Exam 11: Flexible Budgets and Overhead Analysis

Exam 1: Introduction to Managerial Accounting64 Questions

Exam 2: Basic Managerial Accounting Concepts238 Questions

Exam 3: Cost Behavior231 Questions

Exam 4: Cost-Volume-Profit Analysis: a Managerial Planning Tool185 Questions

Exam 5: Job-Order Costing196 Questions

Exam 6: Process Costing177 Questions

Exam 7: Activity-Based Costing and Management178 Questions

Exam 8: Absorption and Variable Costing, and Inventory Management125 Questions

Exam 9: Profit Planning186 Questions

Exam 10: Standard Costing: a Managerial Control Tool180 Questions

Exam 11: Flexible Budgets and Overhead Analysis173 Questions

Exam 12: Performance Evaluation and Decentralization167 Questions

Exam 13: Short-Run Decision Making: Relevant Costing170 Questions

Exam 14: Capital Investment Decisions172 Questions

Exam 15: Statement of Cash Flows185 Questions

Exam 16: Financial Statement Analysis190 Questions

Select questions type

In an activity framework, controlling costs is equivalent to managing activities.

(True/False)

4.9/5  (32)

(32)

Activity flexible budgeting provides a more accurate prediction of costs than a traditional flexible budgeting approach because

(Multiple Choice)

4.8/5 (25)

What is the fixed overhead volume variance? Suppose that the fixed overhead volume variance is unfavorable; what does that mean?

(Essay)

4.9/5 (42)

The _____________________ measures the aggregate effect of differences between the actual variable overhead rate and the standard variable overhead rate.

(Short Answer)

5.0/5 (32)

Which of the following relationships is valid concerning fixed overhead budgeted at the beginning of the year?

(Multiple Choice)

4.9/5 (40)

In an activity flexible budget, the fixed cost component typically corresponds to

(Multiple Choice)

4.8/5 (46)

An activity-based budgetary approach can be used to emphasize cost increases through the reduction of wasteful activities and improving the efficiency of necessary activities.

(True/False)

4.9/5 (41)

Because activities are what consume resources, activity-based budgeting may prove to be a much more powerful planning and control tool than the traditional approach.

(True/False)

4.9/5 (33)

Folson Company is planning to produce 4,250,000 speakers for the coming year. Actual production was 4,000,000 speakers. Each speaker requires 0.80 direct labor hours per unit. Predetermined overhead rates are calculated using expected production, measured in direct labor hours. The budgeted variable overhead for the coming year is $680,000. The actual variable overhead incurred was $714,000. The applied variable overhead for the year is

(Multiple Choice)

4.8/5 (45)

Markus, Inc. produces a specialized machine part used in forklifts. For last year's operations, the following data were gathered:  Markus employs a standard costing system. During the year, a variable overhead rate of $5.00 was used. The labor standard requires 0.50 hours per unit produced. The variable overhead spending and efficiency variances are, respectively

Markus employs a standard costing system. During the year, a variable overhead rate of $5.00 was used. The labor standard requires 0.50 hours per unit produced. The variable overhead spending and efficiency variances are, respectively

(Multiple Choice)

4.7/5 (32)

_______________________ is the difference between the actual variable overhead and applied variable overhead.

(Short Answer)

4.9/5 (43)

The ____________________ budget gives expected outcomes for a range of activity levels.

(Short Answer)

4.7/5 (37)

MATCHING

Match the following terms with the items below:

a.

(Actual hours -Standard hours)SVOR

b.

Prediction of what activity costs will be as activity output changes

c.

A measure of capacity utilization

d.

Actual variable overhead - (SVOR * Actual hours)

e.

Difference between the actual amount and the flexible budget amount

f.

A budget that specifies costs for a range of activity

g.

A budget for a particular level of activity

h.

Estimating activity output and then assessing the cost of resources to produce this output

i.

A report that compares actual with planned costs

j.

Difference between actual and budgeted fixed overhead

-Activity flexible budget

(Short Answer)

4.7/5 (28)

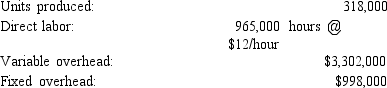

Figure 11-4.

Kris Company calculates its predetermined rates using practical volume, which is 325,000 units. The standard cost system allows 3 direct labor hours per unit produced. Overhead is applied using direct labor hours. The total budgeted overhead is $4,260,000, of which $994,000 is fixed overhead. The actual results for the year are as follows:

-Refer to Figure 11-4. Calculate the fixed overhead volume variance.

-Refer to Figure 11-4. Calculate the fixed overhead volume variance.

(Multiple Choice)

4.9/5 (35)

For a static activity budget in a company already using an ABC or ABM system, the activities within the organization must be identified.

(True/False)

4.9/5 (28)

MATCHING

Match the following terms with the items below:

a.

(Actual hours -Standard hours)SVOR

b.

Prediction of what activity costs will be as activity output changes

c.

A measure of capacity utilization

d.

Actual variable overhead - (SVOR * Actual hours)

e.

Difference between the actual amount and the flexible budget amount

f.

A budget that specifies costs for a range of activity

g.

A budget for a particular level of activity

h.

Estimating activity output and then assessing the cost of resources to produce this output

i.

A report that compares actual with planned costs

j.

Difference between actual and budgeted fixed overhead

-Performance report

(Short Answer)

4.9/5 (36)

Discuss the following statement: "As long as the total variable overhead variance is small, the managers can be assured that actual activity is proceeding as planned. No further action is necessary."

(Essay)

4.8/5 (45)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)