Exam 19: Cost Management: Quality, Time, and the Theory of Constraints

Exam 1: The Accountants Vital Role in Decision Making141 Questions

Exam 2: An Introduction to Cost Terms and Purposes165 Questions

Exam 3: Cost-Volume-Profit Analysis139 Questions

Exam 4: Job Costing138 Questions

Exam 5: Activity-Based Costing and Management133 Questions

Exam 6: Master Budget and Responsibility Accounting150 Questions

Exam 7: Flexible Budgets, Variances, and Management Control: I146 Questions

Exam 8: Flexible Budgets, Variances, and Management Control: II137 Questions

Exam 9: Income Effects of Denominator Level on Inventory Valuation154 Questions

Exam 10: Quantitative Analyses of Cost Functions114 Questions

Exam 11: Decision Making and Relevant Information146 Questions

Exam 12: Pricing Decisions, Product Profitability Decisions, and Cost Management135 Questions

Exam 13: Strategy, Balanced Scorecard, and Profitability Analysis140 Questions

Exam 14: Period Cost Allocation153 Questions

Exam 15: Cost Allocation: Joint Products and Byproducts149 Questions

Exam 16: Revenue and Customer Profitability Analysis137 Questions

Exam 17: Process Costing128 Questions

Exam 18: Spoilage, Rework, and Scrap121 Questions

Exam 19: Cost Management: Quality, Time, and the Theory of Constraints158 Questions

Exam 20: Inventory Cost Management Strategies136 Questions

Exam 21: Capital Budgeting: Methods of Investment Analysis128 Questions

Exam 22: Capital Budgeting: a Closer Look120 Questions

Exam 23: Transfer Pricing and Multinational Management Control Systems141 Questions

Exam 24: Multinational Performance Measurement and Compensation139 Questions

Select questions type

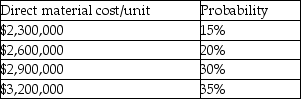

Columbus Shipbuilding Ltd. is preparing a bid on a contract to supply 8 small vessels. It is facing two issues in preparing its estimates. First, due to volatility in the market place there is uncertainty regarding the cost of direct materials. Second, it recognizes that there will be improvements in labour productivity during the contract.

Columbus has estimated the following probability distribution for its direct materials costs:

In estimating the direct labour costs, Columbus has predicted a 90% cumulative average time learning curve. The time required to produce the first vessel is estimated at 4,000 hours. Direct labour costs average $68 per hour.

Manufacturing overhead is applied at the rate of 250% of direct labour costs. The bid price will be established to permit a 40% gross margin.

Required:

Prepare the total bid price for the order.

In estimating the direct labour costs, Columbus has predicted a 90% cumulative average time learning curve. The time required to produce the first vessel is estimated at 4,000 hours. Direct labour costs average $68 per hour.

Manufacturing overhead is applied at the rate of 250% of direct labour costs. The bid price will be established to permit a 40% gross margin.

Required:

Prepare the total bid price for the order.

(Essay)

4.8/5  (37)

(37)

Which of the following statements related to the theory of constraints is/are true?

(Multiple Choice)

4.8/5 (35)

Producing more non-bottleneck output increases throughput contribution.

(True/False)

4.9/5 (37)

The Glass Shop, a manufacturer of large windows, is experiencing a bottleneck in its plant. Setup time at one of its workstations has been identified as the culprit. A manager has proposed a plan to reduce setup time at a cost of $72,000. The change will result in 8,000 additional windows. The selling price per window is $18, direct labour costs are $3 per window, and the cost of direct materials is $5 per window. Assume all units produced can be sold. The change will result in an increase in the throughput contribution of:

(Multiple Choice)

4.7/5 (33)

When an average unit of time declines by a constant percentage each time that the cumulative quantity of units produced is doubled, it is known as

(Multiple Choice)

4.8/5 (34)

Which of the following are not nonfinancial measures for evaluating customer satisfaction?

(Multiple Choice)

5.0/5 (35)

Bank of Bowmanville has variable demand for its counter services. The daily demand ranges from 200 to 250 customers a day and the average banking transaction takes 6 minutes. The average daily demand is 228 customers. The bank currently has 5 staff members serving the counter and operates 7 hours a day.

Required:

a. What is the average customer waiting time in minutes?

b. In an effort to reduce costs, the bank is considering eliminating one of its counter services staff and having a manager fill in during two hours of the day. What would be the effect of this change on wait time? What might the customers' reaction be?

(Essay)

4.8/5 (34)

Aunt Lydia's Cookies, Inc., prepares frozen gourmet cookies for shipment to upscale grocery stores as well as mailing to web and catalog customers. The company has two workstations, cooking and distribution. The cooking station is limited by the cooking time of the food. Distribution is limited by the speed of the workers. Distribution normally waits on food from cooking. Because the demand has increased in recent months to 4,000 dozen cookies, management is considering adding another oven in the cooking station or else having the cooks start to work earlier. The monthly cost of operating the cooking station one more hour each day is $1,500. The cost of adding another cooking station would add an average of $8 per hour. The current operating hours total eight hours a day, 24 days a month. The contribution margin of the finished products is currently $2 per dozen. Inventory carrying costs average $0.50 per dozen per month. Either the extra hour or the new cooking station would increase production by 50 dozen a day, with a long-run increase of 100 dozen units in finished goods inventory to 500 dozen.

Required:

a. What is the total production per month if the change is made?

b. What is the increase in the expected monthly product contribution for each of the possible changes? Assume long-run production equals sales.

c. What course of action would you recommend?

(Essay)

4.8/5 (35)

Compare financial and nonfinancial performance, and explain why planning and control systems should consider both.

(Essay)

4.8/5 (36)

Manufacturing lead time is a combination of order receipt time and order manufacturing time.

(True/False)

4.9/5 (36)

In order for management to initiate quality improvement programs and projects, a complete cost-benefit analysis (including a projection of how the improvement will incrementally affect total costs and total revenues) is necessary.

(True/False)

4.9/5 (38)

When a firm has a bottleneck machine, a good way to manage the bottleneck is to make sure that prior machines produce more units for the bottleneck machine to increase its throughput.

(True/False)

4.8/5 (42)

Palmateer Industries makes an electronic component in two departments, Machining and Assembly. The capacity per month is 30,000 units in the Machining Department and 20,000 in the Assembly Department. The only variable cost of the product is the direct material of $100 per unit. All direct material cost is incurred in the Machining Department. All other costs of operating the two departments are fixed costs. Palmateer can sell as many units of this electronic component as it produces at a selling price of $300 per unit.

Required:

Assuming any defective unites produced in either department must be scrapped:

a. Compute the loss that occurs if a defective unit is produced in the Machining Department.

b. Compute the loss that occurs if a defective unit is produced in the Assembly Department.

c. How do your answers in parts (a) and (b) relate to the theory of constraints? Explain.

(Essay)

4.9/5 (41)

Design Products is committed to its quality program. It works with all areas of the company to establish sound quality programs within reasonable budget guidelines. For the current year, it has budgeted $1,000,000 for prevention costs and $800,000 for appraisal costs. Internal failure has a budget of $100 per failed item, while external failure has a total budget of $600,000.

Product Testing has proposed to management a new method of testing products. If management decides to implement the new method, $2 per unit of appraisal costs will be saved, up to a level of 200,000 tests. No additional savings are incurred past the 200,000 level. The new method involves $110,000 in training costs and $60,000 in yearly testing supplies.

Traditionally, 3 percent of all completed items have to be reworked. External failure costs average $120 per failed unit. The company's average external failures are 1 percent of units sold. The company carries no ending inventories.

Required:

a. What is the adjusted budget for appraisal costs assuming the new method is implemented and 800,000 units are tested during the manufacturing process during the year?

b. How much does internal failure costs change assuming 600,000 units are tested under the new method and it reduces the amount of unacceptable units in the manufacturing process by 40 percent?

c. What would be the change in the external failure budget assuming external failures are reduced by 60 percent, assuming the same facts as in part (b)?

(Essay)

4.8/5 (39)

A corporation can measure its quality performance by using financial or nonfinancial measures of quality. Discuss the merits of each method and whether the use of one precludes the use of the other.

(Essay)

4.8/5 (41)

When considering the theory of constraints, operating costs refer to all costs involved in the manufacturing process.

(True/False)

4.9/5 (39)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)