Exam 17: Business Tax Credits and the Alternative Minimum Tax

Exam 1: Introduction to Taxation98 Questions

Exam 2: Working With the Tax Law102 Questions

Exam 3: Taxes on the Financial Statements68 Questions

Exam 4: Gross Income96 Questions

Exam 5: Business Deductions208 Questions

Exam 6: Losses and Loss Limitations185 Questions

Exam 7: Property Transactions: Basis, Gain and Loss, and Nontaxable Exchanges118 Questions

Exam 8: Property Transactions: Capital Gains and Losses109 Questions

Exam 9: Individuals As the Taxpayer105 Questions

Exam 10: Individuals: Income, Deductions, and Credits119 Questions

Exam 11: Individuals As Employees and Proprietors131 Questions

Exam 12: Corporations: Organization, Capital Structure, and Operating Rules128 Questions

Exam 13: Corporations: Earnings and Profits and Distributions125 Questions

Exam 14: Partnerships and Limited Liability Entities122 Questions

Exam 15: S Corporations118 Questions

Exam 16: Multijurisdictional Taxation145 Questions

Exam 17: Business Tax Credits and the Alternative Minimum Tax132 Questions

Exam 18: Comparative Forms of Doing Business97 Questions

Select questions type

How can interest on a private activity bond issued in 2013 result in both an AMT adjustment that decreases AMTI and an AMT preference that increases AMTI?

(Essay)

4.9/5  (32)

(32)

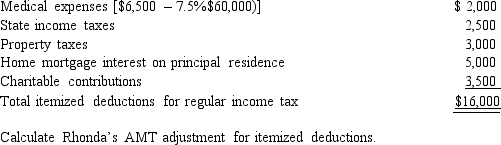

In calculating her taxable income, Rhonda, who is age 45, claims the following itemized deductions.

(Essay)

4.8/5 (27)

Which of the following would not cause an individual taxpayer's AMTI to increase in the current year?

(Multiple Choice)

4.8/5 (34)

How can the positive AMT adjustment for research and experimental expenditures be avoided?

(Essay)

4.9/5 (40)

AGI is used as the base for application of percentage limitations i.e., 20%, 30%, 50%) that apply to the charitable contribution deduction for regular income tax purposes.Modified AGI is used as the base for application of percentage limitations that apply to the charitable contribution deduction for AMT purposes.

(True/False)

4.9/5 (36)

The required adjustment for AMT purposes for pollution control facilities placed in service this year is equal to the difference between the amortization deduction allowed for regular income tax purposes and the depreciation deduction computed under ADS.

(True/False)

4.9/5 (34)

A U.S.taxpayer may take a current FTC equal to the greater of the FTC limit or the actual foreign taxes direct or indirect) paid or accrued.

(True/False)

4.8/5 (46)

The sale of business property could result in an AMT adjustment.

(True/False)

5.0/5 (34)

Dale owns and operates Dale's Emporium as a sole proprietorship.On January 30, 2004, Dale's Emporium acquired a warehouse for $100,000.For regular income tax purposes in 2018, depreciation was deducted under MACRS using a 2.564% rate.Determine the AMT adjustment for depreciation and indicate whether it is positive or negative.

(Multiple Choice)

4.9/5 (28)

Some or all) of the tax credit for rehabilitation expenditures will have to be recaptured if the rehabilitated property is disposed of prematurely or if it ceases to be qualifying property.

(True/False)

4.9/5 (39)

Durell's sole proprietorship builds residential housing.The business is eligible to use the completed contract method for regular income tax purposes.What can Durell do to minimize his AMT?

(Essay)

4.8/5 (35)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)