Exam 8: Flexible Budgets, Variances, and Management Control: II

Exam 1: The Accountants Vital Role in Decision Making141 Questions

Exam 2: An Introduction to Cost Terms and Purposes165 Questions

Exam 3: Cost-Volume-Profit Analysis139 Questions

Exam 4: Job Costing138 Questions

Exam 5: Activity-Based Costing and Management133 Questions

Exam 6: Master Budget and Responsibility Accounting150 Questions

Exam 7: Flexible Budgets, Variances, and Management Control: I146 Questions

Exam 8: Flexible Budgets, Variances, and Management Control: II137 Questions

Exam 9: Income Effects of Denominator Level on Inventory Valuation154 Questions

Exam 10: Quantitative Analyses of Cost Functions114 Questions

Exam 11: Decision Making and Relevant Information146 Questions

Exam 12: Pricing Decisions, Product Profitability Decisions, and Cost Management135 Questions

Exam 13: Strategy, Balanced Scorecard, and Profitability Analysis140 Questions

Exam 14: Period Cost Allocation153 Questions

Exam 15: Cost Allocation: Joint Products and Byproducts149 Questions

Exam 16: Revenue and Customer Profitability Analysis137 Questions

Exam 17: Process Costing128 Questions

Exam 18: Spoilage, Rework, and Scrap121 Questions

Exam 19: Cost Management: Quality, Time, and the Theory of Constraints158 Questions

Exam 20: Inventory Cost Management Strategies136 Questions

Exam 21: Capital Budgeting: Methods of Investment Analysis128 Questions

Exam 22: Capital Budgeting: a Closer Look120 Questions

Exam 23: Transfer Pricing and Multinational Management Control Systems141 Questions

Exam 24: Multinational Performance Measurement and Compensation139 Questions

Select questions type

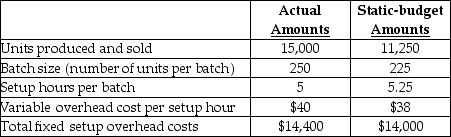

Answer the following question(s) using the information below.

Munoz Inc. produces a special line of plastic toy racing cars in batches. To manufacture a batch of the cars Munoz Inc. must setup the machines and molds. Setup costs are batch-level costs because they are associated with batches rather than individual units of products. A separate Setup Department is responsible for setting up machines and molds for different styles of car.

Setup overhead costs consist of some costs that are variable and some costs that are fixed with respect to the number of setup hours. The following information pertains to June 2012:

-Calculate the rate variance for variable setup overhead costs.

-Calculate the rate variance for variable setup overhead costs.

(Multiple Choice)

4.9/5  (32)

(32)

Identifying the reasons for variances is important because it helps managers plan for corrective action.

(True/False)

4.8/5 (36)

The fixed overhead flexible budget variance is the same as the fixed overhead static budget variance.

(True/False)

4.8/5 (36)

The variable overhead efficiency variance can be interpreted the same way as the efficiency variance for direct-cost items.

(True/False)

4.9/5 (32)

If budgeted machine-hours allowed per actual output unit equals 1.0 hour, and budgeted variable manufacturing overhead per machine-hour is $200, what is the budgeted variable manufacturing overhead rate per output unit?

(Multiple Choice)

4.7/5 (40)

The production-volume variance may also be referred to as the

(Multiple Choice)

4.9/5 (40)

A favourable production-volume variance arises when manufacturing capacity planned for is not used.

(True/False)

4.9/5 (32)

Regal Company uses a single cost pool for fixed manufacturing overhead. The amount for June 2012 was budgeted at $500,000; however, the actual amount was $700,000. Actual production for June was 12,500 units, and actual machine hours were 10,000. Budgeted production included 17,750 units and 12,375 machine hours. What is the budgeted fixed overhead rate per machine hour?

(Multiple Choice)

4.9/5 (36)

In flexible budgets, costs that remain the same regardless of the output levels within the relevant range are

(Multiple Choice)

4.8/5 (36)

Variance analysis of variable nonmanufacturing as well as variable manufacturing costs is used for pricing decisions and for decisions about which products to emphasize.

(True/False)

4.8/5 (36)

Which option(s) would be consistent with the proration approach for end-of-period adjustments when the underallocated or overallocated variable overhead costs are significant?

(Multiple Choice)

4.9/5 (43)

An unfavourable variable overhead rate variance indicates that

(Multiple Choice)

4.9/5 (38)

Managers have found that non-financial measures provide useful information for their planning and control decisions.

(True/False)

4.9/5 (33)

Actual overhead is $700,000, while budgeted overhead is $598,000. What is the fixed overhead static-budget variance if 250,000 units are produced and 225,000 are budgeted?

(Multiple Choice)

4.7/5 (44)

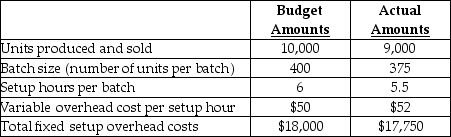

Answer the following question(s) using the information below.

Lukehart Industries Inc. produces air purifiers in batches. To manufacture a batch of the purifiers Lukehart Inc. must setup the machines and assembly line tooling. Setup costs are batch-level costs because they are associated with batches rather than individual units of products. A separate Setup Department is responsible for setting up machines and tooling for different models of the air purifiers.

Setup overhead costs consist of some costs that are variable and some costs that are fixed with respect to the number of setup hours. The following information pertains to June 2012:

-Calculate the efficiency variance for variable setup overhead costs.

-Calculate the efficiency variance for variable setup overhead costs.

(Multiple Choice)

4.9/5 (38)

The production-volume variance arises because the actual output level differs from the output level used as the denominator to calculate the budgeted fixed overhead rate.

(True/False)

4.7/5 (31)

An unfavourable fixed setup overhead rate variance could be due to higher lease costs of new setup equipment or higher salaries paid to engineers and supervisors.

(True/False)

4.8/5 (36)

In order to properly record a fixed manufacturing overhead rate variance of $30,000 unfavourable and a production-volume overhead variance of $20,000 favourable, what would the appropriate journal entry be if actual fixed overhead is $500,000?

(Multiple Choice)

4.8/5 (46)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)