Exam 14: Interest Rate and Currency Swaps

Exam 1: International Monetary System100 Questions

Exam 2: Globalization and the Multinational Firm100 Questions

Exam 3: Balance of Payments97 Questions

Exam 4: Corporate Governance Around the World100 Questions

Exam 5: The Market for Foreign Exchange100 Questions

Exam 6: International Parity Relationships and Forecasting Foreign Exchange Rates85 Questions

Exam 7: Futures and Options on Foreign Exchange94 Questions

Exam 8: Management of Transaction Exposure100 Questions

Exam 9: Management of Economic Exposure100 Questions

Exam 10: Management of Translation Exposure81 Questions

Exam 11: International Banking and Money Market100 Questions

Exam 12: International Bond Market100 Questions

Exam 13: International Equity Markets100 Questions

Exam 14: Interest Rate and Currency Swaps100 Questions

Exam 15: International Portfolio Investment100 Questions

Exam 16: Foreign Direct Investment and Cross-Border Acquisitions100 Questions

Exam 17: International Capital Structure and the Cost of Capital100 Questions

Exam 18: International Capital Budgeting99 Questions

Exam 19: Multinational Cash Management82 Questions

Exam 20: International Trade Finance100 Questions

Exam 21: International Tax Environment and Transfer Pricing98 Questions

Select questions type

Suppose the quote for a five-year swap with semiannual payments is 8.50−8.60 percent in dollars and 6.60−6.80 percent in euro against six-month dollar LIBOR.This means

Free

(Multiple Choice)

4.8/5  (34)

(34)

Correct Answer: Verified

Verified

C

Consider the situation of firm A and firm B.The current exchange rate is $2.00/£ Firm A is a U.S.MNC and wants to borrow £30 million for 2 years.Firm B is a British MNC and wants to borrow $60 million for 2 years.Their borrowing opportunities are as shown,both firms have AAA credit ratings.

\ £ A \ 6\% £5\% B \7 \% £4\% Act as a swap bank and quote bid and ask prices to A and B that are attractive to A and B and promise to make at least 20bp for your firm.

USD EURO

bid ask bid ask

Free

(Essay)

4.7/5 (42)

Correct Answer:Verified

USD pounds

Consider the situation of firm A and firm B.The current exchange rate is $2.00/£ Firm A is a U.S.MNC and wants to borrow £30 million for 2 years.Firm B is a British MNC and wants to borrow $60 million for 2 years.Their borrowing opportunities are as shown,both firms have AAA credit ratings.

\ £ A \ 6\% £5\% B \7 \% £4\% The IRP 1-year and 2-year forward exchange rates are ($ ∣ £)= = ($ ∣ £)= = USD pounds

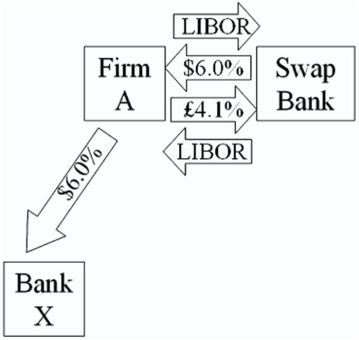

Bid Ask Bid Ask 6\% 6.1\% 4\% 4.1\% Explain how firm A could use two of the swaps offered above to hedge its exchange rate risk.

Free

(Essay)

4.7/5 (22)

Correct Answer:Verified

Firm A could agree to a swap at the pound ask price,agreeing to pay 4.1 percent to the swap bank in exchange for receiving USD LIBOR while at the same time agreeing to a USD swap at the bid price,agreeing to pay USD LIBOR in exchange for receiving $6 percent.

Consider the situation of firm A and firm B.The current exchange rate is $1.50/€.Firm A is a U.S.MNC and wants to borrow €40 million for 2 years.Firm B is a French MNC and wants to borrow $60 million for 2 years.Their borrowing opportunities are as shown; both firms have AAA credit ratings.

\ A \ 7\% 6\% B \8 \% 5\% Explain how this opportunity affects which swap firm B will be willing to participate in.

(Essay)

4.8/5 (38)

An interest-only currency swap has a remaining life of 18 months.It involves exchanging interest at 14 percent on £20 million for interest at 10 percent on $14 million once a year.The term structure of interest rates is currently flat in both the U.S.and in the U.K.If the swap were negotiated today the interest rates exchanged would be $8 percent and £11 percent.All rates were quoted with annual compounding.The current exchange rate is $1.95 = £1.What is the value of the swap to the party paying dollars?

(Essay)

4.8/5 (35)

Consider the situation of firm A and firm B.The current exchange rate is $1.50/€.Firm A is a U.S.MNC and wants to borrow €40 million for 2 years.Firm B is a French MNC and wants to borrow $60 million for 2 years.Their borrowing opportunities are as shown; both firms have AAA credit ratings.

\ A \ 7\% 6\% B \8 \% 5\% Explain how this opportunity affects which swap firm A will be willing to participate in.

(Essay)

4.8/5 (37)

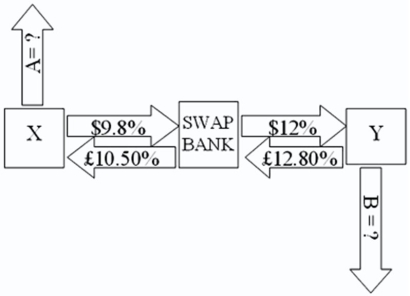

Company X wants to borrow $10,000,000 floating for 5 years; company Y wants to borrow £5,000,000 fixed for 5 years.The exchange rate is $2 = £1 and is not expected to change over the next 5 years.Their external borrowing opportunities are: \Bortowing £ Borrowing Cost Cost Compary X \ 10\% £10.5\% Compary Y \ 12\% £13\% A swap bank proposes the following interest-only swap: Company X will pay the swap bank annual payments on $10,000,000 at an interest rate of $9.80 percent; in exchange the swap bank will pay to company X interest payments on £5,000,000 at a fixed rate of 10.5 percent.Y will pay the swap bank interest payments on £5,000,000 at a fixed rate of 12.80 percent and the swap bank will pay Y annual payments on $10,000,000 with the coupon rate of 12 percent.  If company X takes on the swap,what external actions should they engage in?

If company X takes on the swap,what external actions should they engage in?

(Multiple Choice)

5.0/5 (37)

Consider the situation of firm A and firm B.The current exchange rate is $2.00/£ Firm A is a U.S.MNC and wants to borrow £30 million for 2 years.Firm B is a British MNC and wants to borrow $60 million for 2 years.Their borrowing opportunities are as shown,both firms have AAA credit ratings.

\ £ A \ 6\% £5\% B \7 \% £4\% If firm A could use the forward exchange markets to redenominate a 2-year $60m 6 percent USD loan into a 2-year pound denominated loan,what would be the interest rate?

(Essay)

4.9/5 (35)

Consider the borrowing rates for Parties A and B.A wants to finance a $100,000,000 project at a fixed rate.B wants to finance a $100,000,000 project at a floating rate.Both firms want the same maturity,5 years.

FinI Fixed Rate Floating A \ 10.3\% Prime +1\% B \ 8.9\% Prime +1/2\% For your swap (the one you have shown above)how would the swap bank quote the swap against prime? (Hint: they are quoting a bid-ask spread against "flat" prime.)

(Essay)

4.9/5 (33)

Consider the situation of firm A and firm B.The current exchange rate is $1.50/€.Firm A is a U.S.MNC and wants to borrow €40 million for 2 years.Firm B is a French MNC and wants to borrow $60 million for 2 years.Their borrowing opportunities are as shown; both firms have AAA credit ratings.

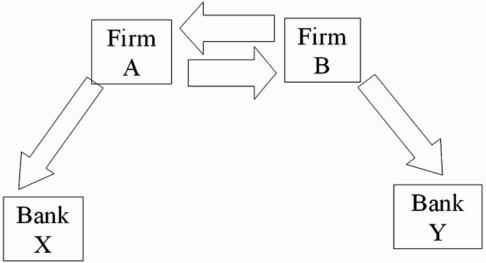

\ A \ 7\% 6\% B \8 \% 5\% Devise a direct swap for A and B that has no swap bank.Show their external borrowing.

(Essay)

4.9/5 (41)

A swap bank has identified two companies with mirror-image financing needs-they both want to borrow equivalent amounts for the same amount of time.Company X has agreed to one leg of the swap but company Y is "playing hard to get."

(Multiple Choice)

4.9/5 (48)

A swap bank makes the following quotes for 5-year swaps and AAA-rated firms: USD Euro

Bid Ask Bid Ask 5\% 5.2\% 7\% 7.2\%

(Multiple Choice)

4.8/5 (43)

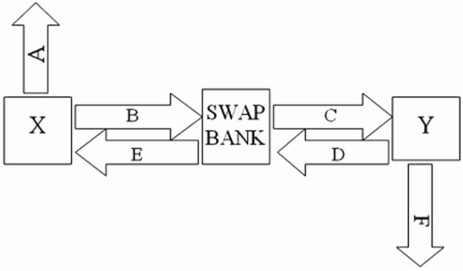

Company X wants to borrow $10,000,000 floating for 5 years; company Y wants to borrow $10,000,000 fixed for 5 years.Their external borrowing opportunities are shown here: Fixed-Rate Floating-Rate Borrowing Cost Bortowing Cost Compary X 10\% LIBOR Compary Y 12\% LIBOR +1.5\% A swap bank is involved and quotes the following rates five-year dollar interest rate swaps at 10.05 percent?10.45 percent against LIBOR flat.  Assume both X and Y agree to the swap bank's terms.Fill in the values for A,B,C,D,E,& F on the diagram.

Assume both X and Y agree to the swap bank's terms.Fill in the values for A,B,C,D,E,& F on the diagram.

(Multiple Choice)

4.9/5 (37)

Find the all-in-cost of a swap to a party that has agreed to borrow $5 million at 5 percent externally and pays LIBOR + ½ percent on a notational principal of $5 million in exchange for fixed rate payments of 6 percent.

(Multiple Choice)

4.9/5 (35)

Consider the situation of firm A and firm B.The current exchange rate is $2.00/£ Firm A is a U.S.MNC and wants to borrow £30 million for 2 years.Firm B is a British MNC and wants to borrow $60 million for 2 years.Their borrowing opportunities are as shown,both firms have AAA credit ratings.

\ £ A \ 6\% £5\% B \7 \% £4\% Explain how this opportunity affects which swap firm A will be willing to participate in.

(Essay)

4.9/5 (31)

Suppose that the swap that you proposed is now 4 years old (i.e.,there is exactly one year to go on the swap).The fourth payment has already been made.If the spot exchange rate prevailing in year 4 is $1.8778 = €1 and the 1-year forward exchange rate prevailing in year 4 is $1.95 = €1,what is the value of the swap to the party paying dollars? If the swap were initiated today the correct rates would be as shown.

(Essay)

4.8/5 (41)

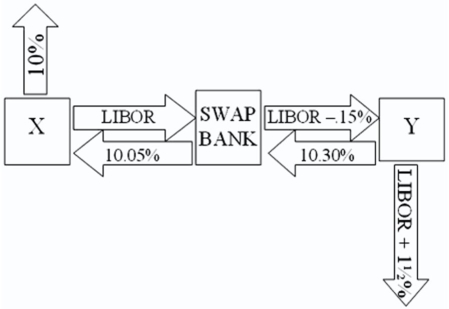

Company X wants to borrow $10,000,000 floating for 5 years; company Y wants to borrow $10,000,000 fixed for 5 years.Their external borrowing opportunities are shown here: Fixed-Rate Floating-Rate Borrowing Cost Bortowing Cost Compary X 10\% LIBOR Compary Y 12\% LIBOR +1.5\% A swap bank proposes the following interest only swap:

X will pay the swap bank annual payments on $10,000,000 with the coupon rate of LIBOR; in exchange the swap bank will pay to company X interest payments on $10,000,000 at a fixed rate of 10.05 percent.Y will pay the swap bank interest payments on $10,000,000 at a fixed rate of 10.30 percent and the swap bank will pay Y annual payments on $10,000,000 with the coupon rate of LIBOR ? 0.15 percent.  What is the value of this swap to the swap bank?

What is the value of this swap to the swap bank?

(Multiple Choice)

4.8/5 (43)

Compute the payments due in the second year on a three-year amortizing swap from company B to company A.Company A and company B both want to borrow £1,000,000 for three years.A wants to borrow floating and B wants to borrow fixed.A and B agree to split the QSD.

Fixed-Rate Borrowirg Floatirig-Rate Bort owirig Cost Cost Compary A 10\% LIBOR Compary B 12\% LIBOR+1.5\%

(Multiple Choice)

4.8/5 (39)

Consider the situation of firm A and firm B.The current exchange rate is $2.00/£ Firm A is a U.S.MNC and wants to borrow £30 million for 2 years.Firm B is a British MNC and wants to borrow $60 million for 2 years.Their borrowing opportunities are as shown,both firms have AAA credit ratings.

\ £ A \ 6\% £5\% B \7 \% £4\% The IRP 1-year and 2-year forward exchange rates are ($ ∣ £)= = ($ ∣ £)= = USD pounds

Bid Ask Bid Ask 6\% 6.1\% 4\% 4.1\% Explain how this opportunity affects which swap firm B will be willing to participate in.

(Essay)

4.8/5 (26)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)