Exam 1: CPA Auditing and Attestation Exam

Exam 1: CPA Auditing and Attestation Exam1 k+ Questions

Select questions type

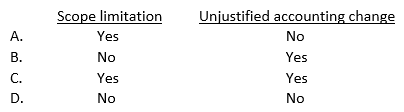

When a qualified opinion results from a limitation on the scope of the audit, the situation should be described in an explanatory paragraph:

(Multiple Choice)

4.8/5  (39)

(39)

Which of the following is not true regarding audit documentation for a specific audit?

(Multiple Choice)

4.9/5 (37)

After fieldwork audit procedures are completed, a partner of the CPA firm who has not been involved in the audit performs a second or wrap-up review of the audit documentation. This second review usually focuses on:

(Multiple Choice)

4.8/5 (29)

Negative confirmation of accounts receivable is less effective than positive confirmation of accounts receivable because:

(Multiple Choice)

4.8/5 (40)

An auditor may reasonably issue an "except for" qualified opinion for a(an):

(Multiple Choice)

4.8/5 (35)

Analytical procedures used in planning an audit should focus on:

(Multiple Choice)

4.8/5 (40)

This question consists of an item pertaining to possible deficiencies in an accountant's review report. Jordan & Stone, CPAs, audited the financial statements of Tech Co., a nonissuer, for the year ended December 31, 20X1, and expressed an unqualified opinion. For the year ended December 31, 20X2, Tech issued comparative financial statements. Jordan & Stone reviewed Tech's 20X2 financial statements and Kent, an assistant on the engagement, drafted the accountants' review report below. Land, the engagement supervisor, decided not to reissue the prior year's auditors' report, but instructed Kent to include a separate paragraph in the current year's review report describing the responsibility assumed for the prior year's audited financial statements. This is an appropriate reporting procedure. Land reviewed Kent's draft and indicated in the Supervisor's Review Notes below that there were several deficiencies in Kent's draft. Accountant's Review Report We have reviewed and audited the accompanying balance sheets of Tech Co. as of December 31, 20X2 and 20X1, and the related statements of income, retained earnings, and cash flows for the years then ended, in accordance with Statements on Standards for Accounting and Review Services issued by the American Institute of Certified Public Accountants and generally accepted auditing standards. All information included in these financial statements is the representation of the management of Tech Co. A review consists principally of inquiries of company personnel and analytical procedures applied to financial data. It is substantially less in scope than an audit in accordance with generally accepted auditing standards, the objective of which is the expression of an opinion regarding the financial statements taken as a whole. Based on our review, we are not aware of any material modifications that should be made to the accompanying financial statements. Because of the inherent limitations of a review engagement, this report is intended for the information of management and should not be used for any other purpose. The financial statements for the year ended December 31, 20X1, were audited by us and our report was dated March 2, 20X2. We have no responsibility for updating that report for events and circumstances occurring after that date. Jordan and Stone, CPAs March 1, 20X3 Supervisor's Review Notes There should be no reference to the prior year's audited financial statements in the first (introductory) paragraph.

(Multiple Choice)

4.8/5 (28)

When using classical variables sampling for estimation, an auditor normally evaluates the sampling results by calculating the possible error in either direction. This statistical concept is known as:

(Multiple Choice)

4.9/5 (51)

When performing an engagement to review a nonissuer's financial statements, an accountant most likely would:

(Multiple Choice)

4.9/5 (30)

This question consists of an item pertaining to possible deficiencies in an accountant's review report. Jordan & Stone, CPAs, audited the financial statements of Tech Co., a nonissuer, for the year ended December 31, 20X1, and expressed an unqualified opinion. For the year ended December 31, 20X2, Tech issued comparative financial statements. Jordan & Stone reviewed Tech's 20X2 financial statements and Kent, an assistant on the engagement, drafted the accountants' review report below. Land, the engagement supervisor, decided not to reissue the prior year's auditors' report, but instructed Kent to include a separate paragraph in the current year's review report describing the responsibility assumed for the prior year's audited financial statements. This is an appropriate reporting procedure. Land reviewed Kent's draft and indicated in the Supervisor's Review Notes below that there were several deficiencies in Kent's draft. Accountant's Review Report We have reviewed and audited the accompanying balance sheets of Tech Co. as of December 31, 20X2 and 20X1, and the related statements of income, retained earnings, and cash flows for the years then ended, in accordance with Statements on Standards for Accounting and Review Services issued by the American Institute of Certified Public Accountants and generally accepted auditing standards. All information included in these financial statements is the representation of the management of Tech Co. A review consists principally of inquiries of company personnel and analytical procedures applied to financial data. It is substantially less in scope than an audit in accordance with generally accepted auditing standards, the objective of which is the expression of an opinion regarding the financial statements taken as a whole. Based on our review, we are not aware of any material modifications that should be made to the accompanying financial statements. Because of the inherent limitations of a review engagement, this report is intended for the information of management and should not be used for any other purpose. The financial statements for the year ended December 31, 20X1, were audited by us and our report was dated March 2, 20X2. We have no responsibility for updating that report for events and circumstances occurring after that date. Jordan and Stone, CPAs March 1, 20X3 Supervisor's Review Notes There should be no reference to "updating the prior year's auditor's report for events and circumstances occurring after that date" in the fourth (separate) paragraph.

(Multiple Choice)

4.9/5 (42)

Statements on Standards for Accounting and Review Services establish standards and procedures for which of the following engagements?

(Multiple Choice)

4.9/5 (34)

An auditor vouched data for a sample of employees in a payroll register to approved clock card data to provide assurance that:

(Multiple Choice)

4.8/5 (35)

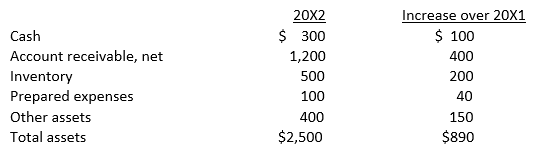

At December 31, 20X2, Curry Co. had the following balances in selected asset accounts:  Curry also had current liabilities of $1,000 at December 31, 20X2, and net credit sales of $7,200 for the year then ended. What was the average number of days to collect Curry's accounts receivable during 20X2?

Curry also had current liabilities of $1,000 at December 31, 20X2, and net credit sales of $7,200 for the year then ended. What was the average number of days to collect Curry's accounts receivable during 20X2?

(Multiple Choice)

4.7/5 (40)

For which of the following audit tests would a CPA most likely use attribute sampling?

(Multiple Choice)

4.9/5 (31)

Which of the following factors most likely would lead a CPA to conclude that a potential audit engagement should be rejected?

(Multiple Choice)

4.9/5 (31)

During a review of the financial statements of a nonissuer, an accountant becomes aware of a lack of adequate disclosure that is material to the financial statements. If management refuses to correct the financial statement presentations, the accountant should:

(Multiple Choice)

4.9/5 (33)

For an entity that does not receive governmental financial assistance, an auditor's standard report on financial statements generally would not refer to:

(Multiple Choice)

4.7/5 (40)

Which of the following components (elements) of an entity's internal control includes the development of personnel manuals documenting employee promotion and training policies?

(Multiple Choice)

4.8/5 (38)

Which of the following is not a control environment factor?

(Multiple Choice)

4.9/5 (36)

Which of the following questions would an auditor most likely include on an internal control questionnaire for notes payable?

(Multiple Choice)

4.9/5 (38)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)