Exam 1: CPA Auditing and Attestation Exam

Exam 1: CPA Auditing and Attestation Exam1 k+ Questions

Select questions type

In obtaining an understanding of a manufacturing entity's internal control concerning inventory balances, an auditor most likely would:

(Multiple Choice)

4.9/5  (36)

(36)

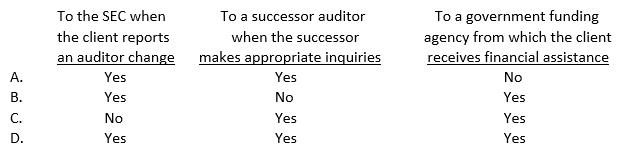

Disclosure of fraud to parties other than a client's senior management, those charged with governance, or its board of directors ordinarily is not part of an auditor's responsibility. However, to which of the following outside parties may a duty to disclose irregularities exist?

(Multiple Choice)

4.8/5 (46)

In developing an overall audit strategy, an auditor should consider:

(Multiple Choice)

4.8/5 (39)

Which of the following presumptions is correct about the reliability of audit evidence?

(Multiple Choice)

4.8/5 (39)

The management of Cain Company, a nonissuer, engaged Bell, CPA, to express an opinion on Cain's internal control. Bell's report described several material weaknesses and potential errors and irregularities that could occur. Subsequently, management included Bell's report in its annual report to the Board of Directors with a statement that the cost of correcting the weaknesses would exceed the benefits. Bell should:

(Multiple Choice)

4.8/5 (42)

When assessing an internal auditor's objectivity, an independent auditor should:

(Multiple Choice)

4.7/5 (28)

For an entity's financial statements to be presented fairly in conformity with generally accepted accounting principles, the principles selected should:

(Multiple Choice)

4.8/5 (42)

Prior to commencing fieldwork, an auditor usually discusses the general audit strategy with the client's management. Which of the following matters do the auditor and management agree upon at this time?

(Multiple Choice)

4.8/5 (40)

In the auditor's report, the principal auditor decides not to make reference to another CPA who audited a client's subsidiary. The principal auditor could justify this decision if, among other requirements, the principal auditor:

(Multiple Choice)

4.9/5 (45)

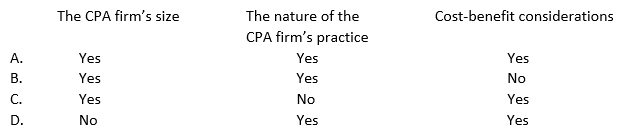

The nature and extent of a CPA firm's quality control policies and procedures depend on:

(Multiple Choice)

4.8/5 (36)

An auditor obtains knowledge about a new client's business and its industry to:

(Multiple Choice)

4.9/5 (34)

The objective of auditing procedures applied to segment information is to provide the auditor with a reasonable basis for concluding whether:

(Multiple Choice)

4.8/5 (33)

In reviewing the financial statements of a nonissuer, an accountant is required to modify the standard review report for which of the following matters?

(Multiple Choice)

4.8/5 (41)

An auditor is required to establish an understanding with a client regarding the services to be performed for each engagement. This understanding generally includes:

(Multiple Choice)

4.9/5 (45)

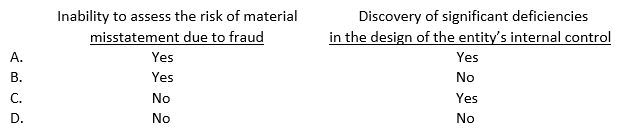

Which of the following statements is correct concerning significant deficiencies noted in an audit of a nonissuer?

(Multiple Choice)

4.8/5 (34)

An auditor who uses a transaction cycle approach to assessing control risk most likely would test control activities related to transactions involving the sale of goods to customers with the:

(Multiple Choice)

4.9/5 (34)

Which of the following evidence provides the least assurance of reliability?

(Multiple Choice)

4.8/5 (40)

In considering materiality for planning purposes, an auditor believes that misstatements aggregating $10,000 would have a material effect on an entity's income statement, but that misstatements would have to aggregate $20,000 to materially affect the balance sheet. Ordinarily, it would be appropriate to design auditing procedures that would be expected to detect misstatements that aggregate:

(Multiple Choice)

4.9/5 (37)

An internal auditor's work would most likely affect the nature, timing, and extent of an independent CPA's auditing procedures when the internal auditor's work relates to assertions about the:

(Multiple Choice)

4.8/5 (42)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)