Exam 13: Risk and the Pricing of Options

Exam 1: Corporate Finance and the Financial Manager91 Questions

Exam 2: Introduction to Financial Statement Analysis122 Questions

Exam 3: The Valuation Principle: the Foundation of Financial Decision Making120 Questions

Exam 4: The Time Value of Money101 Questions

Exam 5: Interest Rates118 Questions

Exam 6: Bonds122 Questions

Exam 7: Valuing Stocks122 Questions

Exam 8: Investment Decision Rules137 Questions

Exam 9: Fundamentals of Capital Budgeting107 Questions

Exam 10: Risk and Return in Capital Markets101 Questions

Exam 11: Systematic Risk and the Equity Risk Premium102 Questions

Exam 12: Determining the Cost of Capital106 Questions

Exam 13: Risk and the Pricing of Options112 Questions

Exam 14: Raising Equity Capital104 Questions

Exam 15: Debt Financing109 Questions

Exam 16: Capital Structure113 Questions

Exam 17: Payout Policy101 Questions

Exam 18: Financial Modelling and Pro Forma Analysis124 Questions

Exam 19: Working Capital Management122 Questions

Exam 20: Short Term Financial Planning105 Questions

Exam 21: Risk Management108 Questions

Exam 22: International Corporate Finance108 Questions

Exam 23: Leasing86 Questions

Exam 24: Mergers and Acquisitions81 Questions

Exam 25: Corporate Governance52 Questions

Select questions type

Suppose a stock is currently trading for $23,and in one period it will either increase to $30 or decrease to $20.If the one-period risk-free rate is 5%,what is the price of a European call option that expires in one period and has an exercise price of $25?

(Multiple Choice)

4.8/5  (39)

(39)

Using an option to reduce the risk of a portfolio is called ________,while using options to bet on the direction of the market or an asset is called ________.

(Multiple Choice)

4.9/5 (40)

The value of a call option ________ with the risk-free rate,and the value of a put option ________ with the risk-free rate.

(Multiple Choice)

4.9/5 (48)

A one-year European call option on ABX corporation with a strike price of $50 is currently trading for $4.30,and a one-year European put option on ABX with the same strike price is currently trading for $1.47.If the stock pays no dividends and the risk free rate is 4% per year,what is the current price of ABX stock?

(Multiple Choice)

4.9/5 (40)

The price of a European put option on Scotiabank stock with one year to expiry is trading at $2.25,and the price of a European call option is trading at $1.60.If the exercise price of the options is $45,and the risk-free rate is 5%,what must be the current price of Scotiabank stock?

(Multiple Choice)

4.8/5 (32)

________ options allow the holder to exercise the option on any date up to and including the expiration date.

(Multiple Choice)

4.8/5 (37)

The value of an otherwise identical call option is ________ if the stock price is ________.

(Multiple Choice)

4.8/5 (27)

Hedging is accomplished by holding contracts or securities whose payoffs are positively correlated with some risk exposure that already exists.

(True/False)

4.9/5 (32)

A put option on a stock has an exercise price of $31.If the stock price at expiration is $29.45,what is the option payoff for a long put position?

(Multiple Choice)

4.8/5 (31)

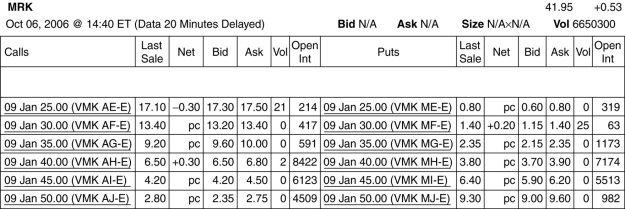

Use the table for the question(s) below.

Consider the following information on options from the CBOE for Merck:

-Assume you want to sell 20 call option contracts with an exercise price closest to being at-the-money and that expires January 2011.The current price that you would receive for such a contract is:

-Assume you want to sell 20 call option contracts with an exercise price closest to being at-the-money and that expires January 2011.The current price that you would receive for such a contract is:

(Multiple Choice)

4.9/5 (34)

The price at which the holder of an option buys or sells a share of stock when the option is exercised is called the ________ price.

(Multiple Choice)

4.8/5 (34)

Debt holders can be thought as owning the firm but having ________ a call option on the assets of the firm with a strike price equal to ________.

(Multiple Choice)

4.8/5 (42)

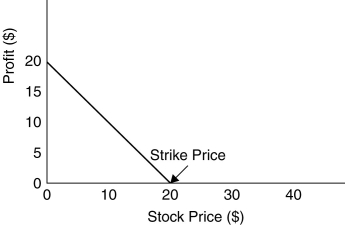

Use the figure for the question(s) below.

-What is the long position of an options contract?

-What is the long position of an options contract?

(Essay)

4.7/5 (42)

The price of a European call option on RBC stock with an exercise price of $85 and one year to expiry is trading at $3.15.The current price of the stock is $81.25,and the risk-free rate is 2.5%.With no arbitrage,what must be the price of a European put on RBC with an exercise price of $85?

(Multiple Choice)

4.9/5 (41)

The Black-Scholes formula gives the price of an American call option.

(True/False)

4.8/5 (32)

Consider the following equation: C = P + S - PV(K)- PV(Div)

In this equation,what does the term K represent?

(Multiple Choice)

4.8/5 (19)

Suppose a stock is currently trading for $35,and in one period it will either increase to $38 or decrease to $33.If the one-period risk-free rate is 6%,what is the price of a European put option that expires in one period and has an exercise price of $36?

(Multiple Choice)

4.8/5 (33)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)