Exam 11: Flexible Budgets and Overhead Analysis

Exam 1: Introduction to Managerial Accounting64 Questions

Exam 2: Basic Managerial Accounting Concepts238 Questions

Exam 3: Cost Behavior231 Questions

Exam 4: Cost-Volume-Profit Analysis: a Managerial Planning Tool185 Questions

Exam 5: Job-Order Costing196 Questions

Exam 6: Process Costing177 Questions

Exam 7: Activity-Based Costing and Management178 Questions

Exam 8: Absorption and Variable Costing, and Inventory Management125 Questions

Exam 9: Profit Planning186 Questions

Exam 10: Standard Costing: a Managerial Control Tool180 Questions

Exam 11: Flexible Budgets and Overhead Analysis173 Questions

Exam 12: Performance Evaluation and Decentralization167 Questions

Exam 13: Short-Run Decision Making: Relevant Costing170 Questions

Exam 14: Capital Investment Decisions172 Questions

Exam 15: Statement of Cash Flows185 Questions

Exam 16: Financial Statement Analysis190 Questions

Select questions type

MATCHING

Match the following terms with the items below:

a.

(Actual hours -Standard hours)SVOR

b.

Prediction of what activity costs will be as activity output changes

c.

A measure of capacity utilization

d.

Actual variable overhead - (SVOR * Actual hours)

e.

Difference between the actual amount and the flexible budget amount

f.

A budget that specifies costs for a range of activity

g.

A budget for a particular level of activity

h.

Estimating activity output and then assessing the cost of resources to produce this output

i.

A report that compares actual with planned costs

j.

Difference between actual and budgeted fixed overhead

-Fixed overhead volume variance

(Short Answer)

4.7/5  (45)

(45)

Describe flexible budgeting, including the two types of flexible budgets.

(Essay)

4.8/5 (41)

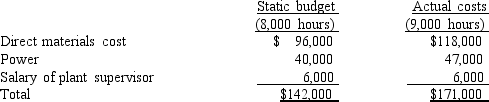

Figure 11-2.

Lawson, Inc. produces plastic grocery bags. Lawson has developed a static budget for the month of July based on 8,000 direct labor hours. During the quarter, the actual activity was 9,000 direct labor hours. Data for July are summarized as follows:

-Refer to Figure 11-2. What is the flexible budget variance for July?

-Refer to Figure 11-2. What is the flexible budget variance for July?

(Multiple Choice)

4.9/5 (38)

Price changes of variable overhead items are easily controlled by production supervisors.

(True/False)

4.8/5 (43)

Static budgets are the best benchmarks for preparing a performance report.

(True/False)

4.9/5 (40)

Activity flexible budgeting is the prediction of what activity costs will be as related output changes.

(True/False)

4.9/5 (41)

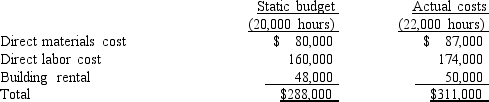

Figure 11-1.

Jason, Inc. produces leather purses. Jason has developed a static budget for the first quarter, based on 20,000 direct labor hours. During the quarter, the actual activity was 22,000 direct labor hours. Data for the first quarter are summarized as follows:

-Refer to Figure 11-1. Comparing the static budget to the actual outcomes, we can say the following:

-Refer to Figure 11-1. Comparing the static budget to the actual outcomes, we can say the following:

(Multiple Choice)

4.8/5 (48)

The ________________ budget is based on the actual level of activity.

(Short Answer)

4.7/5 (42)

Figure 11-6.

Kyle Company uses forklifts to move materials from the storage area to the production floor. There are five forklifts. They are fully used 20 hours per day (making 8 moves per hour). The company works 320 days per year, running two 7-hour shifts per day. Fork-lift operators work 1,800 hours per year and are paid an annual salary of $56,000.

Based on a recent study each forklift uses 0.45 gallons of fuel per move. The cost of fuel is $3.80 per gallon.

-Refer to Figure 11-6. Calculate the fuel budget for the year for moving materials.

(Multiple Choice)

4.8/5 (37)

MATCHING

Match the following terms with the items below:

a.

(Actual hours -Standard hours)SVOR

b.

Prediction of what activity costs will be as activity output changes

c.

A measure of capacity utilization

d.

Actual variable overhead - (SVOR * Actual hours)

e.

Difference between the actual amount and the flexible budget amount

f.

A budget that specifies costs for a range of activity

g.

A budget for a particular level of activity

h.

Estimating activity output and then assessing the cost of resources to produce this output

i.

A report that compares actual with planned costs

j.

Difference between actual and budgeted fixed overhead

-Variable overhead efficiency variance

(Short Answer)

4.9/5 (40)

Although general responsibility for the volume variance is usually assigned to the purchasing department, responsibility on occasion may be assigned to the production department.

(True/False)

4.9/5 (38)

If variable manufacturing overhead is applied based on direct labor hours and there is an unfavorable direct labor efficiency variance

(Multiple Choice)

4.9/5 (44)

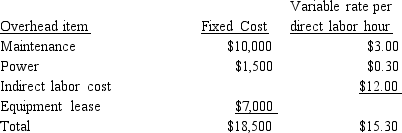

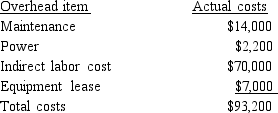

Figure 11-3.

Montgomery Company has developed the following flexible budget formulas for its four overhead items:

Montgomery normally produces 15,000 units (each unit requires 0.30 direct labor hours); however this year 19,000 units were produced with the following actual costs:

Montgomery normally produces 15,000 units (each unit requires 0.30 direct labor hours); however this year 19,000 units were produced with the following actual costs:

-Refer to Figure 11-3. Using an after-the-fact flexible budget, calculate the total budget variance.

-Refer to Figure 11-3. Using an after-the-fact flexible budget, calculate the total budget variance.

(Multiple Choice)

4.8/5 (44)

An activity-based budgeting system may help support continuous improvement and process management.

(True/False)

4.7/5 (36)

In budgeting at the activity level, the cost behavior of each activity is defined with respect to

(Multiple Choice)

4.9/5 (38)

Figure 11-6.

Kyle Company uses forklifts to move materials from the storage area to the production floor. There are five forklifts. They are fully used 20 hours per day (making 8 moves per hour). The company works 320 days per year, running two 7-hour shifts per day. Fork-lift operators work 1,800 hours per year and are paid an annual salary of $56,000.

Based on a recent study each forklift uses 0.45 gallons of fuel per move. The cost of fuel is $3.80 per gallon.

-Refer to Figure 11-6. Prepare a flexible budget formula for the moving materials activity.

(Multiple Choice)

4.8/5 (41)

Activity-based budgeting focuses on estimating the costs of activities rather than the costs of departments and plants.

(True/False)

4.8/5 (41)

For activity flexible budgeting, a cost formula is developed for each

(Multiple Choice)

4.9/5 (37)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)