Exam 3: Partially Owned Created Subsidiaries & Variable Interest Entities

Exam 1: Wholly Owned Subsidiaries: at Date of Creation87 Questions

Exam 2: Wholly Owned Subsidiaries: Postcreation Periods110 Questions

Exam 3: Partially Owned Created Subsidiaries & Variable Interest Entities138 Questions

Exam 4: Introduction to Business Combinations105 Questions

Exam 5: The Purchase Method: at Date of Acquisition-100 Ownership135 Questions

Exam 6: The Purchase Method: Postacquisition Periods and Partial Ownerships74 Questions

Exam 7: New Basis of Accounting52 Questions

Exam 8: Introduction to Intercompany Transactions42 Questions

Exam 9: Intercompany Inventory Transfers66 Questions

Exam 10: Intercompany Fixed Asset Transfers & Bond Holdings31 Questions

Exam 11: Changes in a Parents Ownership Interest, Statement of Cash Flows, & Earnings Per Share86 Questions

Exam 12: Reporting Segment and Related Information90 Questions

Exam 13: International Accounting Standards & Translating Foreign Currency Transactions103 Questions

Exam 14: Using Derivatives to Manage Foreign Currency Exposures256 Questions

Exam 15: Translating Foreign Currency Statements: The Current Rate Method99 Questions

Exam 16: Translating Foreign Currency Statements: The Temporal Method and the Functional Currency Concept231 Questions

Exam 17: Interim Period Reporting49 Questions

Exam 18: Securities and Exchange Commission Reporting55 Questions

Exam 19: Bankruptcy Reorganizations and Liquidations51 Questions

Exam 20: Partnerships: Formation and Operation45 Questions

Exam 21: Partnerships: Changes in Ownership37 Questions

Exam 22: Partnerships: Liquidations35 Questions

Exam 23: Estates and Trusts40 Questions

Exam 24: Governmental Accounting: Basic Principles and the General Fund138 Questions

Exam 25: Governmental Accounting: The Special-Purpose Funds and Special General Ledger232 Questions

Exam 26: Not-For-Profit Organizations: Introduction and Private Npos218 Questions

Select questions type

A concept of viewing the noncontrolling interest that assumes that a new reporting entity results from the consolidation process is the _________________________ concept.

(Short Answer)

4.7/5  (43)

(43)

_____ Regarding the preparation of a consolidated tax return, which of the following statements is false?

(Multiple Choice)

4.8/5 (46)

If Entity A will absorb a majority of a VIE's expected losses and Entity B will receive a majority of that VIE's expected residual returns, both entities must consolidate the VIE.

(True/False)

4.8/5 (30)

_____Which of the following statements is false concerning the parent company concept?

(Multiple Choice)

4.8/5 (31)

The rationale underlying the parent company concept is that the reporting entity does not change as a result of the consolidation process.

(True/False)

4.8/5 (43)

_____ For reporting earnings of subsidiaries by parent companies, the Internal Revenue Code specifies, for most situations, the use of the

(Multiple Choice)

4.9/5 (34)

When a partially owned created subsidiary reports profits, the amount reported for consolidated net income would be the highest under which of the following methods?

(Multiple Choice)

4.8/5 (39)

The "dividend received deduction" is 100% if the subsidiary is 100% owned.

(True/False)

4.9/5 (35)

Under the economic unit concept, the interest of the noncontrolling shareholders is considered to be an equity interest of the consolidated reporting entity.

(True/False)

4.8/5 (45)

matching

based on the information given.

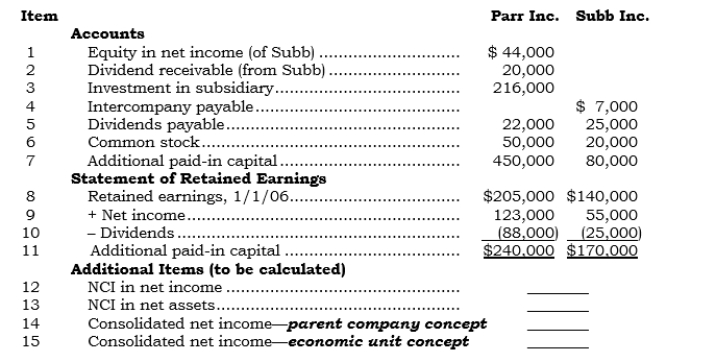

The following (a) seven account balances and (b) statements of retained earnings were obtained from the separate company statements of Parr Inc. and its 80%-owned created sub-sidiary, Subb Inc. (Parr's only subsidiary), at the end of 2006:

When Subb was created (in 2004, 20% of the common shares it issued were sold to private investors.

Requirement 1:

How is each of the first 11 preceding items reported in Parr's 2006 consolidated statements? Use the following list of possible answer codes in the answer columns:

-_____(item 10)

When Subb was created (in 2004, 20% of the common shares it issued were sold to private investors.

Requirement 1:

How is each of the first 11 preceding items reported in Parr's 2006 consolidated statements? Use the following list of possible answer codes in the answer columns:

-_____(item 10)

(Multiple Choice)

4.8/5 (35)

A manner of consolidation in which the noncontrolling interest is not presented in the consolidated statements is called _________________________________.

(Short Answer)

4.8/5 (42)

_____ Sixx is an 80%-owned domestic subsidiary of Pixx. For 2006, Sixx had $250,000 of pretax income and $150,000 of net income. On 12/31/06, Sixx paid a $100,000 dividend. The remaining $50,000 of net income is expected to be invested indefinitely. The tax rate is 40%. For 2006, Pixx should record income taxes relating to Sixx of:

(Multiple Choice)

4.9/5 (52)

Under the economic unit concept, the NCI in the subsidiary's net assets is presented as part of consolidated stockholders' equity.

(True/False)

4.9/5 (38)

_____ For financial reporting purposes, parent companies must provide income taxes on their share of their domestic subsidiaries' current earnings

(Multiple Choice)

4.8/5 (41)

A loan guarantee to a VIE's lenders could be a potential variable interest.

(True/False)

4.9/5 (29)

_____ Prell's 100%-owned domestic subsidiary has filed for bankruptcy protection. How should Prell value its investment in its unconsolidated statements if Prell cannot exercise significant influence?

(Multiple Choice)

4.8/5 (43)

A provision of the U.S. tax code that allows dividend income from a domestic subsidiary to not be taxed at the parent level is the election to file a(n) _____________________________________________.

(Short Answer)

4.9/5 (25)

FIN 46 allows an exception to consolidation for _____________________________ .

(Short Answer)

4.9/5 (37)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)