Exam 1: CPA Auditing and Attestation Exam

Exam 1: CPA Auditing and Attestation Exam1 k+ Questions

Select questions type

In auditing a manufacturing entity, which of the following procedures would an auditor least likely perform to determine whether slow-moving, defective, and obsolete items included in inventory are properly identified?

(Multiple Choice)

4.9/5  (37)

(37)

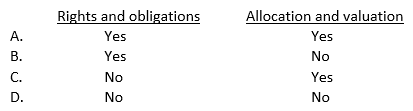

After making inquiries about credit granting policies, an auditor selects a sample of sales transactions and examines evidence of credit approval. This test of controls most likely supports management's financial statement assertion(s) of:

(Multiple Choice)

4.9/5 (35)

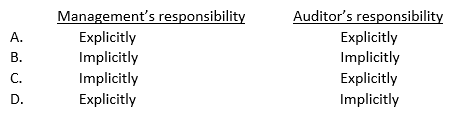

How are management's responsibility and the auditor's responsibility represented in the standard auditor's report?

(Multiple Choice)

4.8/5 (37)

Payroll Data Co. (PDC) processes payroll transactions for a retailer. Cook, CPA, is engaged to express an opinion on a description of PDC's internal controls placed in operation as of a specific date. These controls are relevant to the retailer's internal control, so Cook's report may be useful in providing the retailer's independent auditor with information necessary to plan a financial statement audit. Cook's report should:

(Multiple Choice)

4.8/5 (26)

Which of the following standards requires a critical review of the work done and the judgment exercised by those assisting in an audit at every level of supervision?

(Multiple Choice)

4.8/5 (35)

This question consists of an item pertaining to possible deficiencies in an accountant's review report. Jordan & Stone, CPAs, audited the financial statements of Tech Co., a nonissuer, for the year ended December 31, 20X1, and expressed an unqualified opinion. For the year ended December 31, 20X2, Tech issued comparative financial statements. Jordan & Stone reviewed Tech's 20X2 financial statements and Kent, an assistant on the engagement, drafted the accountants' review report below. Land, the engagement supervisor, decided not to reissue the prior year's auditors' report, but instructed Kent to include a separate paragraph in the current year's review report describing the responsibility assumed for the prior year's audited financial statements. This is an appropriate reporting procedure. Land reviewed Kent's draft and indicated in the Supervisor's Review Notes below that there were several deficiencies in Kent's draft. Accountant's Review Report We have reviewed and audited the accompanying balance sheets of Tech Co. as of December 31, 20X2 and 20X1, and the related statements of income, retained earnings, and cash flows for the years then ended, in accordance with Statements on Standards for Accounting and Review Services issued by the American Institute of Certified Public Accountants and generally accepted auditing standards. All information included in these financial statements is the representation of the management of Tech Co. A review consists principally of inquiries of company personnel and analytical procedures applied to financial data. It is substantially less in scope than an audit in accordance with generally accepted auditing standards, the objective of which is the expression of an opinion regarding the financial statements taken as a whole. Based on our review, we are not aware of any material modifications that should be made to the accompanying financial statements. Because of the inherent limitations of a review engagement, this report is intended for the information of management and should not be used for any other purpose. The financial statements for the year ended December 31, 20X1, were audited by us and our report was dated March 2, 20X2. We have no responsibility for updating that report for events and circumstances occurring after that date. Jordan and Stone, CPAs March 1, 20X3 Supervisor's Review Notes All the current-year basic financial statements are not properly identified in the first (introductory) paragraph.

(Multiple Choice)

4.8/5 (44)

As a result of sampling procedures applied as tests of controls, an auditor incorrectly assesses control risk lower than appropriate. The most likely Explanation: for this situation is that:

(Multiple Choice)

4.8/5 (32)

Ordinarily, the predecessor auditor permits the successor auditor to review the predecessor's audit documentation relating to:

(Multiple Choice)

4.9/5 (33)

When there has been a change in accounting principles, but the effect of the change on the comparability of the financial statements is not material, the auditor should:

(Multiple Choice)

4.8/5 (39)

To reduce the risks associated with accepting e-mail responses to requests for confirmation of accounts receivable, an auditor most likely would:

(Multiple Choice)

4.8/5 (35)

An auditor may report on condensed financial statements that are derived from complete audited financial statements if the:

(Multiple Choice)

4.9/5 (40)

This question presents independent factual situations an auditor might encounter in conducting an audit. List A represents the types of opinions the auditor ordinarily would issue. Select as the best answer for this item, the action the auditor normally would take. The types of opinions in List A may be selected once, more than once, or not at all. Assume: - The auditor is independent. - The auditor previously expressed an unqualified opinion on the prior year's financial statements. - Only single-year (not comparative) statements are presented for the current year. - The conditions for an unqualified opinion exist unless contradicted in the factual situations. - The conditions stated in the factual situations are material. - No report modifications are to be made except in response to the factual situation. Item to Be Answered Due to recurring operating losses and working capital deficiencies, an auditor has substantial doubt about an entity's ability to continue as a going concern for a reasonable period of time. However, the financial statement disclosures concerning these matters are adequate. List A Types of Options

(Multiple Choice)

4.8/5 (51)

Which of the following is an engagement attribute for an audit of an entity that processes most of its financial data in electronic form without any paper documentation?

(Multiple Choice)

4.7/5 (40)

An auditor testing long-term investments would ordinarily use analytical review as the primary audit procedure to ascertain the reasonableness of the:

(Multiple Choice)

4.7/5 (29)

If requested to perform a review engagement for a nonissuer in which an accountant has an immaterial direct financial interest, the accountant is:

(Multiple Choice)

4.9/5 (41)

In auditing the financial statements of Star Corp., Land discovered information leading Land to believe that Star's prior year's financial statements, which were audited by Tell, require substantial revisions. Under these circumstances, Land should:

(Multiple Choice)

5.0/5 (46)

An auditor issued an audit report that was dual dated for a subsequent event occurring after the original date of the auditor's report. The auditor's responsibility for events occurring subsequent to the original date was:

(Multiple Choice)

4.7/5 (32)

In an environment that is highly automated, an auditor determines that it is not possible to reduce detection risk solely by substantive tests of transactions. Under these circumstances, the auditor most likely would:

(Multiple Choice)

4.7/5 (31)

Analytical procedures performed during an audit indicate that accounts receivable doubled since the end of the prior year. However, the allowance for doubtful accounts as a percentage of accounts receivable remained about the same. Which of the following client Explanation: s would satisfy the auditor?

(Multiple Choice)

4.8/5 (36)

Which of the following combinations of procedures would an auditor most likely perform to obtain evidence about fixed asset additions?

(Multiple Choice)

4.8/5 (33)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)