Exam 8: Flexible Budgets, Variances, and Management Control: II

Exam 1: The Accountants Vital Role in Decision Making141 Questions

Exam 2: An Introduction to Cost Terms and Purposes165 Questions

Exam 3: Cost-Volume-Profit Analysis139 Questions

Exam 4: Job Costing138 Questions

Exam 5: Activity-Based Costing and Management133 Questions

Exam 6: Master Budget and Responsibility Accounting150 Questions

Exam 7: Flexible Budgets, Variances, and Management Control: I146 Questions

Exam 8: Flexible Budgets, Variances, and Management Control: II137 Questions

Exam 9: Income Effects of Denominator Level on Inventory Valuation154 Questions

Exam 10: Quantitative Analyses of Cost Functions114 Questions

Exam 11: Decision Making and Relevant Information146 Questions

Exam 12: Pricing Decisions, Product Profitability Decisions, and Cost Management135 Questions

Exam 13: Strategy, Balanced Scorecard, and Profitability Analysis140 Questions

Exam 14: Period Cost Allocation153 Questions

Exam 15: Cost Allocation: Joint Products and Byproducts149 Questions

Exam 16: Revenue and Customer Profitability Analysis137 Questions

Exam 17: Process Costing128 Questions

Exam 18: Spoilage, Rework, and Scrap121 Questions

Exam 19: Cost Management: Quality, Time, and the Theory of Constraints158 Questions

Exam 20: Inventory Cost Management Strategies136 Questions

Exam 21: Capital Budgeting: Methods of Investment Analysis128 Questions

Exam 22: Capital Budgeting: a Closer Look120 Questions

Exam 23: Transfer Pricing and Multinational Management Control Systems141 Questions

Exam 24: Multinational Performance Measurement and Compensation139 Questions

Select questions type

Trilite Windows manufactures windows. The 2012 operating budget is based on production of 56,000 windows with 1.0 machine hours allowed per window. Variable manufacturing overhead is anticipated to be $896,000.

Actual production for 2012 was 58,000 windows using 60,000 machine hours. Actual variable costs were $15 per machine hour.

Required:

Determine the variable overhead rate and efficiency variances.

(Essay)

4.8/5  (36)

(36)

Mediquip International is a manufacturing firm that has many assembly lines, numerous heavy duty machines and highly skilled machine operators. It has used very complex variance analysis in planning and controlling it operations during the last few years. Everything always appeared to be satisfactory until an economic recession tightened the competition and cost control became critical to the company's success. The operating managers believe that the traditional managerial accounting variance measures do not provide all the information they need during times of economic difficulties.

Required:

Discuss what additional information could be provided to the managers.

(Essay)

4.8/5 (41)

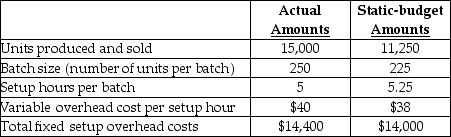

Answer the following question(s) using the information below.

Munoz Inc. produces a special line of plastic toy racing cars in batches. To manufacture a batch of the cars Munoz Inc. must setup the machines and molds. Setup costs are batch-level costs because they are associated with batches rather than individual units of products. A separate Setup Department is responsible for setting up machines and molds for different styles of car.

Setup overhead costs consist of some costs that are variable and some costs that are fixed with respect to the number of setup hours. The following information pertains to June 2012:

-Calculate the flexible-budget variance for variable setup overhead costs.

-Calculate the flexible-budget variance for variable setup overhead costs.

(Multiple Choice)

4.9/5 (33)

Which decisions are most likely to have been made by the start of the accounting period?

(Multiple Choice)

4.9/5 (42)

The difference between the actual amount of variable overhead incurred and the budget amount allowed for actual output achieved is

(Multiple Choice)

4.8/5 (36)

The difference between budgeted fixed overhead and fixed overhead allocated for actual output units achieved, is the production-volume variance.

(True/False)

4.7/5 (28)

Answer the following question(s) using the information below.

Munoz Inc. produces a special line of plastic toy racing cars in batches. To manufacture a batch of the cars Munoz Inc. must setup the machines and molds. Setup costs are batch-level costs because they are associated with batches rather than individual units of products. A separate Setup Department is responsible for setting up machines and molds for different styles of car.

Setup overhead costs consist of some costs that are variable and some costs that are fixed with respect to the number of setup hours. The following information pertains to June 2012:

-Calculate the production-volume variance for fixed setup overhead costs.

(Multiple Choice)

4.9/5 (41)

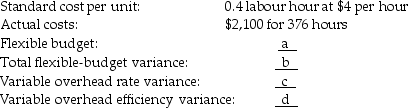

McKenna Company manufactured 1,000 units during April with a total overhead budget of $12,400.

However, while manufacturing the 1,000 units the microcomputer that contained the month's cost

information broke down. With the computer out of commission, the accountant has been unable to

complete the variance analysis report. The information missing from the report is lettered in the

following set of data:

Variable overhead:

Fixed overhead:

Fixed overhead:

Required:

Required:

(Essay)

4.7/5 (36)

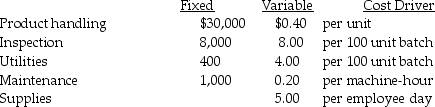

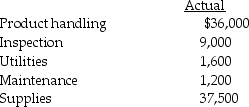

Jael Equipment uses a flexible budget for its indirect manufacturing costs. For 2012 the company anticipated that it would produce 18,000 units with 3,500 machine-hours and 7,200 employee days. The costs and cost drivers were to be as follows:

During the year, the company processed 20,000 units; worked 7,500 employee days; and, had 4,000 machine hours. The actual costs for 2012 were:

During the year, the company processed 20,000 units; worked 7,500 employee days; and, had 4,000 machine hours. The actual costs for 2012 were:

Required:

a. Prepare the static-budget using the overhead items above and then compute the static-budget variances.

b. Prepare the flexible-budget using the overhead items above and then compute the flexible-budget variances.

Required:

a. Prepare the static-budget using the overhead items above and then compute the static-budget variances.

b. Prepare the flexible-budget using the overhead items above and then compute the flexible-budget variances.

(Essay)

4.9/5 (33)

Regal Company uses a single cost pool for fixed manufacturing overhead. The amount for June 2012 was budgeted at $500,000; however, the actual amount was $700,000. Actual production for June was 12,500 units, and actual machine hours were 10,000. Budgeted production included 17,750 units and 12,375 machine hours. What is the budgeted fixed overhead rate per output unit?

(Multiple Choice)

5.0/5 (32)

The variable overhead efficiency variance measures the efficiency with which the cost-allocation base is used.

(True/False)

4.9/5 (30)

Variable overhead rate variance is the difference between the actual amount of variable overhead incurred and the budgeted amount allowed for the actual quantity of the variable overhead allocation base used for the actual output units achieved.

(True/False)

4.9/5 (31)

Calculate the fixed manufacturing overhead rate variance based on the following data:

(Essay)

4.9/5 (43)

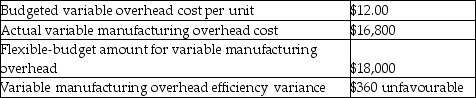

Use the information below to answer the following question(s).

Michelle Inc. uses a level 4-variance analysis of its manufacturing overhead costs, and has the following results for April.

A. Budgeted direct labour-hours per unit is used to allocate variable manufacturing overhead.

B. Budgeted amounts for April 2012 are:

B. Budgeted amounts for April 2012 are:

C. Actual amounts for April 2012 are:

C. Actual amounts for April 2012 are:

-What are the fixed manufacturing overhead efficiency and production-volume variances, respectively?

-What are the fixed manufacturing overhead efficiency and production-volume variances, respectively?

(Multiple Choice)

4.8/5 (43)

Effective planning of variable overhead costs means that a company performs those variable overhead costs that primarily add value

(Multiple Choice)

4.9/5 (35)

Answer the following question(s) using the information below.

Kellar Corporation manufactured 1,500 chairs during June. The following variable overhead data pertain to June:

-What is the variable overhead rate variance?

-What is the variable overhead rate variance?

(Multiple Choice)

5.0/5 (31)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)