Exam 1: CPA Auditing and Attestation Exam

Exam 1: CPA Auditing and Attestation Exam1 k+ Questions

Select questions type

An audit performed in accordance with OMB Circular A-133 will expand the auditor's responsibilities beyond generally accepted auditing standards. The auditor's expanded responsibilities include:

(Multiple Choice)

4.8/5  (39)

(39)

Unaudited financial statements for the prior year presented in comparative form with audited financial statements for the current year should be clearly marked to indicate their status and

(Multiple Choice)

4.8/5 (33)

Statements on Standards for Accounting and Review Services (SSARS) require an accountant to report when the accountant has:

(Multiple Choice)

4.8/5 (52)

This question consists of an item pertaining to possible deficiencies in an accountant's review report. Jordan & Stone, CPAs, audited the financial statements of Tech Co., a nonissuer, for the year ended December 31, 20X1, and expressed an unqualified opinion. For the year ended December 31, 20X2, Tech issued comparative financial statements. Jordan & Stone reviewed Tech's 20X2 financial statements and Kent, an assistant on the engagement, drafted the accountants' review report below. Land, the engagement supervisor, decided not to reissue the prior year's auditors' report, but instructed Kent to include a separate paragraph in the current year's review report describing the responsibility assumed for the prior year's audited financial statements. This is an appropriate reporting procedure. Land reviewed Kent's draft and indicated in the Supervisor's Review Notes below that there were several deficiencies in Kent's draft. Accountant's Review Report We have reviewed and audited the accompanying balance sheets of Tech Co. as of December 31, 20X2 and 20X1, and the related statements of income, retained earnings, and cash flows for the years then ended, in accordance with Statements on Standards for Accounting and Review Services issued by the American Institute of Certified Public Accountants and generally accepted auditing standards. All information included in these financial statements is the representation of the management of Tech Co. A review consists principally of inquiries of company personnel and analytical procedures applied to financial data. It is substantially less in scope than an audit in accordance with generally accepted auditing standards, the objective of which is the expression of an opinion regarding the financial statements taken as a whole. Based on our review, we are not aware of any material modifications that should be made to the accompanying financial statements. Because of the inherent limitations of a review engagement, this report is intended for the information of management and should not be used for any other purpose. The financial statements for the year ended December 31, 20X1, were audited by us and our report was dated March 2, 20X2. We have no responsibility for updating that report for events and circumstances occurring after that date. Jordan and Stone, CPAs March 1, 20X3 Supervisor's Review Notes There should be no reference to "material modifications" in the third paragraph.

(Multiple Choice)

4.8/5 (29)

As the acceptable level of detection risk decreases, an auditor may:

(Multiple Choice)

4.8/5 (41)

When an auditor tests the internal controls of a computerized accounting system, which of the following is true of the test data approach?

(Multiple Choice)

4.8/5 (35)

Which of the following procedures should an auditor generally perform regarding subsequent events?

(Multiple Choice)

4.9/5 (36)

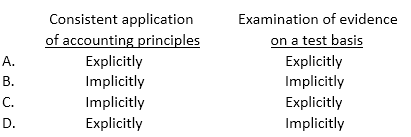

Does an auditor make the following representations explicitly or implicitly when issuing the standard auditor's report on comparative financial statements?

(Multiple Choice)

4.9/5 (42)

Which of the following statements is correct concerning an auditor's assessment of control risk?

(Multiple Choice)

4.8/5 (35)

Under properly designed internal control, the same employee most likely would match vendors' invoices with receiving reports and also:

(Multiple Choice)

4.9/5 (35)

Which of the following internal controls most likely would reduce the risk of diversion of customer receipts by an entity's employees?

(Multiple Choice)

4.9/5 (40)

An accountant performing a compilation or review of the financial statements of a nonissuer should:

(Multiple Choice)

5.0/5 (41)

Which of the following controls most likely would be effective in offsetting the tendency of sales personnel to maximize sales volume at the expense of high bad debt write-offs?

(Multiple Choice)

5.0/5 (30)

A weakness in internal control over recording retirements of equipment may cause an auditor to:

(Multiple Choice)

4.9/5 (34)

Which of the following circumstances would an auditor most likely consider a risk factor relating to misstatements arising from fraudulent financial reporting?

(Multiple Choice)

4.7/5 (41)

Sound internal control dictates that, immediately upon receiving checks from customers by mail, a responsible employee should:

(Multiple Choice)

4.8/5 (40)

Which of the following matters would an auditor most likely communicate to those charged with governance?

(Multiple Choice)

4.8/5 (27)

The usefulness of the standard bank confirmation request may be limited because the bank employee who completes the form may:

(Multiple Choice)

4.9/5 (38)

The in-charge auditor most likely would have a supervisory responsibility to explain to the staff assistants:

(Multiple Choice)

4.8/5 (41)

In which of the following situations would an auditor ordinarily choose between expressing a qualified opinion or an adverse opinion?

(Multiple Choice)

4.9/5 (33)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)