Exam 14: Interest Rate and Currency Swaps

Exam 1: International Monetary System100 Questions

Exam 2: Globalization and the Multinational Firm100 Questions

Exam 3: Balance of Payments97 Questions

Exam 4: Corporate Governance Around the World100 Questions

Exam 5: The Market for Foreign Exchange100 Questions

Exam 6: International Parity Relationships and Forecasting Foreign Exchange Rates85 Questions

Exam 7: Futures and Options on Foreign Exchange94 Questions

Exam 8: Management of Transaction Exposure100 Questions

Exam 9: Management of Economic Exposure100 Questions

Exam 10: Management of Translation Exposure81 Questions

Exam 11: International Banking and Money Market100 Questions

Exam 12: International Bond Market100 Questions

Exam 13: International Equity Markets100 Questions

Exam 14: Interest Rate and Currency Swaps100 Questions

Exam 15: International Portfolio Investment100 Questions

Exam 16: Foreign Direct Investment and Cross-Border Acquisitions100 Questions

Exam 17: International Capital Structure and the Cost of Capital100 Questions

Exam 18: International Capital Budgeting99 Questions

Exam 19: Multinational Cash Management82 Questions

Exam 20: International Trade Finance100 Questions

Exam 21: International Tax Environment and Transfer Pricing98 Questions

Select questions type

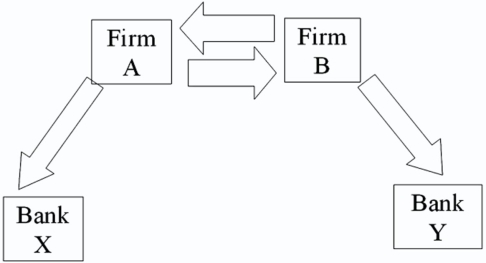

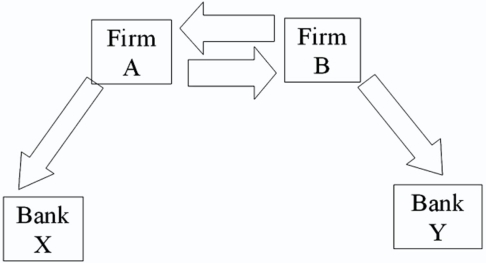

Consider the situation of firm A and firm B.The current exchange rate is $1.50/€.Firm A is a U.S.MNC and wants to borrow €40 million for 2 years.Firm B is a French MNC and wants to borrow $60 million for 2 years.Their borrowing opportunities are as shown; both firms have AAA credit ratings.

\ A \ 7\% 6\% B \8 \% 5\% Explain how firm A could use the forward exchange markets to redenominate a 2-year $60m 7 percent USD loan into a 2-year euro denominated loan.

(Essay)

4.9/5  (31)

(31)

Suppose the quote for a five-year swap with semiannual payments is 8.50-8.60 percent.This means

(Multiple Choice)

4.8/5 (28)

Consider the situation of firm A and firm B.The current exchange rate is $2.00/£ Firm A is a U.S.MNC and wants to borrow £30 million for 2 years.Firm B is a British MNC and wants to borrow $60 million for 2 years.Their borrowing opportunities are as shown,both firms have AAA credit ratings.

\ £ A \ 6\% £5\% B \7 \% £4\% The IRP 1-year and 2-year forward exchange rates are ($ ∣ £)= = ($ ∣ £)= = USD pounds

Bid Ask Bid Ask 6\% 6.1\% 4\% 4.1\% Devise a direct swap for A and B that has no swap bank.Show their external borrowing.Answer the problem in the template provided

(Essay)

4.8/5 (39)

Consider the situation of firm A and firm B.The current exchange rate is $2.00/£ Firm A is a U.S.MNC and wants to borrow £30 million for 2 years.Firm B is a British MNC and wants to borrow $60 million for 2 years.Their borrowing opportunities are as shown,both firms have AAA credit ratings.

\ £ A \ 6\% £5\% B \7 \% £4\% Devise a direct swap for A and B that has no swap bank.Show their external borrowing.

(Essay)

4.8/5 (43)

Consider the situation of firm A and firm B.The current exchange rate is $1.50/€.Firm A is a U.S.MNC and wants to borrow €40 million for 2 years.Firm B is a French MNC and wants to borrow $60 million for 2 years.Their borrowing opportunities are as shown; both firms have AAA credit ratings.

\ A \ 7\% 6\% B \8 \% 5\% Explain how firm B could use the forward exchange markets to redenominate a 2-year €40m 5 percent euro loan into a 2-year USD-denominated loan.

(Essay)

4.8/5 (36)

Consider the situation of firm A and firm B.The current exchange rate is $1.50/€.Firm A is a U.S.MNC and wants to borrow €40 million for 2 years.Firm B is a French MNC and wants to borrow $60 million for 2 years.Their borrowing opportunities are as shown; both firms have AAA credit ratings.

\ A \ 7\% 6\% B \8 \% 5\% If firm A could use the forward exchange markets to redenominate a 2-year $60m 7 percent USD loan into a 2-year euro denominated loan,what would be the interest rate?

(Essay)

5.0/5 (35)

Consider the situation of firm A and firm B.The current exchange rate is $2.00/£ Firm A is a U.S.MNC and wants to borrow £30 million for 2 years.Firm B is a British MNC and wants to borrow $60 million for 2 years.Their borrowing opportunities are as shown,both firms have AAA credit ratings.

\ £ A \ 6\% £5\% B \7 \% £4\% Explain how firm A could use the forward exchange markets to redenominate a 2-year $60m 6 percent USD loan into a 2-year pound denominated loan.

(Essay)

4.8/5 (32)

In an efficient market without barriers to capital flows,the cost-savings argument of the QSD is difficult to accept,because

(Multiple Choice)

4.8/5 (44)

When an interest-only swap is established on an amortizing basis,

(Multiple Choice)

4.8/5 (41)

The primary reasons for a counterparty to use a currency swap are

(Multiple Choice)

4.9/5 (38)

Come up with a swap (principal + interest)for two parties A and B who have the following borrowing opportunities.

\ \ LIBOR\% \ 8\% \ +1/2\% \8 .20\% The current exchange rate is $1.60 = €1.00.Company "A" wishes to borrow $1,000,000 for 5 years and "B" wants to borrow €625,000 for 5 years.You are a swap dealer.Quote A and B a swap that makes money for all parties and eliminates exchange rate risk for both A and B.Firms A and B are more concerned with what currency that they borrow in than whether the debt is fixed or floating.

(Essay)

4.8/5 (41)

Consider the situation of firm A and firm B.The current exchange rate is $2.00/£ Firm A is a U.S.MNC and wants to borrow £30 million for 2 years.Firm B is a British MNC and wants to borrow $60 million for 2 years.Their borrowing opportunities are as shown,both firms have AAA credit ratings.

\ £ A \ 6\% £5\% B \7 \% £4\% If firm B could use the forward exchange markets to redenominate a 2-year £30m 4 percent pound sterling loan into a 2-year USD-denominated loan,what would be the interest rate?

(Essay)

4.9/5 (34)

A swap bank has identified two companies with mirror-image financing needs (they both want to borrow equivalent amounts for the same amount of time.Company X has agreed to one leg of the swap but company Y is "playing hard to get."

(Multiple Choice)

4.9/5 (43)

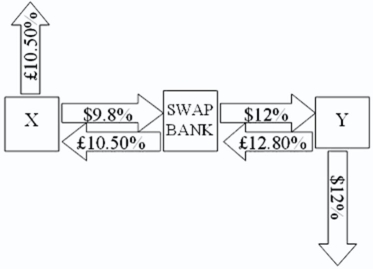

Company X wants to borrow $10,000,000 for 5 years; company Y wants to borrow £5,000,000 for 5 years.The exchange rate is $2 = £1 and is not expected to change over the next 5 years.Their external borrowing opportunities are shown here: \Bortowing E Borrowing Cost Cost Compary X \ 10\% £10.5\% Compary Y \ 12\% £13\% A swap bank proposes the following interest only swap:

X will pay the swap bank annual payments on $10,000,000 with the coupon rate of 9.80 percent; in exchange the swap bank will pay to company X interest payments on £5,000,000 at a fixed rate of 10.5 percent.Y will pay the swap bank interest payments on £5,000,000 at a fixed rate of 12.80 percent and the swap bank will pay Y annual payments on $10,000,000 with the coupon rate of 12 percent.  What is the value of this swap to the swap bank?

What is the value of this swap to the swap bank?

(Multiple Choice)

4.7/5 (35)

Compute the payments due in the first year on a three-year amortizing swap from company B to company A.Company A and company B both want to borrow £1,000,000 for three years.A wants to borrow floating and B wants to borrow fixed.A and B agree to split the QSD.

Fixed-Rate Borrowirg Floatirig-Rate Bort owirig Cost Cost Compary A 10\% LIBOR Compary B 12\% LIBOR+1.5\%

(Multiple Choice)

4.9/5 (44)

Consider the situation of firm A and firm B.The current exchange rate is $2.00/£ Firm A is a U.S.MNC and wants to borrow £30 million for 2 years.Firm B is a British MNC and wants to borrow $60 million for 2 years.Their borrowing opportunities are as shown,both firms have AAA credit ratings.

\ £ A \ 6\% £5\% B \7 \% £4\% The IRP 1-year and 2-year forward exchange rates are ($ ∣ £)= = ($ ∣ £)= = USD pounds

Bid Ask Bid Ask 6\% 6.1\% 4\% 4.1\% Explain how firm B could use the forward exchange markets to redenominate a 2-year £30m 4 percent-pound sterling loan into a 2-year USD-denominated loan.

(Essay)

4.9/5 (34)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)