Exam 1: CPA Auditing and Attestation Exam

Exam 1: CPA Auditing and Attestation Exam1 k+ Questions

Select questions type

For a nonissuer, a previously communicated significant deficiency that has not been corrected, ordinarily should be communicated again:

(Multiple Choice)

4.8/5  (41)

(41)

Accepting an engagement to compile a financial projection for a publicly held company most likely would be inappropriate if the projection were to be distributed to:

(Multiple Choice)

4.8/5 (49)

This question consists of an item pertaining to possible deficiencies in an accountant's review report. Jordan & Stone, CPAs, audited the financial statements of Tech Co., a nonissuer, for the year ended December 31, 20X1, and expressed an unqualified opinion. For the year ended December 31, 20X2, Tech issued comparative financial statements. Jordan & Stone reviewed Tech's 20X2 financial statements and Kent, an assistant on the engagement, drafted the accountants' review report below. Land, the engagement supervisor, decided not to reissue the prior year's auditors' report, but instructed Kent to include a separate paragraph in the current year's review report describing the responsibility assumed for the prior year's audited financial statements. This is an appropriate reporting procedure. Land reviewed Kent's draft and indicated in the Supervisor's Review Notes below that there were several deficiencies in Kent's draft. Accountant's Review Report We have reviewed and audited the accompanying balance sheets of Tech Co. as of December 31, 20X2 and 20X1, and the related statements of income, retained earnings, and cash flows for the years then ended, in accordance with Statements on Standards for Accounting and Review Services issued by the American Institute of Certified Public Accountants and generally accepted auditing standards. All information included in these financial statements is the representation of the management of Tech Co. A review consists principally of inquiries of company personnel and analytical procedures applied to financial data. It is substantially less in scope than an audit in accordance with generally accepted auditing standards, the objective of which is the expression of an opinion regarding the financial statements taken as a whole. Based on our review, we are not aware of any material modifications that should be made to the accompanying financial statements. Because of the inherent limitations of a review engagement, this report is intended for the information of management and should not be used for any other purpose. The financial statements for the year ended December 31, 20X1, were audited by us and our report was dated March 2, 20X2. We have no responsibility for updating that report for events and circumstances occurring after that date. Jordan and Stone, CPAs March 1, 20X3 Supervisor's Review Notes The accountant's review and audit responsibilities should follow management's responsibilities in the first (introductory) paragraph.

(Multiple Choice)

4.7/5 (32)

Which of the following information discovered during an audit most likely would raise a question concerning possible illegal acts?

(Multiple Choice)

4.9/5 (41)

Management of Eva Industries, an issuer as defined under the Sarbanes-Oxley Act, believes it has eliminated a material weakness previously noted in its assessment of internal control, and has hired Henna and Company, CPAs, to attest to the improvements in internal control. Which of the following is true of this engagement?

(Multiple Choice)

4.9/5 (29)

An auditor observes the mailing of monthly statements to a client's customers and reviews evidence of follow-up on errors reported by the customers. This test of controls most likely is performed to support management's financial statement assertions of:

(Multiple Choice)

4.9/5 (38)

Which of the following items does not pertain to the control environment?

(Multiple Choice)

4.8/5 (33)

Which of the following services performed by another entity would not be considered to be part of the client's information system?

(Multiple Choice)

4.8/5 (44)

"There have been no communications from regulatory agencies concerning noncompliance with, or deficiencies in, financial reporting practices that could have a material effect on the financial statements." The foregoing passage is most likely from a:

(Multiple Choice)

4.9/5 (37)

The most likely explanation why the auditor's examination cannot reasonably be expected to bring all illegal acts by the client to the auditor's attention is that:

(Multiple Choice)

4.9/5 (25)

Negative assurance may be expressed when an accountant is requested to report on the:

(Multiple Choice)

5.0/5 (33)

An auditor scans a client's investment records for the period just before and just after the year-end to determine that any transfers between categories of investments have been properly recorded. The primary purpose of this procedure is to obtain evidence about management's financial statement assertions of:

(Multiple Choice)

4.8/5 (33)

An accountant's standard report on a compilation of a projection should not include a:

(Multiple Choice)

4.9/5 (29)

Which of the following procedures is not usually performed by the accountant during a review engagement of a nonissuer?

(Multiple Choice)

4.9/5 (31)

This question consists of an item pertaining to possible deficiencies in an accountant's review report. Jordan & Stone, CPAs, audited the financial statements of Tech Co., a nonissuer, for the year ended December 31, 20X1, and expressed an unqualified opinion. For the year ended December 31, 20X2, Tech issued comparative financial statements. Jordan & Stone reviewed Tech's 20X2 financial statements and Kent, an assistant on the engagement, drafted the accountants' review report below. Land, the engagement supervisor, decided not to reissue the prior year's auditors' report, but instructed Kent to include a separate paragraph in the current year's review report describing the responsibility assumed for the prior year's audited financial statements. This is an appropriate reporting procedure. Land reviewed Kent's draft and indicated in the Supervisor's Review Notes below that there were several deficiencies in Kent's draft. Accountant's Review Report We have reviewed and audited the accompanying balance sheets of Tech Co. as of December 31, 20X2 and 20X1, and the related statements of income, retained earnings, and cash flows for the years then ended, in accordance with Statements on Standards for Accounting and Review Services issued by the American Institute of Certified Public Accountants and generally accepted auditing standards. All information included in these financial statements is the representation of the management of Tech Co. A review consists principally of inquiries of company personnel and analytical procedures applied to financial data. It is substantially less in scope than an audit in accordance with generally accepted auditing standards, the objective of which is the expression of an opinion regarding the financial statements taken as a whole. Based on our review, we are not aware of any material modifications that should be made to the accompanying financial statements. Because of the inherent limitations of a review engagement, this report is intended for the information of management and should not be used for any other purpose. The financial statements for the year ended December 31, 20X1, were audited by us and our report was dated March 2, 20X2. We have no responsibility for updating that report for events and circumstances occurring after that date. Jordan and Stone, CPAs March 1, 20X3 Supervisor's Review Notes There should be a statement that no opinion is expressed on the current year's financial statements in the second (scope) paragraph.

(Multiple Choice)

4.7/5 (36)

Digit Co. uses the FIFO method of costing for its international subsidiary's inventory and LIFO for its domestic inventory. Under these circumstances, the auditor's report on Digit's financial statements should express an:

(Multiple Choice)

4.8/5 (33)

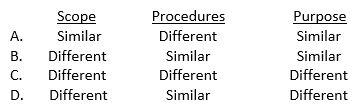

How do the scope, procedures, and purpose of an engagement to express a separate opinion on a nonissuer's internal control compare to those for obtaining an understanding of internal control and assessing control risk as part of an audit?

(Multiple Choice)

4.8/5 (26)

Snow, CPA, was engaged by Master Co., a nonissuer, to examine and report on management's written assertion about the effectiveness of Master's internal control over financial reporting. Snow's report should state that:

(Multiple Choice)

4.9/5 (33)

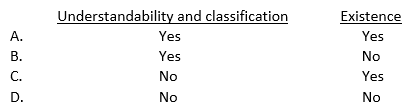

To which of the following matters would materiality limits not apply when obtaining written client representations?

(Multiple Choice)

4.8/5 (42)

In which of the following circumstances would an auditor most likely add an explanatory paragraph to the standard report while not affecting the auditor's unqualified opinion?

(Multiple Choice)

4.7/5 (35)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)