Exam 15: Market Risk

Exam 1: Why Are Financial Institutions Special90 Questions

Exam 2: Deposit-Taking Institutions43 Questions

Exam 3: Finance Companies71 Questions

Exam 4: Securities, Brokerage, and Investment Banking91 Questions

Exam 5: Mutual Funds, Hedge Funds, and Pension Funds61 Questions

Exam 6: Insurance Companies80 Questions

Exam 7: Risks of Financial Institutions110 Questions

Exam 8: Interest Rate Risk I110 Questions

Exam 9: Interest Rate Risk II116 Questions

Exam 10: Credit Risk: Individual Loans112 Questions

Exam 11: Credit Risk: Loan Portfolio and Concentration Risk51 Questions

Exam 12: Liquidity Risk85 Questions

Exam 13: Foreign Exchange Risk87 Questions

Exam 14: Sovereign Risk89 Questions

Exam 15: Market Risk95 Questions

Exam 16: Off-Balance-Sheet Risk101 Questions

Exam 17: Technology and Other Operational Risks107 Questions

Exam 18: Liability and Liquidity Management38 Questions

Exam 19: Deposit Insurance and Other Liability Guarantees54 Questions

Exam 20: Capital Adequacy102 Questions

Exam 21: Product and Geographic Expansion114 Questions

Exam 22: Futures and Forwards234 Questions

Exam 23: Options, Caps, Floors, and Collars113 Questions

Exam 24: Swaps95 Questions

Exam 25: Loan Sales83 Questions

Exam 26: Securitization Index98 Questions

Select questions type

The earnings at risk for an FI is a function of

Free

(Multiple Choice)

5.0/5  (37)

(37)

Correct Answer: Verified

Verified

E

Income from trading activities of FIs is less important today than the traditional activities of banks.

Free

(True/False)

4.9/5 (38)

Correct Answer:Verified

False

The Volker Rule is intended to reduce market risk at U.S. deposit-taking institutions.

Free

(True/False)

4.8/5 (22)

Correct Answer:Verified

True

If an FIs trading portfolio of stock is not well-diversified, the additional risk that must be taken into account is

(Multiple Choice)

4.8/5 (33)

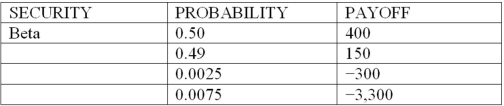

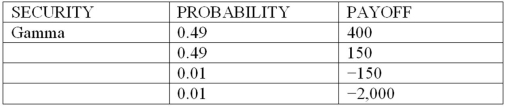

Consider the following discrete probability distributions of payoffs for 3 securities that are held in a DI's trading portfolio (payoff amounts shown are in $millions):

What is the one-day, 99% confidence level, value at risk (VAR) of securities Alpha and Beta, respectively (in millions)?

What is the one-day, 99% confidence level, value at risk (VAR) of securities Alpha and Beta, respectively (in millions)?

(Multiple Choice)

4.8/5 (35)

In the BIS standardized framework model, the general market risk weights reflect the product of the modified durations and interest rate shocks.

(True/False)

4.8/5 (34)

For situations in which probability distributions exhibit fat tail losses, expected shortfall (ES) may look relatively small, but value at risk (VaR) may be very large.

(True/False)

4.9/5 (35)

As securitization of assets continues to expand, the management of market risk will become more important to FIs.

(True/False)

5.0/5 (38)

A major weakness of the Risk Metrics Model is the need to assume a symmetric or normal distribution of asset returns.

(True/False)

4.8/5 (31)

Sumitomo Bank's risk manager has estimated that the VaRs of two of its major assets in its trading portfolio, foreign exchange and bonds, are -$150,000 and -$250,000, respectively. What is the total VaR of Sumitomo's trading portfolio if the correlation among assets is assumed to be -1.0?

(Multiple Choice)

4.8/5 (31)

In the BIS framework, vertical offsets are charges that reflect the modified duration and interest rate shocks for each maturity.

(True/False)

4.8/5 (36)

The mean change in the value of a portfolio of trading assets has been estimated to be 0 with a standard deviation of 20 percent. Yield changes are assumed to be normally distributed. What is the maximum yield change expected if a 90 percent confidence (one-tailed) limit is used?

(Multiple Choice)

4.9/5 (36)

Conceptually, an FI's trading portfolio can be differentiated from its investment portfolio by

(Multiple Choice)

4.8/5 (39)

Which of the following is a method that may overcome weaknesses in the historic or back simulation model?

(Multiple Choice)

4.9/5 (34)

The VaR of a bank's trading portfolio has been estimated at $5,000. It is assumed that the daily earnings are independently and normally distributed. What is the 20-day VaR?

(Multiple Choice)

4.8/5 (23)

The VaR of a portfolio of assets is simply the weighted average of each individual assets' VaR.

(True/False)

4.9/5 (32)

Market value at risk (VaR) is defined as the daily value at risk (VaR) times the number of days (N).

(True/False)

4.7/5 (34)

Monte-Carlo simulation is a tool for considering portfolio valuation under all possible combinations of factors that determine a security's value.

(True/False)

4.8/5 (34)

In the Risk Metrics model, value at risk (VAR) is calculated as

(Multiple Choice)

4.8/5 (23)

Deposit-taking institutions operating in the U.S. are prohibited from proprietary trading by the Volker Rule.

(True/False)

4.8/5 (30)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)