Side Equilibrium: Unemployment or Inflation215 Questions

Exam 26: Bringing in the Supply Side: Unemployment and Inflation228 Questions

Exam 27: Managing Aggregate Demand: Fiscal Policy207 Questions

Exam 28: Money and the Banking System222 Questions

Exam 29: Monetary Policy: Conventional and Unconventional208 Questions

Exam 30: The Financial Crisis and the Great Recession64 Questions

Exam 31: The Debate Over Monetary and Fiscal Policy216 Questions

Exam 32: Budget Deficits in the Short and Long Run214 Questions

Exam 33: The Trade-Off Between Inflation and Unemployment218 Questions

Exam 34: International Trade and Comparative Advantage215 Questions

Exam 35: The International Monetary System: Order or Disorder216 Questions

Exam 36: Exchange Rates and the Macroeconomy215 Questions

Exam 37: Contemporary Issues in the Useconomy23 Questions

Select questions type

All business firms should consider their fixed costs in determining the prices they set.

(True/False)

4.8/5  (39)

(39)

In 1984, British Prime Minister Margaret Thatcher decided to shut down so-called uneconomic coal mines owned by the government.The National Union of Mineworkers protested, asserting that there was enough coal in the mines to continue current levels of production for years.Thatcher implicitly argued that her decision was economically sound because, at any practical level of output, for each "uneconomic" mine,

(Multiple Choice)

4.9/5 (38)

Assume that you have taken over management of a small concession stand on a local beach for the summer.Your main product is iced water, popular on hot days.You've been selling 400 cups per day at 50 cents each.The cups cost 5 cents each.One of your customers suggests that you cut the price to 40 cents to make more money.For the customer to be correct, how much must your sales increase?

(Essay)

4.9/5 (41)

If a firm's average cost is currently $100, and the marginal cost is $95, then the average cost is currently falling.

(True/False)

4.9/5 (36)

The average revenue curve can also be described as the demand curve.

(True/False)

4.8/5 (37)

If the price of a product is $10 per unit and the variable cost per unit is $5, the firm is making a profit.

(True/False)

4.8/5 (33)

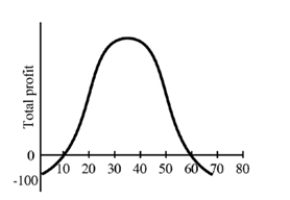

Figure 8-3  -Figure 8-3 shows a firm's total profit function.At an output of 40, the firm's total profit equals ____.

-Figure 8-3 shows a firm's total profit function.At an output of 40, the firm's total profit equals ____.

(Multiple Choice)

4.7/5 (37)

-The firm described in Table 8-1 has a fixed cost of ____ at its optimal level of output.

-The firm described in Table 8-1 has a fixed cost of ____ at its optimal level of output.

(Multiple Choice)

4.8/5 (39)

Most business people calculate marginal cost and marginal revenue to decide how much to produce.

(True/False)

4.7/5 (36)

The goal of the business firm is maximization of ____, and the goal of the consumer is maximization of ____.

(Multiple Choice)

4.8/5 (36)

If a firm has determined its optimal output level, where MR = MC, then price

(Multiple Choice)

4.7/5 (38)

Tour companies and cruise lines often offer last minute fares that are far below the prices paid by customers who have booked their trips far in advance.Use marginal analysis to explain this pricing tactic.

(Essay)

4.8/5 (38)

A firm is generally more interested in marginal profits than in total profits.

(True/False)

4.8/5 (40)

The rule of equating marginal benefit with marginal cost is a tool that can be applied to a wide variety of decisions, not just economics.

(True/False)

4.8/5 (43)

In reality, decisions made by firms may not always produce maximum total profit because some executives

(Multiple Choice)

4.7/5 (42)

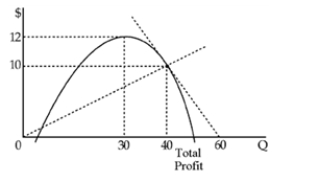

Figure 8-5  -In Figure 8-5, profits are maximized at output of

-In Figure 8-5, profits are maximized at output of

(Multiple Choice)

4.8/5 (43)

Explain the rules for finding maximum profit using total revenue and total cost and marginal revenue and marginal cost.

(Essay)

4.7/5 (30)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)